The Hidden Truth: Why Traditional Credit Building Fails Millions in 2025

When we talk about building credit, most advice boils down to one familiar phrase: “Get a credit card.” While this approach has worked for millions, it’s far from one-size-fits-all. In fact, relying solely on traditional credit building methods can leave many people behind, especially those with low income, limited credit history, or unique financial situations.

In this comprehensive guide, we’ll explore the limitations of conventional credit-building strategies like credit cards, highlight the groups that these methods fail to serve, and offer alternative solutions that make credit building more inclusive and accessible.

Understanding Traditional Credit Building Tools

Credit Cards

Credit cards are one of the most common tools recommended for building or improving a credit score. When used responsibly — such as paying off the balance in full each month and keeping usage below 30% of the credit limit — they can show lenders that you’re a reliable borrower. However, not everyone qualifies for a credit card, especially those with no credit history, low income, or past financial difficulties. Additionally, high interest rates and fees can quickly become burdensome if the balance isn’t managed properly.

Installment Loans

Installment loans include things like student loans, auto loans, and personal loans. These loans require you to repay a fixed amount over a set period. Making consistent, on-time payments helps build a solid payment history, which is a key factor in your credit score. But for many, taking on debt just to build credit can feel risky or counterproductive — especially if you’re trying to stay out of debt altogether or are recovering from previous financial challenges.

Authorized User Accounts

Becoming an authorized user on a friend’s or family member’s credit card is another method of boosting your credit. If the primary cardholder has a long history of on-time payments and low utilization, that positive activity can be reflected in your credit report. While this method doesn’t require you to apply for credit yourself, it still relies heavily on someone else’s financial behavior — and not everyone has access to someone willing to extend this type of support.

While these traditional credit building strategies do work for some, they can create unnecessary barriers for others. Whether it’s a lack of access, fear of debt, or not meeting strict approval requirements, many individuals are left looking for safer, more inclusive alternatives.

1. Not Everyone Can Qualify

To get a traditional unsecured credit card, you generally need a good credit score. But what if you don’t have a score at all? Millions of people in the U.S. are “credit invisible” or “unscorable.”

Who does this affect?

- Young adults

- Immigrants and newcomers

- Low-income individuals

- People who prefer cash-based lifestyles

For these groups, even secured credit cards — which require a cash deposit — may be out of reach due to financial instability or lack of trust in the system.

2. Credit Cards Can Be Risky

Using a credit card requires discipline. High interest rates, late fees, and the temptation to overspend can quickly lead to debt.

Real dangers include:

- Falling into a debt spiral

- Damaging your credit score with one missed payment

- Paying more in interest than you originally borrowed

For someone trying to build credit for the first time, this financial minefield can do more harm than good.

3. Cultural and Psychological Barriers

Not everyone is comfortable using credit. In some cultures or households, debt is seen as inherently negative. Others may have grown up watching family members struggle with bankruptcy, collections, or loan defaults.

These barriers can lead to:

- Fear of using credit tools

- Mistrust of financial institutions

- Avoidance of credit-building opportunities altogether

This isn’t about ignorance — it’s about trauma, values, and life experience.

4. Income Inequality Makes Access Unequal

Low-income individuals may not have enough disposable income to:

- Make a security deposit for a secured card

- Keep credit utilization low

- Pay off balances monthly

In short, traditional credit building methods assume a level of financial stability that simply doesn’t exist for everyone.

5. Limited Impact of Authorized User Status

Becoming an authorized user is often hailed as a quick credit fix, but it’s not guaranteed to help. Not all credit card companies report authorized users to credit bureaus, and even if they do, your score might not improve if the primary account holder has poor habits.

Plus, this method depends on having someone in your life who is financially responsible and willing to share their account with you — a luxury not everyone has.

6. Lack of Financial Education

Many people are encouraged to build credit before they fully understand how credit works. This can result in:

- Late payments due to confusion over due dates

- Maxed-out cards from misunderstanding credit limits

- Applying for multiple cards and triggering hard inquiries

Without proper financial education, traditional credit building tools can backfire.

Alternative Credit Building Options That Work for More People

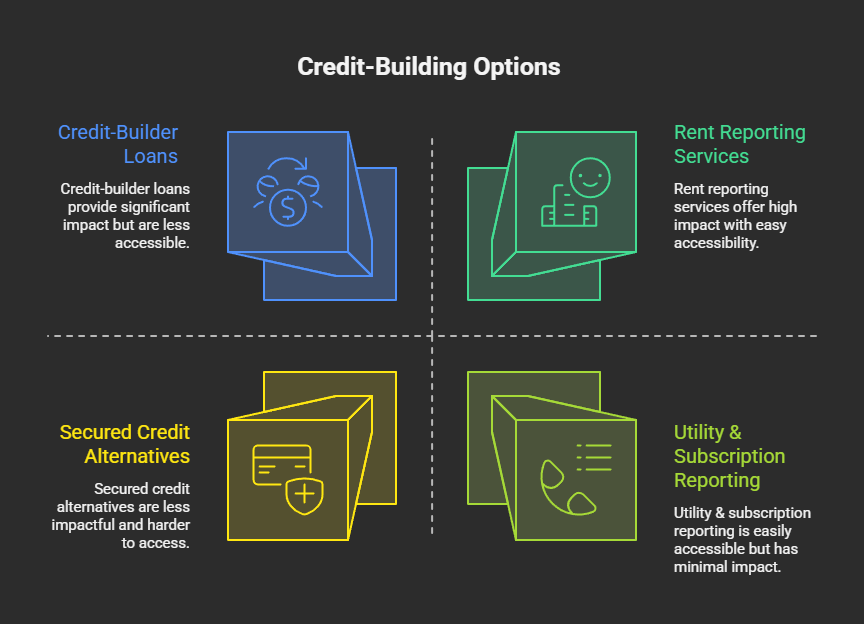

1. Rent Reporting Services Programs like AxcessRent and Experian Boost allow your rent payments to be included in your credit report. This is a powerful option for renters who reliably pay their landlord but don’t have other tradelines.

2. Credit-Builder Loans Offered by community banks and credit unions, these loans work in reverse: you make payments first, and then receive the loan amount at the end. These small payments are reported to credit bureaus, helping build positive history.

3. Utility & Subscription Reporting Some services allow you to include utility, phone, and even streaming service payments in your credit profile. These are everyday bills that you’re already paying on time — why not get credit for them?

4. Secured Credit Alternatives Some fintech companies now offer credit-building cards that don’t require a credit check or traditional security deposit. Instead, they may link to a bank account or require a small upfront payment.

5. Employer-Based Credit Programs Some employers offer financial wellness programs that include credit education, score monitoring, or even rent-reporting services as a benefit.

Who Benefits From These Alternatives?

These inclusive options are ideal for:

- College students without a credit history

- New immigrants

- Gig workers and freelancers

- People recovering from financial hardship

- Those with low or unpredictable income

They are also safer and more predictable than revolving credit, making them better for those who want to build credit without high risk.

Why This Matters in 2025 and Beyond

Access to credit is no longer a luxury. It’s a necessity for:

- Getting approved for rental housing

- Landing certain jobs

- Securing auto loans or mortgages

- Lowering insurance premiums

- Starting a business

If we continue to rely solely on traditional credit building tools, we risk leaving millions of responsible individuals behind — not because they’re untrustworthy, but because they’re underserved.

By expanding access to modern, low-risk credit-building methods, we open financial doors for more people and help reduce systemic inequality.

AxcessRent: A Modern Alternative to Traditional Credit Building

For those who want to avoid the complications of credit cards and still build credit reliably, AxcessRent is a game-changer. Unlike traditional credit building tools that often require debt or risky spending, AxcessRent helps you build credit simply by paying your rent on time. It reports your monthly rent payments directly to major credit bureaus, allowing renters to steadily grow their credit scores without taking out loans or opening new credit lines.

This makes AxcessRent an ideal solution for students, freelancers, immigrants, or anyone who wants to strengthen their credit profile without the stress of traditional credit building tools borrowing. In a world where why credit matters is becoming more important than ever, AxcessRent provides a smart, low-risk, and affordable path to financial credibility.

1. No Credit Cards or Loans Required

With AxcessRent, you don’t need to apply for a credit card or take out a loan just to build credit. It uses rent payments you’re already making — turning a necessary expense into a powerful financial tool.

2. Reports to Major Credit Bureaus

AxcessRent reports your monthly rent payments directly to the major credit bureaus (like Experian and TransUnion). This helps improve your credit score over time — just by paying rent on time.

3. Affordable and Transparent

Unlike many credit services, AxcessRent is budget-friendly with no hidden fees. It’s a practical solution for renters who want to build credit without breaking the bank.

4. Designed for Real People — Not Just Credit Experts

AxcessRent is built for everyday people — students, freelancers, immigrants, first-time renters — anyone who wants to build credit safely without needing to understand complex financial systems.

Final Thoughts

Credit cards and traditional loans have long been positioned as the gateway to building credit, but they aren’t a one-size-fits-all solution. Many people especially young adults, low-income earners, immigrants, or those recovering from financial setbacks, find these tools more limiting than empowering. Why should building a credit score require taking on debt or navigating complex interest structures? The truth is, credit should be accessible, fair, and reflective of real-life financial behavior not just your ability to manage revolving debt. It’s time we challenge outdated norms and stop assuming that swiping a credit card is the only path to financial credibility.

As financial technology continues to evolve, so do the opportunities to build credit in healthier, more inclusive ways. From rent reporting services like AxcessRent to alternative credit data models, we now have tools that reflect how people truly live and pay. The modern consumer deserves options that don’t rely on risk but reward responsibility. Whether you’re just starting your credit journey or trying to repair the past, you have choices that don’t force you into debt.

Remember: credit is a tool — and like any tool, the best results come when you choose the one that fits your hand, your lifestyle, and your goals.

FAQS

Why don’t credit cards work for everyone when building credit?

Credit cards often require a good credit score to qualify, charge high interest rates, and can lead to debt if not managed carefully. Many people may not feel comfortable using them or may not qualify at all.

Can I build credit without using a credit card?

Yes! You can build credit through alternatives like rent reporting, secured loans, credit builder accounts, or using services like AxcessRent that report rent payments to major credit bureaus.

Is rent reporting safe and reliable?

Absolutely. Rent reporting is a secure, regulated process. Services like AxcessRent use secure systems and data privacy standards to ensure your financial information stays protected.

Who benefits the most from non-traditional credit-building tools?

First-time renters, students, immigrants, low-income earners, and anyone recovering from financial hardship benefit most from alternatives that don’t require credit checks or debt.

Is rent reporting safe and reliable?

Absolutely. Rent reporting is a secure, regulated process. Services like AxcessRent use secure systems and data privacy standards to ensure your financial information stays protected.