Why did my credit score drop ? Common Traps and solutions

Introduction

You check your credit score and see it’s lower than last time. It’s frustrating, especially if nothing seems wrong. Credit scores can drop for many reasons, some obvious, others not. In 2025, with high interest rates and economic pressures, scores are falling faster than usual. Gen Z has seen the biggest drops, often from student loans.

Your credit score is a key to financial doors: loans, rentals, even jobs. A lower score could mean higher interest rates or outright denials. This article dives into 9 possible reasons your credit score dropped. Each reason includes a detailed explanation, a real-world example, and practical fixes. We’ll also cover how to check your score and prevent future drops. By the end, you’ll have a clear path to recovery.

Credit scores, like FICO (used in 90% of lending decisions) or VantageScore, rely on your credit report from Equifax, Experian, and TransUnion. Five factors drive your score: payment history (35%), amounts owed (30%), credit history length (15%), new credit (10%), and credit mix (10%). Changes in these cause drops. Let’s explore why.

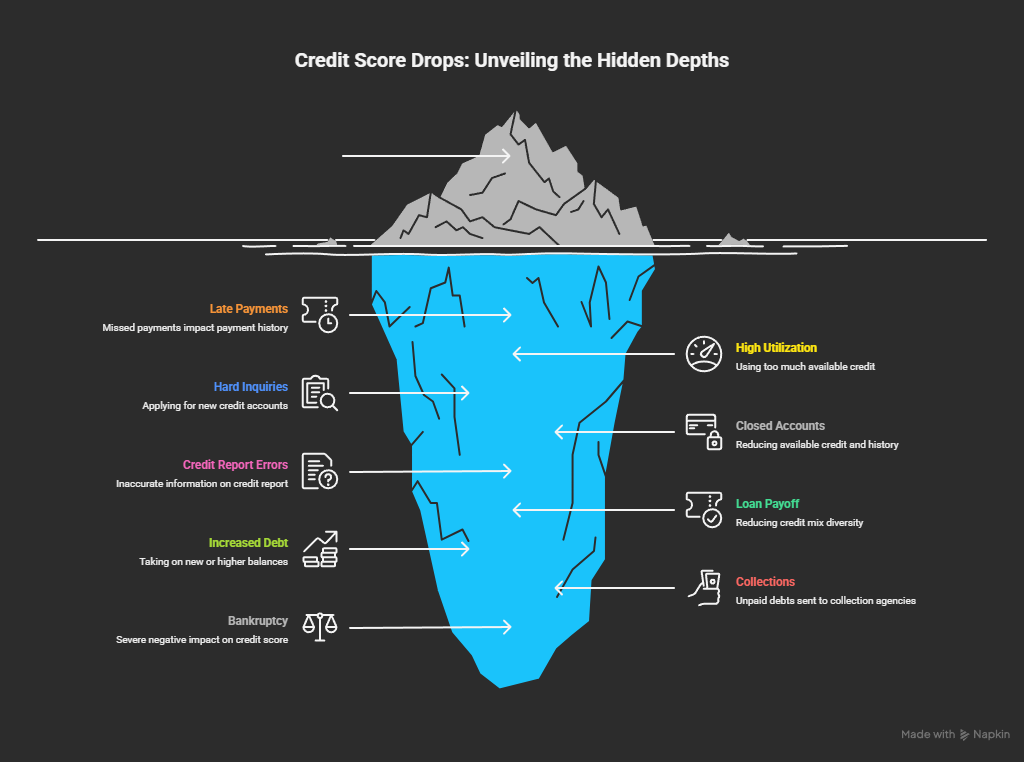

9 Possible Reasons Your Credit Score Dropped

1. Late or Missed Payments

What Happens

Late payments, especially those 30+ days overdue, are reported to credit bureaus, heavily impacting payment history (35% of your FICO score). A single missed payment can slash your score by 100+ points, signaling unreliability to lenders. These marks stay on your report for seven years, even if paid later.

Real-World Example

Sarah, 28, missed a $200 credit card payment during a hectic move. Her score plummeted from 720 to 650. Despite her solid history, this single oversight caused a significant drop, showing how critical timely payments are.

How to Fix It

Set up autopay or calendar reminders to avoid missing due dates. If late, pay immediately and request a goodwill adjustment from the lender. Build consistent on-time payments to rebuild your history over time.

2. High Credit Utilization

What Happens

High credit utilization—using over 30% of your available credit—signals financial strain, affecting 30% of your score. A sudden balance spike, like maxing out a card, can drop your score 20-50 points. Lenders view high ratios as risky, reducing your chances for favorable loan terms.

Real-World Example

Mike, 35, charged $4,000 on a $5,000-limit card for medical bills. His utilization jumped to 80%, dropping his score from 740 to 690. The high ratio hurt despite his good payment history.

How to Fix It

Pay down balances quickly, starting with high-interest cards. Request a credit limit increase to lower utilization. Keep usage below 10% for optimal scores. Budget to avoid overspending.

3. Hard Inquiries from New Credit

What Happens

Applying for loans or cards triggers hard inquiries, lowering your score by 5-10 points each (10% of score). Multiple inquiries in a short period signal desperation, increasing risk perception. They stay on your report for two years but only affect your score for one year.

Real-World Example

Anna, 42, applied for three credit cards in a month to cover expenses. Her score dropped 25 points from 710 to 685, and she was denied one card due to excessive inquiries.

How to Fix It

Group loan applications within 14-45 days to count as one inquiry. Use pre-qualification tools for soft checks. Limit applications to essential needs and space them out to minimize impact.

4. Closing Old Accounts

What Happens

Closing old credit accounts reduces available credit, raising utilization if balances remain. It also shortens your credit history (15% of score), as older accounts add stability. This can drop your score 10-30 points, especially if the closed account was one of your longest-standing ones.

Real-World Example

Tom, 50, closed a 15-year-old credit card after paying it off, thinking it was unnecessary. His utilization rose, and history shortened, dropping his score from 760 to 730.

How to Fix It

Keep old accounts open, using them occasionally for small charges. If fees are high, downgrade to no-fee cards. Rebuild history with responsible credit use over time.

5. Errors on Your Credit Report

What Happens

Errors like incorrect late payments or fraudulent accounts can tank your score. Identity theft adds unauthorized debt, misrepresenting your creditworthiness across multiple score factors. Such inaccuracies can drop your score significantly until corrected, often requiring disputes with bureaus to restore your financial reputation.

Real-World Example

Lisa, 31, discovered a credit card she never opened on her report due to identity theft. Her score fell 80 points from 680 to 600 until she disputed the error.

How to Fix It

Check reports free at AnnualCreditReport.com. Dispute errors online or by mail with evidence. Freeze your credit to prevent fraud. Monitor regularly to catch issues early.

6. Paying Off a Loan

What Happens

Paying off a loan can reduce your credit mix (10% of score), especially if it’s your only installment loan. A less diverse profile appears riskier, causing a temporary score drop of 10-20 points. Scores recover as you maintain other credit types with strong payment habits.

Real-World Example

David, 45, paid off his car loan, his only installment loan. His score dipped 15 points from 750 to 735 due to reduced credit mix, despite his otherwise strong profile.

How to Fix It

This is temporary. Keep other accounts active, like credit cards. If needed, consider a small loan later, but only if manageable. Focus on timely payments to recover.

7. Increased Debt or New Balances

What Happens

Taking on new debt, like a loan or card balance, increases your amounts owed (30% of score). Higher balances raise utilization, and new loans add debt before positive history builds, potentially dropping your score 20-50 points until payments establish reliability.

Real-World Example

Emily, 26, took out a $10,000 student loan. The new debt raised her utilization, dropping her score from 670 to 630, a common issue for Gen Z in 2025.

How to Fix It

Pay extra on high-interest debts using the avalanche method. Budget to avoid new borrowing. Keep utilization low by paying balances monthly and monitoring spending habits.

8. Collections or Charge-Offs

What Happens

Unpaid debts sent to collections or charged off as uncollectible are major negatives, dropping scores 100+ points. These marks, affecting payment history, stay on your report for seven years, signaling high risk to lenders and making approvals harder or costlier.

Real-World Example

John, 38, ignored a $500 medical bill, which went to collections. His score crashed from 700 to 590, hurting his chances for a car loan until he settled the debt.

How to Fix It

Pay or negotiate collections. Request pay-for-delete agreements. Prevent future issues by addressing bills early, setting up payment plans, or seeking financial counseling if needed.

9. Bankruptcy or Public Records

What Happens

Filing bankruptcy or facing judgments like liens devastates your score, dropping it 130-240 points. These severe negatives, impacting payment history and overall risk, stay on reports for 7-10 years, making borrowing difficult and costly until rebuilt over time.

Real-World Example

Rachel, 55, filed bankruptcy after a job loss. Her score plummeted from 720 to 520, limiting her options for years until she rebuilt with secured cards and timely payments.

How to Fix It

Use secured cards to rebuild. Make all payments on time. Seek nonprofit credit counseling. Avoid further public records. Expect slow recovery over several years.

How to Check Why Your Credit Score Dropped

Don’t guess—investigate. Get free weekly credit reports from AnnualCreditReport.com to spot changes like late payments or new accounts. Apps like Credit Karma or Experian send alerts for score drops. Compare old and new reports to pinpoint the cause, such as a new inquiry or error.

Steps to Recover from a Credit Score Drop

Recovery is possible with focus.

- Address the Cause: Pay overdue bills, reduce balances, or dispute errors.

- Build Positive History: Pay on time, keep utilization below 30%.

- Monitor Progress: Check scores monthly via free apps.

- Be Patient: Improvements take 3-6 months, sometimes longer for severe issues.

In 2025, with 4% of accounts delinquent (per FICO), consistent habits are key.

Preventing Future Credit Score Drops

Stay proactive to avoid drops.

- Automate Payments: Ensure no missed due dates.

- Keep Utilization Low: Below 30%, ideally 10%.

- Limit Inquiries: Apply only for necessary credit.

- Check Reports Quarterly: Catch errors early.

- Build an Emergency Fund: Avoid relying on credit for surprises.

An emergency fund of $1,000 can prevent maxing out cards.

Conclusion

A credit score drop can sting, but the 9 reasons—late payments, high utilization, inquiries, and more—have fixes. Real stories like Sarah’s or Lisa’s show it’s common and manageable. Check your report, address issues, and build good habits. In 2025’s tough economy, a strong score opens doors. Start your recovery today.

Frequently Asked Questions

why did my credit score drop after paying off debt ?

Paying off a debt can reduce your credit mix or shift utilization, causing a temporary 10-20 point drop. Maintain other accounts and continue timely payments to recover quickly.

Why Did My Credit Score Drop for No Reason?

It’s rarely “no reason.” Check for unreported changes like limit cuts, new inquiries, or errors. Timing of bureau updates can also affect scores. Review reports to confirm.

Why Did My Credit Score Drop 20 Points?

A 20-point drop often comes from a hard inquiry, small balance increase, or reporting delay. Check your report for specifics and address issues like high utilization promptly.

Can Medical Debt Cause My Credit Score to Drop?

Yes, unpaid medical bills sent to collections can drop scores, though 2025 FICO rules reduce small medical debt impact. Pay or negotiate bills to avoid collections.

Why Did My Credit Score Drop After Closing a Credit Card?

Closing a card raises utilization and shortens credit history, dropping scores 10-30 points. Keep old accounts open with minimal use unless high fees justify closure.