What Revolving Credit ?: Pros, Cons, and Easy Management

Introduction

Revolving credit shows up in many wallets. It powers credit cards and lines of credit. People use it for daily buys or emergencies. But it can help or hurt your finances.

This guide explains revolving credit. We cover what it is. How it works. Types you might see. Differences from other credit. Effects on your score. Pros and cons. Tips to handle it.

You get actionable steps. Real examples. Data from 2025. By the end, you know how to use revolving credit right. Let’s start.

Revolving Credit Definition

Revolving credit is a loan type. You get a credit limit. Borrow up to that amount. Pay some back. Borrow again. No need for a new application each time.

Think of it like a tab at a store. You charge items. Pay part each month. The tab stays open. Lenders set the limit based on your income and credit.

In 2025, revolving credit makes up most consumer debt. Balances hit $1.1 trillion in July. It grew 9.7% that year. People lean on it for flexibility.

How Revolving Credit Works

You apply once. Get approved for a limit, say $5,000. Spend $1,000 on groceries. Your balance is $1,000. Available credit drops to $4,000.

Each month, pay at least the minimum, often 2-3% of balance plus interest. Pay more to cut debt faster. Unused limit stays ready.

Interest accrues on unpaid balances. Rates average 20-25% in 2025. Pay in full by due date. Avoid interest.

Lenders report to bureaus like Equifax. This builds your history.

Key Terms in Revolving Credit

- Credit Limit: Max you can borrow.

- Balance: What you owe now.

- Utilization Ratio: Balance divided by limit. Key for scores.

- Minimum Payment: Least you must pay monthly.

- Grace Period: Time to pay without interest, often 21-25 days.

Know these. They guide your choices.

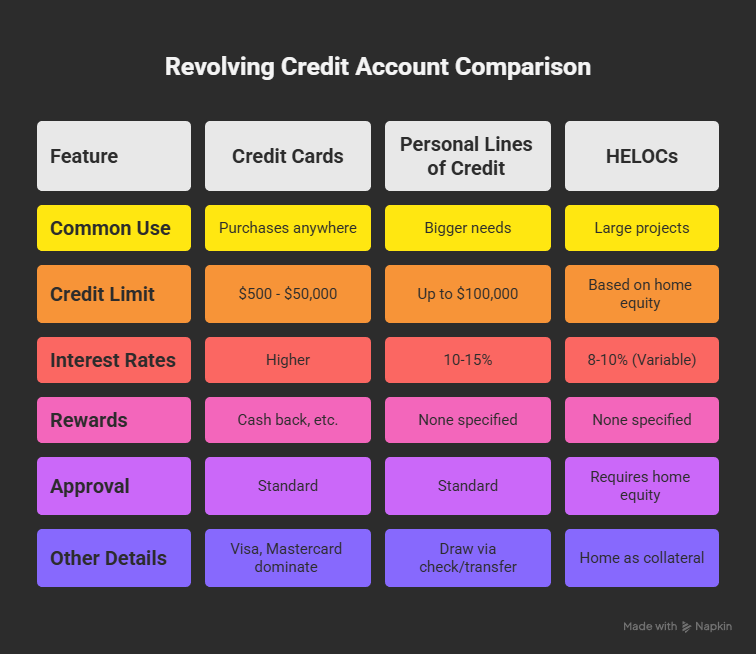

Types of Revolving Credit Accounts

Not all revolving credit looks the same. Common types fit different needs.

Credit Cards

Most people know these. Use for purchases anywhere. Limits from $500 to $50,000. Many offer rewards like cash back.

Visa and Mastercard dominate. In 2025, 80% of adults have one. Good for building credit if used right.

Personal Lines of Credit

Like a card but for bigger needs. Unsecured or secured. Limits up to $100,000. Draw funds via check or transfer.

Rates lower than cards, around 10-15%. Use for debt consolidation or home repairs.

Home Equity Lines of Credit (HELOCs)

- Tied to your home value. Borrow against equity. Limits based on home worth minus mortgage.

- Variable rates, often 8-10% in 2025. Risk: Home as collateral. Good for large projects.

- Other types include store cards. They limit to one retailer. Easier approval but higher rates.

Pick based on your goals. Cards for daily use. Lines for flexibility.

Is a credit card installment or revolving?

Credit comes in two main forms. Revolving and installment. They differ in use and repayment.

- Revolving credit lets you borrow repeatedly. No fixed end. Pay minimums. Balance changes.

- Installment credit gives a lump sum upfront. Fixed payments over time. Like a car loan. Once paid, it’s done.

Key Differences

| Aspect | Revolving Credit | Installment Credit |

|---|---|---|

| Borrowing | Ongoing up to limit | One-time lump sum |

| Repayment | Flexible minimums | Fixed monthly payments |

| Term | Open-ended | Set term (e.g., 5 years) |

| Examples | Credit cards, HELOCs | Mortgages, auto loans |

| Interest | Variable, on unpaid balance | Fixed or variable on full amount |

Revolving suits short-term needs. Installment for big buys. Mix both for better scores.

Which Is Better for Your Credit?

Both revolving and installment credit help your score. Revolving affects it more through daily use and utilization. Installment adds variety to your mix. Aim for one of each. That can boost your mix factor by 10% of your total score.

How Revolving Credit Affects Your Credit Score

Scores go from 300 to 850. Revolving credit hits 30% of that via utilization. Payments make up 35%. History length 15%. New credit 10%. Mix 10%. Keep revolving in check to lift your score.

Credit Utilization Ratio

It packs the biggest punch. Divide total balances by all limits. Stay under 30% for best results. Over 50% can cut your score by 50 to 100 points. Say you have $10,000 limits and $2,000 owed. That’s 20%. Solid. Pay it down quick. Scores refresh each month.

Payment History

Skip payments and your score drops hard. Late notes stick around 7 years. Pay on time to build trust with lenders. In 2025, delinquency rates stayed high at 4.4% in Q2. Keep up to avoid trouble.

Credit Mix and New Accounts

Pair revolving with installment for a better mix. But skip too many new revolving accounts. They add inquiries that hurt. Stick to one a year. New ones shorten your average age too. Hold off if you can. Check free reports at AnnualCreditReport.com to track it.

Pros and Cons of Revolving Credit

Revolving credit gives options but comes with risks. Look at both sides before you dive in.

Pros

- Flexibility: Pull money when you need it. No new applications each time.

- Build Credit: Pay on time and watch your score climb.

- Rewards: Many cards offer cash back or points on buys.

- Emergency Buffer: It covers unexpected hits like repairs.

- Lower Unused Interest: You only pay on what you borrow.

It works well for steady, planned spending.

Cons

- High Rates: APR over 20% adds up if you carry a balance.

- Overspending Risk: Limits tempt you to spend too much.

- Utilization Trap: Big balances drag your score down.

- Fees: Late or over-limit charges stack quick.

- Debt Cycle: Minimum payments keep you in the hole longer.

Handle it with care. Or it can hurt.

Tips for Managing Revolving Credit

Take control of revolving credit. Skip the traps. Use these steps to stay ahead.

Pay More Than Minimum

The minimum just covers interest and a little principal. Go for the full balance each time. It cuts fees and drops your utilization. Set up autopay to hit the full amount.

Keep Utilization Under 30%

Watch your balances close. Pay mid-cycle if you creep near the limit. Apps like Mint send tracking alerts. Ask for a limit raise once a year. It lowers your ratio without extra debt.

Use for Needs, Not Wants

Stick to basics like groceries or gas. Pass on impulse stuff. Set a budget first. Tie the card to one spending area only.

Monitor Statements

Check each month for mistakes. Dispute wrong charges right away. Keep the card out of sight in your wallet. That cuts down on random swipes.

Build Positive Habits

If you’re new, start with a secured card. In 2025, tools like Credit Karma give real-time alerts. Pay twice a month to keep ratios low.

Avoid Closing Old Accounts

Closing kills your payment history. It shrinks limits and hikes utilization. Leave them open. Charge something small once a year to keep them active.

Common Mistakes to Avoid with Revolving Credit

Mistakes hit your wallet and score. Avoid these to stay safe.

- Carry balances month to month. Interest builds fast.

- Max out your limits. It wrecks your utilization.

- Miss due dates. One late can drop your score 100 points.

- Apply for too many at once. Inquiries pile up and hurt.

- Co-sign without a backup plan. It links your score to someone else’s mess.

Others learned the hard way. Missed payments in 2025 cost people plenty.

What Happens If Revolving Credit Goes Wrong?

If balances climb, don’t wait. You have fixes ready.

- Debt consolidation: Roll it into a loan with a lower rate.

- Balance transfer: Shift to a 0% promo card for breathing room.

- Counseling: Groups like NFCC offer free advice from pros.

Last resort is bankruptcy. It wipes debt but marks your score for 7 to 10 years. Step in early. Call your lender.

Conclusion

Revolving credit fits right into daily life. It lets you buy groceries or fix a car. It can build your credit score if you use it right. But without good habits, it leads to debt that sticks around.

You have the full picture now. We covered the types, like cards and lines of credit. We compared it to installment loans. We looked at how it affects your score, especially utilization. And we shared tips to keep it under control.

Start small today. Pull up your credit report. Check your limits and balances. Pick one card and pay it down. Watch how your utilization drops. Use free tools like AnnualCreditReport.com to track changes each month.

It takes time, but it works. Pay on time every month. Keep balances low. That raises your score step by step. In a few months, you might see better rates on loans.

Think about your goals. Want a house? A car? Good credit opens those doors. Revolving credit is a tool. Use it to get there, not hold you back.

If you slip, fix it quick. Talk to a counselor at NFCC. They help for free. Or try a balance transfer to cut interest.

Keep at it. One change leads to more. Your finances get stronger. You can handle this.

Frequently Asked Questions About Revolving Credit

What counts as revolving credit?

It covers credit cards, personal lines of credit, and HELOCs. Any account where you reuse a limit counts. Store cards fit too. They let you borrow, pay back, and go again.

Does revolving credit build credit faster than installment?

It might if you handle utilization and payments well. It shows lenders your day-to-day habits. But blend both for top results. Installment brings needed variety to your mix.

Can I have too much revolving credit?

Sure. A bunch of accounts flags you as risky to lenders. It adds inquiries and cuts your average age. Keep it to 2 or 3 max. Low utilization across them keeps scores healthy.

How often should I check my revolving balances?

Do it weekly to hold under 30% utilization. Set alerts for 80% full. That stops score dips and interest shocks. Monthly checks spot errors early too.

Is revolving credit good for emergencies?

It works as a fast safety net for things like car fixes. But pay it back soon. That skips the high-interest loop. Pair it with a cash emergency fund if you can.