Budgeting Challenges & Savings Hacks for Renters

Introduction

Renting a home comes with financial challenges that can strain even the most disciplined budgeters. With rising rents, unpredictable expenses, and the pressure to balance living costs with savings, many renters find themselves struggling to stay financially secure.

Budgeting effectively isn’t just about cutting expenses it’s about making strategic choices that allow you to live comfortably while still saving for the future. Whether you’re dealing with irregular income, unexpected housing costs, or the desire to eventually buy a home, this guide will help you navigate the financial hurdles of renting.

In this comprehensive article, we’ll explore:

- The most common budgeting challenges renters face

- Smart strategies to manage rent and living expenses

- Creative savings hacks to maximize your money

- Long-term financial planning while renting

- How to build credit and avoid debt traps

- Resources and programs that can help ease financial burdens

By the end, you’ll have actionable steps to take control of your finances—even in a high-rent market.

Common Budgeting Challenges Renters Face

Rising Rent Costs

Rent prices have surged in many cities, often outpacing wage growth. According to recent data, the average rent in the U.S. has increased by X% over the past five years, while incomes have only risen by Y%. This imbalance forces many renters to spend over 30% of their income on housing—a threshold that financial experts warn can lead to financial instability.

When rent consumes too much of your paycheck, it leaves little room for savings, emergencies, or discretionary spending. Many renters find themselves in a cycle where they can barely cover their monthly expenses, let alone save for long-term goals like homeownership or retirement.

Utility & Hidden Housing Costs

Beyond rent, utilities and other hidden expenses can quickly add up. Electricity, water, gas, internet, and trash services are often overlooked when budgeting. Additionally, renters may face:

- Parking fees (especially in urban areas)

- Renter’s insurance (often required by landlords)

- Seasonal spikes in heating or cooling costs

- Maintenance costs (if landlords are slow to respond)

These expenses can vary month-to-month, making it difficult to stick to a strict budget.

Irregular Income Struggles

Freelancers, gig workers, and part-time employees face unique budgeting challenges. Unlike salaried workers, their income fluctuates, making it hard to predict how much they can allocate toward rent and bills each month.

To manage this, some renters:

- Estimate a monthly average based on past earnings

- Set aside a buffer fund for lean months

- Negotiate flexible rent due dates with landlords

Unexpected Expenses

Life as a renter comes with surprise costs, such as:

- Emergency repairs (e.g., broken appliances not covered by the landlord)

- Moving costs (security deposits, moving trucks, cleaning fees)

- Security deposit deductions (if landlords charge for damages)

Without an emergency fund, these unexpected expenses can lead to debt or financial stress.

Limited Savings Opportunities

When rent and utilities take up most of your income, saving becomes difficult. Many renters also feel pressure to:

- Furnish their apartments (leading to impulse purchases)

- Keep up with lifestyle trends in expensive neighborhoods

- Spend on convenience (takeout, subscriptions, etc.)

Over time, these habits can prevent meaningful savings growth.

Smart Budgeting Tips for Renters

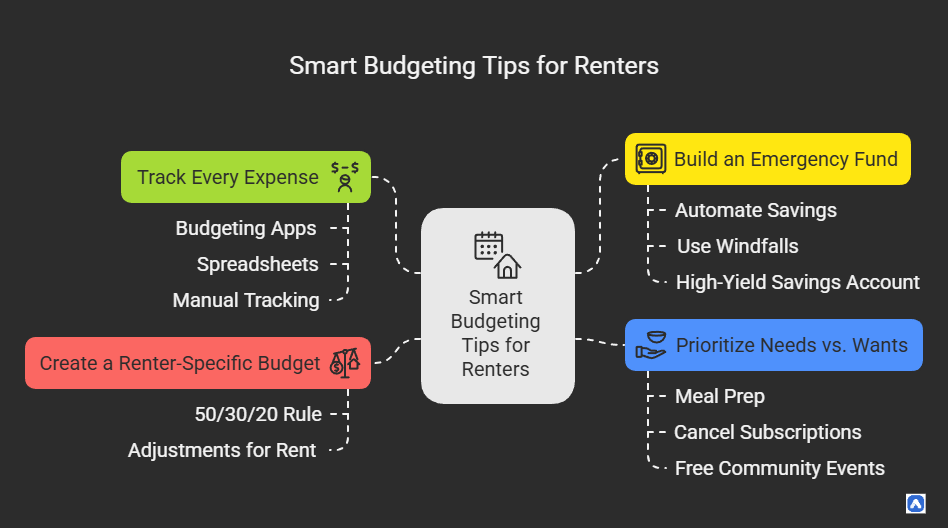

Create a Renter-Specific Budget

Traditional budgeting advice often doesn’t account for the unique circumstances of renters. Here’s how to create a budget that works for your situation. The 50/30/20 rule is a popular budgeting framework, but renters may need adjustments:

- 50% for essentials (rent, utilities, groceries, transportation)

- 30% for discretionary spending (entertainment, dining out)

- 20% for savings & debt repayment

If rent alone exceeds 30-40% of your income, you may need to cut discretionary spending to maintain savings.

Track Every Expense

Start by tracking every dollar you spend for at least one month. Many renters are surprised to discover how much they spend on convenience items like takeout food or ride shares when their kitchen or public transportation could serve the same purpose. Awareness is key. Use:

- Budgeting apps (Mint, YNAB, PocketGuard)

- Spreadsheets (Google Sheets, Excel)

- Manual tracking (receipts, bank statements)

Categorize spending into fixed (rent), variable (groceries), and discretionary (entertainment) to identify where cuts can be made.

Build an Emergency Fund

Automation is a renter’s best friend. Set up automatic transfers to savings accounts on payday so you’re not tempted to spend that money. Even small amounts add up over time and can help cover unexpected expenses that might otherwise derail your budget. Aim for 3–6 months’ worth of rent + living expenses. Start small:

- Automate savings (10–10–20 per week)

- Use windfalls (tax refunds, bonuses) to boost savings

- Keep funds in a high-yield savings account

This safety net prevents reliance on credit cards during emergencies.

Prioritize Needs vs. Wants

Don’t forget to budget for irregular expenses. Those once-a-year costs like security deposit renewals or annual insurance premiums can cause financial stress if you’re not prepared. Divide these annual costs by 12 and set aside that amount each month. To reduce unnecessary spending:

- Meal prep instead of ordering takeout

- Cancel unused subscriptions

- Use free community events for entertainment

Small changes add up over time.

Savings Hacks Every Renter Should Know

While you can’t control the rental market, you can control how you navigate it. Here are some often-overlooked strategies to reduce your housing expenses.

Timing your move can significantly impact what you pay. Rental prices often follow seasonal patterns, with higher demand (and higher prices) in summer months when families prefer to relocate. Moving during winter months might secure you a better deal, especially in colder climates where demand drops.

Consider alternative housing arrangements. Renting a room in a house rather than an entire apartment can dramatically lower costs. House-sitting arrangements can sometimes provide free or reduced-cost housing in exchange for property maintenance.

If you’re in a position to do so, negotiating your rent can be surprisingly effective. Landlords often prefer keeping a good tenant at slightly reduced rent rather than risking vacancy. Come prepared with market research showing comparable units at lower prices, and highlight your reliability as a tenant.

Negotiate Rent or Lease Terms

Many renters don’t realize rent prices aren’t always fixed. Before signing or renewing a lease, research comparable units in your area using sites like Zillow or Rentometer. If you find better deals, politely ask your landlord to match them. Offering to sign a longer lease (18-24 months) or pay multiple months upfront can also secure discounts. Timing matters—landlords are more flexible during slower rental seasons (winter months). Even a 50−50−100 monthly reduction saves 600−600−1,200 yearly.

Landlords may lower rent if:

- You sign a longer lease

- You pay a few months upfront

- You point out comparable cheaper rentals

Use tools like Zillow or Rentometer to research fair market prices.

Split Costs Strategically

Sharing expenses with roommates dramatically cuts housing costs. Beyond splitting rent, consider shared utilities, internet, streaming subscriptions, and bulk grocery purchases. Use apps like Splitwise to track shared expenses fairly. For solo renters, platforms like Neighbor let you rent unused storage space, while Airbnb allows short-term room rentals. Co-buying items like furniture or appliances with neighbors reduces individual costs. Always establish clear agreements upfront to avoid conflicts. Roommates can cut costs significantly. Consider:

- Shared utilities & internet

- Bulk grocery purchases

- Joint purchases (furniture, appliances)

Lower Utility Bills

Small habit changes lead to big savings on utilities. Replace incandescent bulbs with LEDs, install smart thermostats, and unplug idle electronics to cut electricity use. Seal drafty windows with weatherstripping and use heavy curtains to regulate temperature. Negotiate internet bills by comparing competitor rates—providers often offer retention discounts. Reduce water waste with low-flow showerheads and fix leaky faucets promptly. Reduce energy costs by:

- Using LED bulbs & smart power strips

- Sealing drafty windows

- Unplugging unused electronics

Furnish on a Budget

Furnishing an apartment doesn’t require debt or expensive stores. Scout thrift shops, Facebook Marketplace, and estate sales for quality secondhand furniture at 50-80% off retail. Join local “Buy Nothing” groups for free items. Focus on multifunctional pieces (e.g., storage ottomans) and prioritize essentials first. Save on furniture by:

- Shopping secondhand (Facebook Marketplace, thrift stores)

- DIY upcycling projects

- Borrowing or renting items

Use Rent Reporting to Build Credit

Services like AxcessRent report rent payments to credit agencies, improving your score over time. This builds positive payment history, which accounts for 35% of your FICO score. Over time, this can help qualify for better loans, credit cards, or even a mortgage. Some services also offer rent payment flexibility or cashback rewards.

Long-Term Financial Goals for Renters

Saving for Homeownership

If buying a home is part of your long-term plan, renting doesn’t have to delay that dream. Use your rental period to prepare financially. Start by saving for a down payment systematically. Treat it like another bill that must be paid each month. Even modest amounts add up over time, especially when invested wisely.

Even while renting, you can:

- Save for a down payment (set up automatic transfers)

- Improve credit (via rent reporting & on-time payments)

- Research first-time homebuyer programs

Investing While Renting

Use your rental period to improve your debt-to-income ratio. Paying down existing debt while renting will make it easier to qualify for a mortgage when you’re ready. Research first-time homebuyer programs in your area. Many offer down payment assistance or favorable loan terms that can make homeownership accessible sooner than you think.

Start small with:

- Robo-advisors (Betterment, Wealthfront)

- Index funds (low-cost, diversified options)

- Retirement accounts (Roth IRA, 401(k))

Smart Credit Card Use

While credit cards offer convenience and rewards, they can quickly lead to debt if misused especially when covering essential expenses like rent. Many renters are tempted to charge rent during tight months, but high processing fees (typically 2.5–3.5%) often negate any rewards earned. Instead, reserve cards for budgeted discretionary spending where you can pay the full balance monthly to avoid interest.

If your landlord accepts credit payments without fees, using a card with strong cashback or travel rewards can be strategic—but only if you already have the funds to pay it off immediately.

Boosting Income with Side Hustles & Career Growth

Renters facing tight budgets should explore ways to increase income rather than just cutting expenses. Side hustles like freelancing, gig economy jobs (Uber, DoorDash), or renting out unused space (parking, storage) can generate extra cash. If possible, invest in skill-building (online courses, certifications) to qualify for higher-paying jobs or promotions. Negotiating a raise or switching employers for better pay can have a bigger long-term impact than minor expense cuts. Allocate extra income toward debt repayment, investments, or savings goals—just be sure to balance work demands with personal well-being.

Conclusion

Renting presents financial challenges, but with the right strategies, it can be part of a healthy financial life. By implementing the budgeting techniques, cost-saving measures, and wealth-building approaches outlined in this guide, you can take control of your finances regardless of housing market conditions.

Remember that financial progress happens gradually. Small, consistent changes to your spending and saving habits will compound over time. Whether you plan to rent long-term or are saving for a home, these strategies will put you on firmer financial footing.

The most important step is to begin. Choose one or two strategies from this guide to implement this month, then gradually add more as they become habits. Your future self will thank you for the financial security you’re building today.