Does Opening a Checking Account Affect Your Credit Score?

It’s one of the most common questions people ask when starting their financial journey: “Does opening a checking account affect your credit score?”

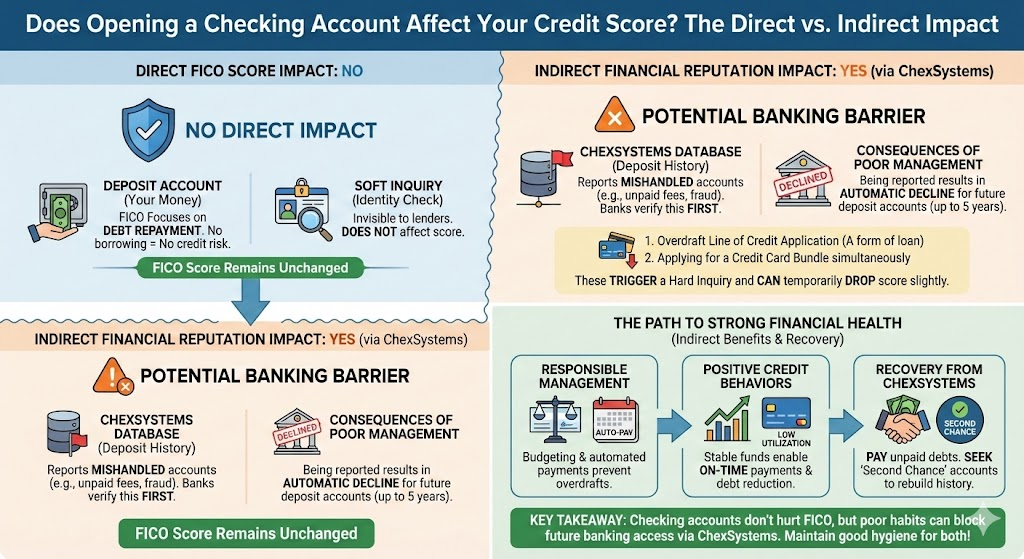

The short answer is: No, opening a checking account does not directly impact your credit score.

However, the longer and more important answer is that the process of opening and managing a checking account can affect your credit file and your ability to open future accounts in several significant ways. Understanding these nuances is crucial for maintaining your long-term financial health.

This article breaks down the relationship between consumer banking accounts and consumer credit scores, detailing how banks screen applicants and how your checking account habits can eventually build—or damage—your financial reputation.

Why Checking Accounts Don’t Affect FICO

Your credit score (like the FICO Score or VantageScore) is designed to measure one thing: your reliability in repaying borrowed money.

A checking account, by definition, is a deposit account, not a debt account. You are depositing and spending your own money. Therefore, traditional credit scoring models ignore checking and savings accounts for the following reasons:

1. No Borrowing, No Credit Risk

The FICO model focuses on debt repayment. Since a checking account does not involve borrowing (it’s your money), there is no credit risk to assess. The 35% of your score dedicated to Payment History is based on loans, credit cards, and mortgages, not deposit accounts.

2. Soft Inquiries vs. Hard Inquiries

When you open a checking account, the bank often pulls a soft inquiry on your credit report.

- Soft Inquiry (Check for Identity): This happens when a bank confirms your identity to prevent fraud. Soft inquiries are visible only to you and do not affect your credit score whatsoever.

- Hard Inquiry (Check for Credit): This happens when you apply for a credit product (like a credit card, auto loan, or personal loan). These inquiries are visible to everyone and can temporarily drop your score by a few points.

Crucial Takeaway: Opening a checking account results in a soft inquiry, which means zero direct impact on your FICO Score.

The Indirect Impact: Screening and the ChexSystems Database

While your FICO Score is safe, banks use other specialized consumer reports to determine if they should accept you as a customer. The primary tool they use is ChexSystems.

What is ChexSystems?

ChexSystems is a consumer reporting agency that functions specifically for deposit accounts. Banks report individuals who have “mishandled” a checking or savings account.

| Factor | Credit Report (FICO) | Deposit Report (ChexSystems) |

|---|---|---|

| Purpose | Measures risk of repaying borrowed money (Debt). | Measures risk of managing deposit accounts (Fraud/Fees). |

| Key Data | Late payments, Credit Utilization, Account Age. | Unpaid negative balances, excessive overdrafts, suspected fraud. |

| Direct Impact | Yes (Affected by hard inquiries and late payments). | No (Doesn’t affect FICO, but affects future bank approvals). |

How Bad Checking Account Habits Affect Your Future

The real danger lies in how poorly managing your checking account can land you in the ChexSystems database, which is a significant barrier to future banking.

A bank will report you to ChexSystems if you:

- Close an account with an unpaid negative balance: This is the most common reason. If overdraft fees or monthly service charges drive your account into the negative, and you fail to pay it off, the bank reports the loss.

- Commit fraud: Passing bad checks or misrepresenting information to open the account.

- Have excessive overdrafts: Although less common, some banks report chronic misuse of overdraft services.

If you are reported, many financial institutions will automatically decline your application for a new checking account for up to five years, regardless of how good your credit score is. This is the biggest consequence of poor checking account management.

When a Checking Account Application Triggers a Hard Inquiry

There is one key exception where opening a bank account can trigger a hard inquiry and slightly affect your credit score: when you apply for credit simultaneously.

1. The Overdraft Line of Credit

When you sign up for “overdraft protection,” the bank often links your checking account to a small, revolving line of credit to cover any shortfalls.

- If the bank offers an automated transfer from your savings, it’s a soft inquiry.

- If the bank offers a line of credit (a form of loan) to cover the overdraft, they perform a hard inquiry to assess the credit risk of that loan.

If you are offered overdraft protection that involves a line of credit, ask the bank explicitly if the application requires a hard inquiry on your credit report.

2. Signing Up for a Credit Card Bundle

Some banks offer promotional bundles (e.g., “Open a new checking account and get pre-approved for our Rewards Credit Card”). If you accept the credit card offer during the checking account application process, you are applying for credit, and a hard inquiry will be generated.

The Path to Building a Stronger Financial Profile

While opening a checking account won’t boost your FICO score, consistently and responsibly managing it is fundamental to building a strong financial profile.

1. Using Debit for Credit Building

Using your debit card responsibly helps you establish a positive banking history (which banks like), but it does not feed positive information to FICO.

2. The Link to Savings

The funds you manage and save in your checking account directly enable you to achieve the key components of a high credit score:

- Pay Down Debt (30% of FICO): Good checking management helps you free up cash flow to reduce your Credit Utilization Ratio.

- Avoid Defaults (35% of FICO): Automated payments from a well-managed checking account are the best defense against late payments.

3. Recovering from ChexSystems

If you find yourself in the ChexSystems database, you must take immediate action to regain banking access:

- Pay the Debt: Contact the bank that reported you and pay the full balance of the negative fee or debt. Get a receipt or confirmation that the debt is settled.

- Request an Update: Ask the bank to update their ChexSystems report to “Paid in Full.”

- Seek Second Chance Banking: Look for banks or credit unions that offer “second chance checking” accounts. These accounts typically have higher fees or fewer features but allow you to re-establish a positive banking history.

Summary: FICO vs. ChexSystems

The rule is simple: Opening an account with your own money is a soft inquiry and does not affect your FICO credit score. However, poor account management (leading to an unpaid negative balance) can result in a ChexSystems report, which will severely limit your ability to open any future deposit accounts.

Maintain perfect financial hygiene in your checking account, and your credit score will remain unaffected, while your banking opportunities remain wide open.

FAQs

1. Why does opening a standard checking account have zero direct impact on my FICO credit score?

A FICO score measures your reliability in repaying borrowed money (debt). Since a checking account is a deposit account where you are using your own money, there is no borrowing or credit risk to be measured by traditional credit scoring models.

2. What is the difference between a soft inquiry and a hard inquiry during the application process?

A soft inquiry is performed by the bank to confirm your identity and prevent fraud; it is visible only to you and does not affect your credit score. A hard inquiry happens only when you apply for a credit product (like a loan or credit card) and can temporarily drop your score. Opening a standard checking account usually results in only a soft inquiry.

3. What is ChexSystems and how does it affect my ability to open new bank accounts?

ChexSystems is a consumer reporting agency that banks use to screen applicants for new deposit accounts. Banks report individuals who have “mishandled” an account (e.g., unpaid negative balances or fraud). Being reported to ChexSystems can lead many financial institutions to automatically deny your application for a new checking account for up to five years.

4. What is the most common reason a bank will report someone to ChexSystems?

The most common reason is closing an account that has an unpaid negative balance. This occurs when fees (like overdraft or monthly service charges) drive the account into the negative, and the customer fails to pay the loss back to the bank.

5. When is the exception? When might a checking account application trigger a hard inquiry?

A hard inquiry is triggered only when the application involves applying for a credit product simultaneously. This happens if you opt-in for an overdraft protection service that is set up as a revolving line of credit (a loan), or if you accept a bundled offer for a credit card during the application.

6. How long does a negative report on ChexSystems last?

The selected text doesn’t explicitly state the duration, but it notes that a negative report can cause denial for a new checking account for up to five years.