Credit Inquiries Explained: Smart Ways to Protect & Grow Your Credit

Whether you’re applying for a credit card, mortgage, car loan, or even renting an apartment, your credit report will likely be reviewed by a lender or landlord. One crucial component of that credit report is credit inquiries. While they may seem minor, understanding how inquiries work can help you better manage your credit profile, avoid unnecessary score drops, and be more strategic with your financial decisions.

In this detailed guide, we’ll explore what credit inquiries are, how long they stay on your report, the difference between hard and soft inquiries, how they affect your credit score, and what you can do to remove unauthorized or harmful inquiries.

What Are Credit Inquiries?

A credit inquiry occurs when a third party typically a lender, creditor, landlord, or employer checks your credit report. These inquiries help the inquiring party assess your financial responsibility and risk level. There are two types of inquiries: soft and hard.

- Soft Inquiries: These occur when your credit is checked for non-lending purposes. Examples include checking your own credit, pre-qualification offers, or employer background checks. Soft inquiries do not affect your credit score.

- Hard Inquiries: These happen when you actively apply for credit, like a loan or credit card. Hard inquiries are recorded on your credit report and can temporarily lower your credit score by a few points.

Understanding the difference between soft and hard inquiries is important because only hard inquiries affect your credit score and are visible to other lenders.

How Long Do Credit Inquiries Stay on Your Credit Report?

A common concern among consumers is: “How long will this inquiry affect my credit score?” The answer depends on whether the inquiry is soft or hard.

Hard inquiries remain on your credit report for up to 2 years. However, their impact on your credit score typically lasts only for the first 12 months. After that, although they still appear on your credit report, they generally no longer influence your credit score.

Credit scoring models like FICO and VantageScore acknowledge that people shop around for credit and therefore reduce the long-term penalty of inquiries. That said, excessive hard inquiries in a short span can still raise red flags to lenders.

Soft inquiries, on the other hand, may appear on your personal credit report but are not visible to lenders and have zero impact on your score.

How Long Do Credit Inquiries Last in Terms of Impact?

Many people ask: “How long do credit inquiries last?” The phrase can be interpreted two ways: duration of visibility on the report and duration of score impact.

- Duration on report: Hard inquiries stay for 2 years.

- Impact on score: They typically affect your credit score for 12 months.

This means the visible presence of the inquiry lingers longer than its actual impact on your creditworthiness. Credit bureaus automatically remove the inquiry from your report after the two-year period, with no action needed from you.

The small score drop caused by a hard inquiry (usually 5–10 points) typically rebounds within months if you maintain good credit behavior, such as paying bills on time and keeping credit utilization low.

Multiple Credit Inquiries Within 30 Days: Are They Harmful?

If you’re shopping around for a car loan, mortgage, or student loan, you might worry that submitting multiple applications will tank your score. Fortunately, credit scoring models are designed to account for this behavior.

When you apply for the same type of credit within a short period—usually 14 to 45 days depending on the scoring model all those inquiries are grouped into a single inquiry for scoring purposes. This means you can compare rates from multiple lenders without being penalized multiple times.

This practice is known as deduplication and exists to support smart financial behavior. For instance, applying to five different auto lenders within a 30-day window typically results in just one hard inquiry in the eyes of your credit score.

However, if you apply for different types of credit (e.g., a credit card and a car loan) around the same time, each will generate a separate hard inquiry, potentially causing a larger dip in your score.

When Do Credit Inquiries Fall Off Your Report?

All hard credit inquiries are automatically removed from your credit report 24 months after the date of the inquiry. This process is handled by the three major credit bureaus—Equifax, Experian, and TransUnion—and does not require any action on your part.

This timeline is consistent across all types of credit inquiries and ensures that outdated or irrelevant information doesn’t affect your financial profile indefinitely. Keep in mind that although inquiries stay on your report for two years, most lenders only focus on those made within the past 12 months when making lending decisions.

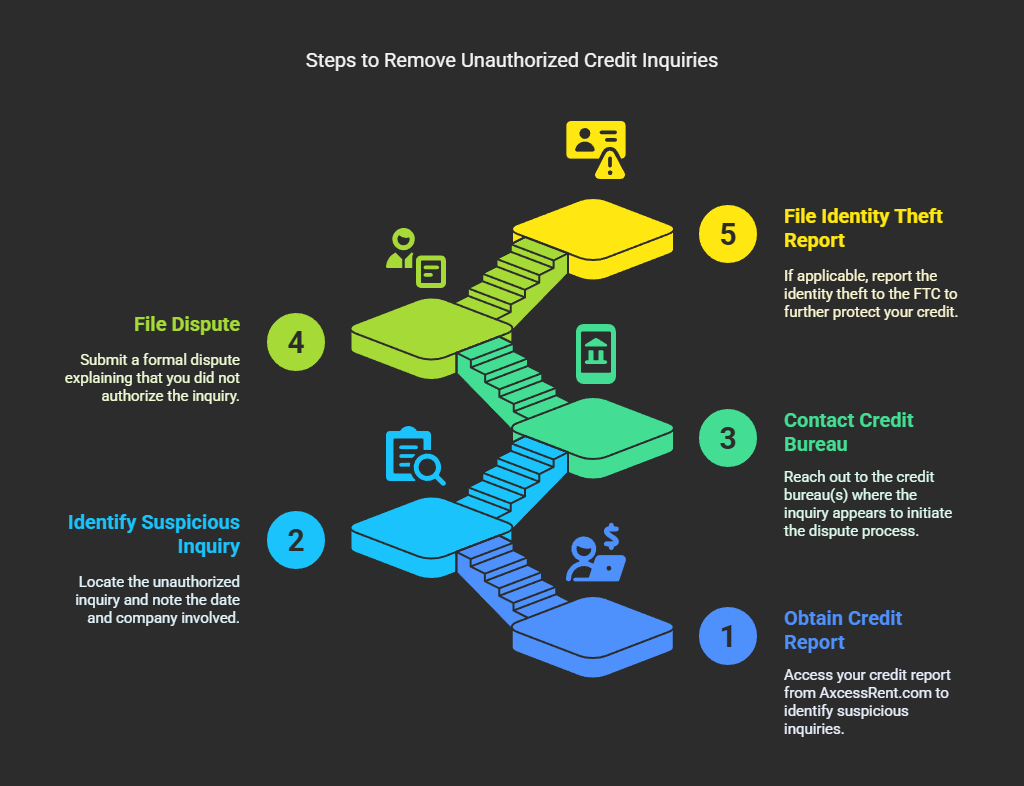

How to Remove Credit Inquiries from Your Report

If a hard inquiry was made without your knowledge or consent, you may be able to remove it from your credit report by disputing it. You cannot remove legitimate inquiries, but you can challenge those that:

- Were made due to identity theft

- Were duplicated

- Were unauthorized

Steps to Dispute a Credit Inquiry:

- Get your credit report from AxcessRent.com

- Locate the suspicious inquiry and note the date and company.

- Contact the credit bureau(s) where the inquiry appears.

- File a dispute explaining that you did not authorize the inquiry.

- If applicable, file an identity theft report with the FTC.

If your dispute is valid, the inquiry will be removed from your report, and you will receive a written confirmation.

Do Credit Inquiries Matter That Much?

In the grand scheme of credit scoring, credit inquiries make up only about 10% of your overall FICO score. This means they have a minor effect compared to:

- Payment History (35%)

- Credit Utilization (30%)

- Length of Credit History (15%)

- Credit Mix (10%)

That said, minimizing unnecessary hard inquiries can still help you maintain a healthier score. Avoid applying for multiple credit cards or loans unless necessary, and space out your applications to reduce impact.

Final Thoughts: Be Smart With Inquiries

Your credit health plays a crucial role in your financial future, and understanding how inquiries affect it can help you make smarter decisions. Whether you’re applying for a loan, renting an apartment, or opening a new credit card, being mindful of hard inquiries ensures you don’t unintentionally lower your score. Remember these key points:

- Hard inquiries stay on your credit report for two years, but their impact on your score diminishes after 12 months.

- Rate shopping works in your favor, multiple inquiries for the same type of loan (like a mortgage or auto loan) within a 14-45 day window are typically counted as a single inquiry.

- Monitor your credit regularly, if you spot unauthorized hard inquiries, you can dispute them to protect your score from fraud.

If you’re working to build or rebuild credit but want to avoid unnecessary hard inquiries or debt, AxcessRent offers a smart alternative. By reporting your on-time rent payments to major credit bureaus, AxcessRent helps you strengthen your credit history without applying for loans or credit cards. It’s a simple, risk-free way to turn your everyday rent payments into long-term credit growth.

Take control of your financial journey—minimize unnecessary inquiries, monitor your credit, and leverage tools like AxcessRent to build a stronger credit profile over time. With the right strategy, you can achieve your goals while keeping your credit score on the rise.

Build smarter. Grow faster. Rent, report, and rise with AxcessRent.