How to Rebuild Credit After Missed Payments: Fix it Now

Introduction: Why Rebuilding Credit Matters More Than Ever

If you’ve missed a few payments and your credit score has taken a hit, you’re not alone. Millions of Americans face financial setbacks every year, whether from unexpected medical bills, job loss, overspending, or simple oversight.

But here’s the truth: a bad moment in your financial life doesn’t have to define your future.

Your credit score is not a fixed number — it’s a reflection of your recent habits, and with the right plan, you can start moving it in the right direction within weeks. Learn how to rebuild credit after missed payments with proven strategies, expert tips, and AxcessRent’s rent reporting. Recover your score faster and smarter.

In this comprehensive guide, we’ll walk through:

- How missed payments hurt your score

- Exactly how long recovery takes

- Step-by-step actions to repair damage

- Proven techniques to speed up the process

- How AxcessRent’s Rent Reporting service can accelerate your recovery

By the end, you’ll have a clear, actionable plan to not only fix your score but make it stronger than before.

How Missed Payments Affect Your Credit Score

Why Payment History Is So Important

Your payment history makes up 35% of your FICO score — more than any other factor. Credit scoring models see missed payments as a sign of financial instability. Even a single 30-day late payment can drop a good score by 60–110 points.

The impact is bigger if:

- You have a high score to begin with (the higher you start, the harder you fall).

- You have multiple missed payments close together.

- The missed payment is on a major account like a mortgage or auto loan.

How Long Late Payments Stay on Your Report

- 30 days late: Shows up on your credit report but is less damaging if corrected quickly.

- 60 days late: Stronger negative impact and stays for 7 years.

- 90+ days late: Severe delinquency — often leads to collections or charge-offs, and recovery takes longer.

Important: The older a late payment is, the less it affects your score — but only if you start building positive history immediately.

How Missed Payments Snowball

Late payments can trigger:

- Penalty APRs on credit cards

- Overdraft fees if payments are auto-deducted without funds

- Collection actions from lenders

- Lower credit limits due to perceived risk

This creates a cycle where your score drops, interest rates rise, and borrowing becomes harder — making it more difficult to recover without a clear plan.

How Long Does It Take to Rebuild Credit After a Missed Payment?

The short answer: It depends on your starting point and your actions now.

- Minor damage (one missed payment): noticeable recovery in 3–6 months if all payments are on time moving forward.

- Moderate damage (multiple missed payments): 6–12 months for meaningful improvement.

- Severe damage (90+ days late, charge-offs, collections): 12–24 months for significant score restoration.

Pro Tip: Adding new positive data (like on-time rent payments) can dramatically shorten recovery time.

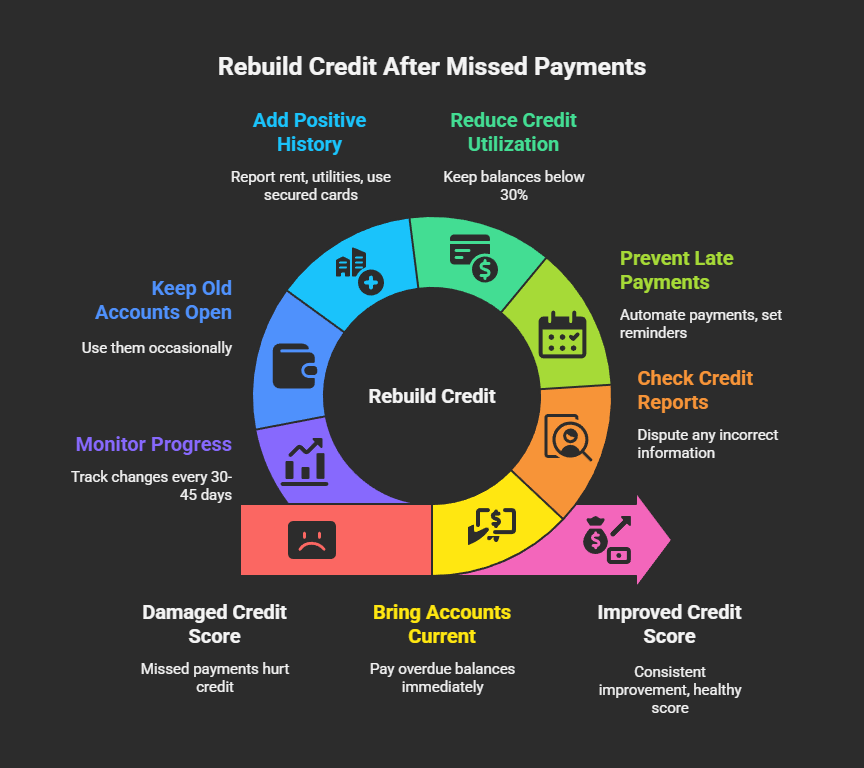

Step-by-Step Guide to Rebuild Your Credit After Missed Payments

Step 1: Bring All Accounts Current

If you’re still behind:

- Pay off overdue balances immediately.

- Call your creditors to explain the situation.

- Request a goodwill adjustment — some creditors may remove the late mark if you’ve been a reliable customer before.

Step 2: Check Your Credit Reports for Errors

You’re entitled to a free report from Experian, Equifax, and TransUnion every year via AnnualCreditReport.com.

Look for:

- Payments marked late when they weren’t.

- Duplicate negative entries.

- Accounts that don’t belong to you.

If you find errors:

- Dispute them online with documentation.

- Credit bureaus have 30 days to investigate.

Step 3: Prevent Future Late Payments

- Automate payments for at least the minimum due.

- Set calendar reminders a week before due dates.

- Link payments to a bank account with a small buffer to prevent overdraft.

Step 4: Reduce Credit Utilization

Credit utilization (your balance compared to your limit) makes up 30% of your score.

- Aim to keep balances below 30% (ideally 10% or less).

- If possible, make mid-cycle payments to lower reported balances.

Step 5: Add New Positive Payment History

Here’s the secret: scoring models reward recent, positive behavior.

Ways to do this:

- Rent Reporting: Services like AxcessRent can report up to 24 months of past rent and ongoing rent payments to credit bureaus.

- Utility Reporting: Some services let you report phone, electricity, and streaming payments.

- Secured Credit Cards: Make small purchases and pay them off in full every month.

Step 6: Keep Old Accounts Open

Closing old credit cards can shorten your credit history and raise your utilization. Keep them open and use them occasionally.

Step 7: Monitor Your Progress

- Use free tools like Credit Karma or Experian to track changes.

- Watch for improvements every 30–45 days.

How to Get Payment History Back to 100%

Your payment history percentage is the ratio of on-time payments to total payments.

To rebuild it:

- Avoid new late payments at all costs.

- Add more on-time payments by keeping multiple accounts active.

- Use rent reporting services to add 12–24 positive months instantly.

Example:

If you’ve made 35 payments with 1 late payment, your on-time rate is 97%. Adding 12 new on-time payments raises it to 98.5%, and 24 on-time payments takes it to 99.2%.

How to Increase Credit Score by 100 Points in 30 Days

While it’s not typical for everyone, some people can see a 100-point jump in a month if:

- They pay off large credit card balances.

- They successfully remove incorrect late payments.

- They add 12–24 months of positive rent payment history at once.

Can You Remove Late Payments from Your Credit Report?

Yes — but it’s not guaranteed.

Methods include:

- Goodwill Letter: Request removal from a lender you’ve been loyal to.

- Disputes: Challenge incorrect information.

- Pay for Delete: Negotiate with a collection agency (not all will agree).

How AxcessRent Helps You Rebuild Faster

AxcessRent gives you a unique advantage:

- Reports rent to all major credit bureaus.

- Can add past rent payments to give your score an instant boost.

- No loans, no extra debt — just credit-building from something you already pay.

Many clients see noticeable results in as little as 2–3 months.

Final Thoughts: Take Action Now, See Results Sooner

Rebuilding credit after missed payments isn’t about perfection — it’s about consistent improvement. Every on-time payment, every reduced balance, and every positive account moves you closer to a healthy score.

With services like AxcessRent’s Rent Reporting services, you can speed up recovery, add positive history instantly, and get back on track faster than relying on time alone.

Your financial future isn’t defined by a single mistake — and with the right plan, your credit comeback story can start today.

FAQs

1. How long does it take to rebuild credit after a missed payment?

The recovery time depends on how late the payment was, how many payments you missed, and your credit history before the mistake. For a single 30-day late payment, you might see improvements in 3–6 months if you make all future payments on time. For more serious delinquencies, such as 60- or 90-day late payments, recovery can take 12–24 months. Adding new positive payment history—such as rent reporting—can speed up the process. The key is to stop any future late payments, reduce credit card balances, and actively build your payment history.

2. How to get payment history back to 100%?

Your payment history percentage is calculated based on the ratio of on-time payments to total reported payments. To get back to 100%, you must stop all late payments immediately and start adding more positive ones. Over time, each new on-time payment reduces the weight of past mistakes. You can speed this up by adding accounts that report monthly—like credit cards, utilities, or rent reporting services. For example, if you have 35 total payments with one late mark, adding 12–24 new on-time payments quickly improves your percentage and strengthens your credit profile.

3. How to increase credit score by 100 points in 30 days?

While not guaranteed for everyone, a 100-point boost in 30 days is possible under the right conditions. Start by paying down high credit card balances to lower your credit utilization ratio, ideally under 10%. Dispute any errors or outdated late payments on your credit report. Add positive payment history—services like AxcessRent can back-report up to two years of rent payments. Becoming an authorized user on a well-managed credit account can also help. Combining these strategies can create a significant score increase in a short time, especially if your score has room for improvement.

4. How long until my credit goes back up after a missed payment?

The time it takes depends on your overall credit health and the severity of the missed payment. If it was a one-time, 30-day late payment, you may notice a partial rebound within 3–6 months by keeping future payments on time. More severe cases, such as 90-day lates or multiple missed payments, may require 12–24 months for significant improvement. The negative mark will stay on your credit report for up to seven years, but its impact lessens over time, especially if you consistently add positive data like rent or utility reporting to your credit profile.

5. Can you remove late payments from your credit report?

Yes, but it’s not always guaranteed. If the late payment was reported in error, you can file a dispute with the credit bureaus to have it removed. If it was legitimate but you’ve been a loyal customer, you can request a goodwill adjustment from the lender. In some cases, you can negotiate a “pay for delete” agreement with collection agencies, although this is less common with original creditors. Even if you can’t remove it, you can offset its effect by adding new positive payment history and keeping your accounts current to rebuild your score.

6. Does rent reporting really help rebuild credit?

Yes, rent reporting can be a powerful tool for rebuilding credit, especially if you have a limited credit history or recent negative marks. Rent is often your largest monthly expense, yet it doesn’t usually appear on your credit report. Services like AxcessRent report your on-time rent payments to major credit bureaus, adding consistent positive history to your profile. Some services can also back-report up to 24 months of past payments, giving your score an instant boost. While results vary, many people see noticeable improvements within 2–3 months of starting rent reporting.

7. How long does a missed payment stay on your credit report?

A missed payment can remain on your credit report for up to seven years from the date of delinquency. However, the impact on your credit score diminishes over time, especially if you build a record of on-time payments afterward. For example, a late payment from last month will have a greater effect than one from three years ago. Lenders care more about recent activity, so adding consistent positive payment history—such as through rent reporting—can help overshadow older late marks. The key is to avoid future late payments and actively strengthen your credit profile.

8. What’s the fastest way to fix a credit score after missed payments?

The fastest way is to combine several high-impact strategies. First, bring all accounts current and stop new late payments immediately. Second, lower your credit utilization by paying down credit card balances to under 10% of your limits. Third, add positive payment history through tools like rent reporting or secured credit cards. Fourth, dispute any inaccurate negative information with the credit bureaus. By combining these steps, you can see measurable improvements in just a few months, and in some cases, a significant score boost in as little as 30–60 days.