FICO Score Explained: Types, Ranges, and How to Check Yours for Free

Think of your FICO Score as a financial passport—the key that decides which opportunities you can unlock, from renting an apartment to securing a mortgage or even landing the best credit card offers. But here’s the surprising part: there isn’t just one FICO Scores. In fact, there are dozens of versions, each tailored for different lenders and purposes. This often leaves people wondering: Which score really matters? Why are there so many? And how does it affect my financial future?

In this guide, we’ll break it all down in simple terms so you can finally understand what a FICO Score is, how it works, and why it plays such a critical role in your financial life.

What is a FICO Score?

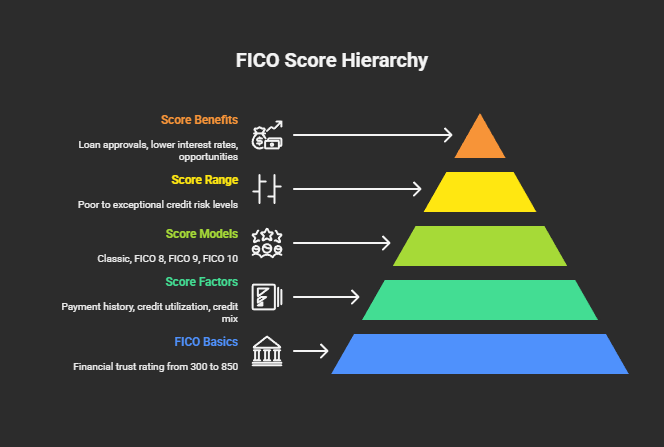

A FICO Score is basically your financial trust rating. It’s a three-digit number, usually ranging from 300 to 850, that tells lenders how risky (or safe) it might be to lend you money. Think of it as your financial reputation condensed into a single number.

It was developed by the Fair Isaac Corporation (FICO) in 1989, and ever since, banks, credit card companies, and even landlords have been using it as a quick way to judge how reliable you might be.

Imagine you’re lending money to a friend. If they always pay you back on time, you’d feel safe lending them again. If they forget, stall, or never pay you back, you’d think twice. That’s essentially how a FICO Score works for lenders — it’s a risk predictor.

Your score is based on five main factors:

- Payment history (do you pay on time?) – 35%

- Credit utilization (how much of your credit are you using?) – 30%

- Credit history length – 15%

- New credit (are you applying for lots of new accounts?) – 10%

- Credit mix (do you have a healthy mix like credit cards, loans, mortgages?) – 10%

The higher your score, the better the chances of getting approved for loans, credit cards, and even securing lower interest rates.

How Many FICO Scores Are There?

This question often surprises people. There isn’t just one FICO Score — there are actually dozens of them.

Here’s why: lenders and industries want scores tailored to their needs. For example, an auto lender cares more about your past car loan payments than your history with credit cards. A mortgage lender, on the other hand, wants a broad picture of your entire financial reliability.

Currently, there are at least 16 versions of the “classic” FICO Score models, plus industry-specific versions for auto loans, credit cards, and mortgages. When you hear someone say “my FICO Score,” they usually mean the most commonly used model, FICO Score 8.

So if you check your score in one place and it looks slightly different in another — don’t panic. You’re probably looking at different FICO versions.

How Many FICO Score Models Are There?

There are multiple FICO Score models, and each one has updated versions, kind of like software upgrades.

- Classic FICO Scores: These are the ones lenders most commonly use. Versions range from FICO Score 2 all the way up to FICO Score 10.

- FICO Score 8: Still the most widely used model today.

- FICO Score 9: Updated to be more forgiving with medical debt.

- FICO Score 10 and 10T: The newest versions, using something called “trended data” (looking at your credit behavior over time, not just a snapshot).

Add to this the industry-specific models, and you end up with dozens of different FICO Scores floating around.

A key thing to remember: you don’t need to know every model. What matters is knowing that lenders may see a slightly different number than what you see when you check your score.

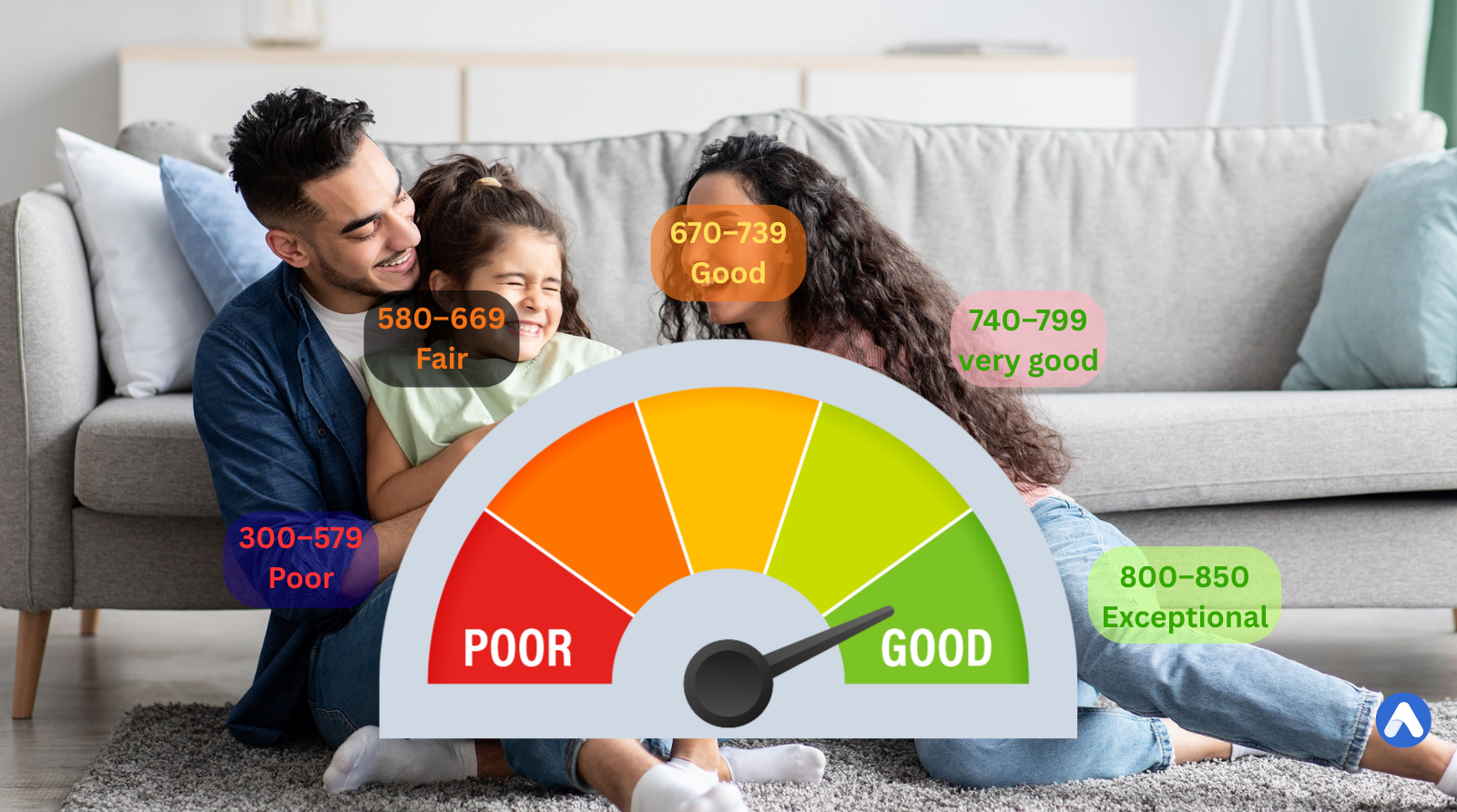

What is the FICO Score Range?

The FICO Score range is 300 to 850, and here’s how lenders typically view it:

- 300–579: Poor – High risk. Getting approved for credit is very tough.

- 580–669: Fair – Below average. You might get approved, but interest rates will be higher.

- 670–739: Good – Average to slightly above. Most lenders will see you as a safe bet.

- 740–799: Very Good – You’ll likely get approved for loans with favorable rates.

- 800–850: Exceptional – The best of the best. You’re considered extremely low-risk.

Real-life example: If you’re at 740, you might get a car loan at 5% interest. But at 620, you could be looking at 11% or higher. Over the life of a loan, that difference can cost you thousands of dollars.

What is a Good FICO Score?

Most people ask this because they want to know where they stand. A good FICO Score generally starts at 670 and above.

But here’s the trick: “good” is relative to what you need.

- If you’re applying for a credit card, a score of 680 might be enough.

- For a mortgage, lenders may want to see 720 or higher for the best interest rates.

Think of it like grades in school. A “B” might get you into college, but if you want Harvard, you’ll probably need an “A.”

What is FICO Score 8?

FICO Score 8 is the most commonly used version of the FICO model. Lenders still rely on it heavily even though newer versions exist.

Key points about FICO Score 8:

- More sensitive to high credit card balances. If you’re maxing out your cards, expect a drop.

- More forgiving of isolated late payments. If you miss once but generally pay on time, it won’t tank your score as much.

- Widely adopted across banks, credit card issuers, and personal loan companies.

So if you check your score and it says “FICO 8,” you’re looking at the most popular benchmark.

What is My FICO Score?

When people say “my FICO Score,” they usually mean the number they got from a credit monitoring service, bank, or directly from MyFICO.com (FICO’s official service).

The thing is, you don’t just have one FICO Score. Remember, there are multiple versions and industry-specific ones. So your “my FICO Score” could look like:

- FICO Score 8 from Experian: 715

- FICO Score 9 from TransUnion: 728

- Auto Score from Equifax: 702

Don’t stress over small differences. The key is keeping your overall habits healthy — paying on time, keeping balances low, and avoiding unnecessary hard inquiries.

How Many FICO Scores Do I Have for Free?

Many people ask, “Where can I check my FICO Score for free?”

Here are some popular ways:

- Discover, American Express, Bank of America, Citi, and Chase all provide free FICO Scores to cardholders.

- Some banks give you access through online banking.

- You can also get a free credit report (not your FICO Score, but still useful) at AnnualCreditReport.com.

Pro tip: Always check whether you’re getting a FICO Score or a VantageScore (another credit scoring model). They’re not the same, though they measure similar things.

FICO Score vs Credit Score: What’s the Difference?

This is where people get confused. All FICO Scores are credit scores, but not all credit scores are FICO Scores.

- FICO Score → The most widely used credit scoring brand.

- Credit Score → A broader term. Could be a FICO Score, a VantageScore, or even a lender’s custom in-house model.

Think of it like this: “Soda” is the general category. “Coke” is a specific brand. Similarly, “credit score” is the general category, and “FICO” is the most trusted brand.

Final Thoughts: Why FICO Scores Matter

At the end of the day, your FICO Score is a key to opportunity. It can decide whether you get approved for a mortgage, the interest rate on your car loan, or even whether a landlord chooses you over another tenant.

But don’t let the numbers intimidate you. They’re not a mysterious code you’ll never crack. They’re simply a reflection of your financial habits. By:

- Paying bills on time

- Keeping credit card balances low

- Building a mix of credit responsibly

- Avoiding unnecessary applications

…you’ll watch your FICO Score grow steadily.

Remember, it’s not about being perfect. It’s about being consistent. Over time, small smart choices add up to a big difference in your financial freedom.