How Does the Fair Credit Reporting Act Protect You?

The Fair Credit Reporting Act covers your credit reports. It started in 1970. It makes sure info is accurate. It stops misuse. Bureaus like Equifax and TransUnion must follow it. You get free reports. You can fix errors. It fights theft too. In 2025, changes help with medical debt. And privacy. This guide tells all. You learn your rights. How to use them. What if rules break. It fits renters. Job hunters. Anyone with credit. Know this. You save money. Avoid stress. Start here.

Key Fair Credit Reporting Act Rights You Need to Know

FCRA gives you free credit reports. One per year from each bureau. Go to AnnualCreditReport.com. Check for wrong info. Like old debts. Or fake accounts. Pull them now. Spot issues fast.

You have the right to dispute errors. Send a note. Or use online forms. Bureau checks in 30 days. They ask the bank or lender. If no proof, it deletes. You get a new report free. This fixes scores quick.

Bureaus can’t share your report without reason. Lenders for loans. Employers if you say yes. No selling to strangers. It keeps privacy. Medical details stay out unless you allow.

If denied credit or a job, you get notice. The letter says why. And gives your report. Plus rights to fight it. This lets you fix before it’s too late.

In 2025, rights hold. CFPB withdrew a data broker rule in May. But Homebuyers Privacy Act stops trigger leads. No spam calls from your report. Good for calm.

These rights help daily. Rent an apartment. Check report first. See a late pay. Dispute it. Score goes up. Approval comes.

- Free reports yearly from Equifax, Experian, TransUnion

- Dispute any inaccuracy with 30-day fix

- Limits on who sees your credit data

- Notices for denials or bad actions

How FCRA Ensures Credit Report Accuracy and Fairness

- FCRA says reports must be accurate. Bureaus take steps to check data. They update old info. Lenders report right. No wrong balances. No made-up accounts.

- Find an error? Dispute it. Write a letter. List the problem. Add proof like bills. Send to the bureau. They look into it. Talk to the lender. 30 days top. Fix it or delete.

- If they say no, add your side. Short note on the report. Up to 100 words. Lenders see it. It gives context.

- 2025 brings more on accuracy. CFPB fined Equifax $425 million in January. For slow checks. And bad deletes. Now rules speed things. AI spots issues. But people review too.

- Fairness means no unfair marks. Old negatives drop after 7 years. Bankruptcies 10. No bias in reports. CFPB watches that. Fines up to $1,000 for breaks.

Check reports often. Quarterly beats yearly. Catch trends. Like debt creep. Fix before it hurts.

Steps to Dispute Credit Report Errors Under FCRA

Disputes fix wrong info on your report. FCRA gives you the right to challenge it. Bureau must investigate. They talk to the lender. 30 days max. If no proof, it deletes. You get a free update. Start with your report. Mark the errors. Wrong address. Fake loan. Old charge-off. This process works for most. One in five reports has mistakes. 80% of disputes get some fix. Keep records. It helps if they say no.

Pull your report first. Mark what’s wrong. Wrong address. Fake loan. Old charge off.

Make a letter. Or use the site form. Put your name. Address. Account numbers. Explain the error. Add proof. Like bank statements.

Send it certified. Keep the receipt. Bureau says they got it in 5 days. They check in 30.

- List the exact error

- Attach proof copies

- Keep your originals safe

- Follow up if over time

One in five reports has mistakes. 80% of disputes get some fix. Keep at it. Re-dispute with new facts.

FCRA Identity Theft Protection: What You Can Do

FCRA helps with theft. Free reports if hit. Weekly for a year. Extended alert for 7 years. It blocks new credit.

- Freeze your credit free. At all bureaus. Get a PIN to lift. Temp or full. Thieves can’t open accounts.

- Put a fraud alert. Lenders check ID extra. One year. Or 7 for big cases.

- Bureaus block stolen data. Like your SSN. They remove fake accounts fast.

- 2025 adds more. CFPB pushes locks on apps. They alert changes right away.

- If stolen, file a report. Police first. Then FTC site. Get the affidavit. Dispute the fakes.

Don’t wait. Act quick. Cuts the damage big.

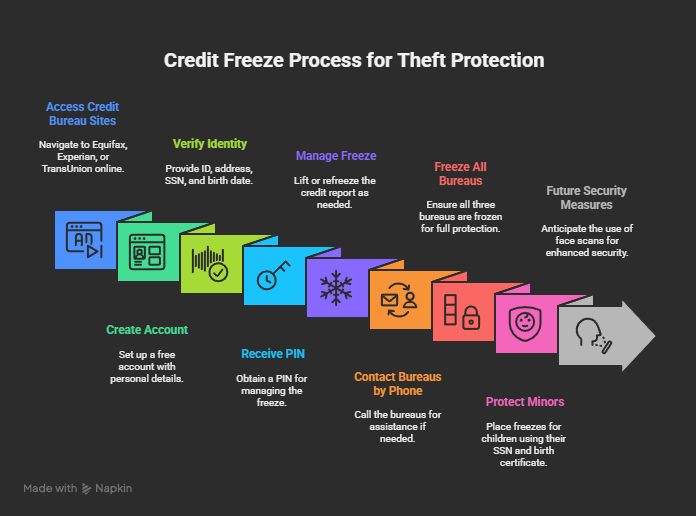

How to Place a Credit Freeze Under FCRA for Theft Protection

A credit freeze blocks access to your report. It stops thieves from opening new accounts. FCRA makes it free for everyone. No time limit. You control when to lift it. Start online. It takes minutes.

- Go to Equifax myEquifax site. Or Experian.com. TransUnion.com too. Set up a free account. Give your ID. Address. SSN. Birth date. Answer security questions. They confirm you.

- You get a PIN right away. Use it to lift the freeze. Temp lift for 1 to 7 days. Or just hours. Pick one lender if needed. Full lift turns it off for good. But you can refreeze anytime.

- No computer? Call them. Equifax at 888-298-0045. Experian 888-397-3742. TransUnion 888-909-8872. Verify your ID over the phone. Rep sets it up. Free call.

- Freeze all three bureaus. Lenders pull from any one. Do it separate. Takes 10 minutes total.

- For kids under 18, parents place it. Use the minor’s SSN. Add birth certificate proof. Call or online. Protects them from theft early.

- In 2025, some sites use face scans. Upload a selfie. Matches your ID. Makes it more secure. No extra steps. Brings peace.

FCRA and Employment Background Checks: Your Rights

Employers often pull credit reports to check your financial history. But FCRA sets clear rules. They must get your written consent before looking. No surprise pulls. This protects your privacy. If they deny a job based on the report, they have to tell you. You get a copy of the report and a summary of your rights. This gives you a chance to dispute any errors. Like an old arrest that shouldn’t be there. Or fake work history. In 2025, FCRA ties in with EEOC rules. No bias from reports.

Things like race or age can’t factor in. About 75% of bosses check credit for some roles. But some skip the consent step. If they do, you can sue. It’s a violation. Always ask what they pull. Check your report ahead. Fix errors before the interview. This way, you show up strong.

- Get written consent before any pull

- Receive notice and report copy if denied

- Dispute wrongs like old records or fakes

- EEOC links no bias on race or age

- Sue if consent skipped—know your leverage

- Ask details on what they check

- Review report early to fix issues

Understanding FCRA Adverse Action Notices

An adverse action notice comes when something bad happens because of your report. Like denied credit. No job offer. Or higher insurance rates. FCRA requires the sender to give you notice. The letter lists the reasons. High debt. Late payments. It comes with a free copy of your report. And a summary of your rights to dispute. You have 60 days from the denial to act. Dispute anything wrong.

In 2025, digital notices are fine. Email works. It gets to you faster than mail. But notices can be vague. Don’t stop there. Ask for more details. CFPB has your back. They can push for clarity. Use the notice to fight back. Fix the issue. Your score improves. The next try goes better.

- Notice required for denials on credit, jobs, insurance

- Lists reasons like debt or lates

- Includes free report copy and rights summary

- 60 days to dispute from denial date

- Digital email okay in 2025 for speed

- Ask CFPB if vague—get full details

- Fight it to fix score for next time

FCRA Violations: Examples and What to Do If It Happens to You

FCRA violations break the rules. Like inaccurate reports. Slow disputes. Or sharing data wrong. In 2025, CFPB fined Equifax $425 million. For bad checks on disputes. And wrong deletes. Another example. A bank reports a closed account as open. Your score drops. A class suit follows. Privacy breaks too.

Report sold to the wrong person. Pays $750 to $1,000 each time. Willful violations get punitive damages. Up to $1,000. Plus lawyer fees. What to do? Complain to the bureau first. Then CFPB. Or FTC. Sue in court. Small claims is simple. No lawyer needed. Many cases settle quiet. But push for change. Log everything. Dates. Names. Build your case strong.

- Inaccurate reports or slow disputes

- Wrong sharing or privacy breaks

- 2025 Equifax fine $425 million example

- Bank closed account error leads to suits

- Willful gets $1,000 punitive plus fees

- Complain to bureau, CFPB, FTC first

- Sue in small claims—log all details

Penalties for FCRA Violations

Negligent violations mean actual damages. Plus fees. Up to $1,000 per case. Willful ones hit harder. Statutory damages $100 to $1,000. Punitive too. Class actions bring millions. CFPB fines big. Equifax paid $425 million in 2025. Suits rose 20% from 2024. Know the law. Report any breaks. It holds them accountable.

- Negligent: Actual damages + fees up to $1,000

- Willful: $100-$1,000 statutory + punitive

- Class actions lead to millions in payouts

- CFPB fines like Equifax’s $425 million

- Suits up 20% year over year

- Report to enforce—know your rights

How FCRA Has Evolved in 2025: Recent Changes and What They Mean

2025 brought tweaks. Homebuyers Act ended trigger leads. More privacy from spam calls. CFPB finalized medical debt rule in January. It banned bills on reports. Court vacated it in August. CFPB won’t reissue the advisory. Under $500 debts stay gone. Paid ones drop fast anyway. Scoring models use rent more. VantageScore at 10% weight. The law dates to 1970. Tech outpaces it. CFPB works on updates. For you, it means better privacy. Easier disputes. Digital notices speed things. Stay on top. Check the FTC site often.

- Homebuyers Act: No more trigger leads for privacy

- Medical debt rule finalized then vacated—bills still limited

- Under $500 debts gone, paid drop quick

- VantageScore rent weight up to 10%

- 1970 law vs. modern tech—CFPB updating

- Better privacy, disputes, digital notices for you

Actionable Steps to Use FCRA Protections Daily

Use rights every day. Pull a free report. Quarterly works best. Spot errors early. Dispute online. Templates make it easy. Track the 30 days. Freeze if at risk. It’s free. Keep the PIN safe. Opt out of prescreen offers. Less junk mail comes. Use OptOutPrescreen.com. Monitor with apps. Free alerts keep you posted. For jobs, get consent in writing. Ask for the report copy. 2025 has AI for disputes. It auto files them. Start with one report today. Small step. Big control over your credit.

- Pull free report quarterly to spot errors

- Dispute online with templates—track 30 days

- Freeze free if risk, save PIN

- Opt out prescreen for less mail

- Monitor apps for free alerts

- Get written consent for job pulls

- Use 2025 AI for auto disputes

Conclusion

The Fair Credit Reporting Act protects you well. Free reports. Fast disputes. Privacy guards. Theft blocks. Denial notices. Job consents. In 2025, medical debt eases. Trigger leads stop. Know these. Use them. Dispute errors. Freeze smart. Monitor regular. If broken, report. Sue if big. Your credit stays fair. You hold the power.

FAQs

What is the Fair Credit Reporting Act?

FCRA is a law from 1970. It regulates credit reports. Makes sure info is accurate. Gives you rights to free reports and disputes. Updated over time. Covers bureaus like Equifax.

How do I get my free credit report under FCRA?

Go to AnnualCreditReport.com. One free per bureau each year. Or weekly now. Enter name and SSN. Download PDF. Check all three. Spot errors fast.

What if I find an error on my credit report?

Dispute it. Send letter or use online form. Add proof. Bureau checks in 30 days. Fix or delete if wrong. Get free update. Add your note if denied.

How does FCRA protect against identity theft?

Free weekly reports if victim. Fraud alert for 1 year. Freeze credit free. Blocks new accounts. Extended alert 7 years. File report with FTC for help.

Can I sue if FCRA is violated?

Yes. For damages. Up to $1,000 per willful break. Plus fees. Complain to CFPB first. Small claims easy. Log everything. Many settle out of court.