What is consolidate debt and How Does it Work?

For many people, the path to financial freedom is littered with high-interest credit cards, multiple personal loans, and scattered monthly payments. It can feel overwhelming and impossible to track.

This is where consolidate debt enters the picture. Consolidation is the act of wrapping several smaller debts into one single, larger debt, often with a different lender, a lower interest rate, and a fixed repayment schedule. The primary goals are simplicity and reducing the total interest paid.

However, consolidation is a tool, not a cure. If you do not address the spending habits that created the debt, consolidation can lead you right back into a deeper financial hole. This guide will help you determine if consolidating your debt is the right move for your financial situation.

What Does Debt Consolidation Mean?

In simple terms, consolidation means moving debt. You are exchanging multiple payments, due dates, and interest rates for a single payment.

Think of it like this: If you have five separate debts, you are making five trips to the bank every month. With consolidation, you get a new, large loan and use that money to pay off the five debts instantly. Now, you only owe money to the provider of the new consolidation loan.

The Two Core Mechanisms

- Lower Interest Rate: The most crucial benefit. If your credit card debt averages 25% APR, a consolidation loan at 10% APR saves you massive amounts of money every month.

- Fixed Payoff Date: Unlike revolving credit card debt, consolidation loans are almost always installment loans (like a car loan). You get a fixed term (e.g., 3 or 5 years), meaning you know exactly when you will be debt-free.

The Good: Why Consolidation Is Appealing (The Pros)

Consolidation offers three major advantages that make it attractive for those drowning in scattered debt.

1. Simplified Budgeting and Reduced Fees

Managing 5 to 10 different accounts is stressful. Each account has its own due date, minimum payment, and statement cycle. By combining them into one monthly payment, you dramatically reduce the chances of missing a payment (which hurts your credit score) and incurring multiple late fees.

2. Lower Monthly Payments

Consolidation often results in a lower average interest rate and, potentially, a longer repayment term. This combination can significantly reduce your minimum monthly obligation, freeing up cash flow for essentials or emergencies.

3. Escape High-Interest Debt

This is the financial powerhouse of consolidation. If you move debt from a 25% APR credit card to an 8% APR personal loan, you save 17 cents on every dollar of interest paid. This means more of your payment goes directly toward the principal balance, accelerating your payoff.

The Bad: The Hidden Dangers of Consolidation (The Cons)

Consolidation is not a magic solution. Before proceeding, you must be aware of the following risks:

1. Failure to Address Spending Habits (The Revolving Door)

The biggest risk is psychological. Once you pay off your high-interest credit cards with the consolidation loan, those cards suddenly have a $0 balance. If you haven’t fixed the underlying cause of your debt (overspending), you may be tempted to run up the balances on those cards again, leaving you with the original credit card debt plus the new consolidation loan.

2. Upfront Fees and Costs

Consolidation options often include fees that eat into your savings:

- Balance Transfer Fees: Credit cards used for balance transfers typically charge 3% to 5% of the transferred amount.

- Origination Fees: Personal loans and HELOCs (Home Equity Lines of Credit) may charge 1% to 6% of the loan principal just to set up the loan.

3. Extending the Payoff Term (Paying More Overall)

If you consolidate a 3-year debt into a 7-year loan just to lower the monthly payment, you will pay significantly more in total interest, even if the rate is lower. Always compare the total cost of interest over the entire term, not just the monthly payment.

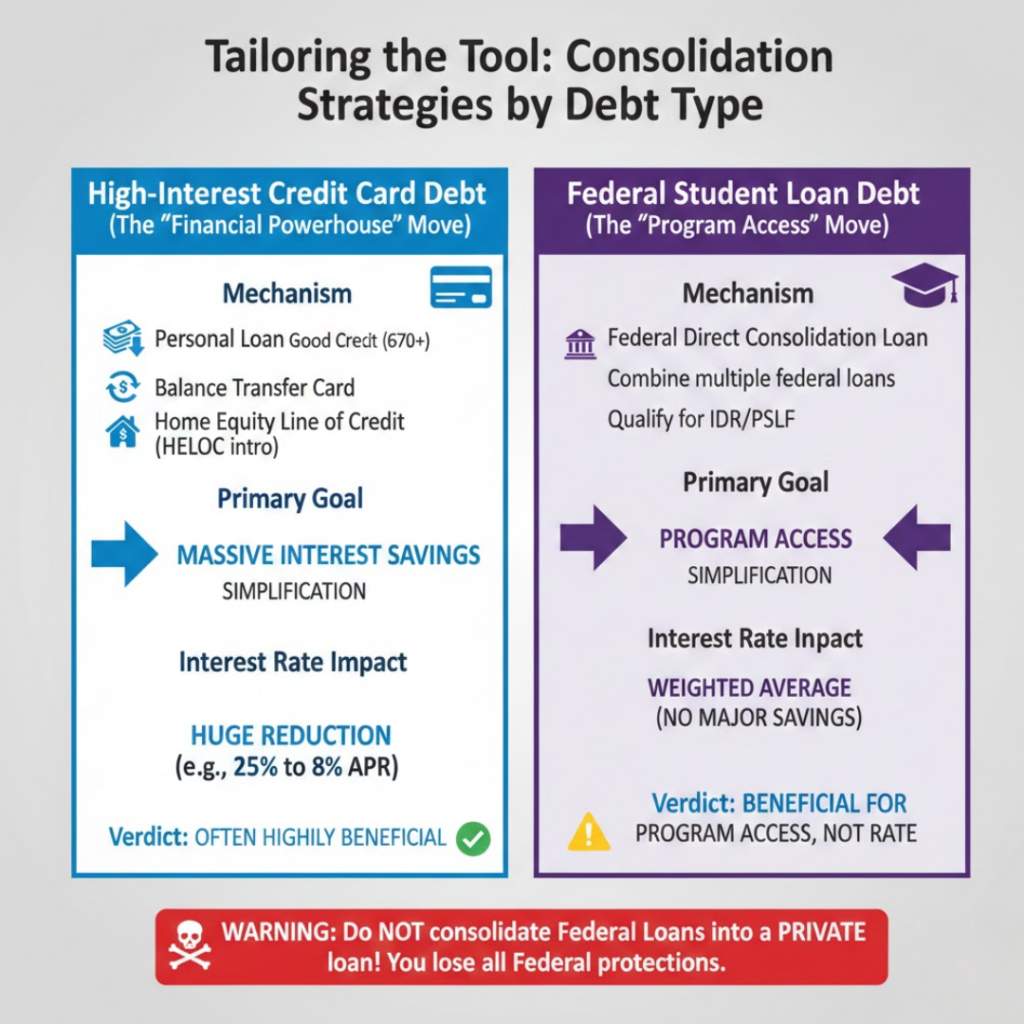

Consolidation by Debt Type: Credit Cards vs. Student Loans

The method and impact of consolidation vary dramatically depending on the type of debt you have.

A. Consolidating High-Interest Credit Card Debt

Consolidating credit card debt is usually highly beneficial due to the extremely high interest rates of revolving debt (typically 20% to 30% APR).

| Consolidation Option | Mechanism | Best For |

|---|---|---|

| Personal Loan | Single, unsecured installment loan from a bank or credit union. | Borrowers with good credit (670+) who want a fixed term and low rate (usually 7–15% APR). |

| Balance Transfer Card | Moving high-rate debt to a new credit card that offers 0% APR for an introductory period (12–21 months). | Debt that can be paid off within the introductory period. Requires a 3–5% transfer fee. |

| Home Equity Line of Credit (HELOC) | A secured loan using your home as collateral. | Homeowners with large amounts of debt. Risk: If you default, you lose your house. |

B. Consolidating Federal Student Loans

Consolidating Federal Student Loans is fundamentally different. It does not aim to lower the interest rate (it typically averages the current rates), but rather to access different repayment programs.

- Federal Direct Consolidation Loan: This combines multiple federal student loans into a single loan. Its primary purpose is to qualify the borrower for certain income-driven repayment (IDR) plans or Public Service Loan Forgiveness (PSLF).

- The Interest Rate Effect: The rate is a weighted average of your current loans, rounded up to the nearest eighth of a percent. The goal is simplification and program access, not massive interest savings.

Warning: Private Student Loan Consolidation If you consolidate federal student loans into a private student loan, you will likely get a lower interest rate, but you permanently forfeit all federal benefits, including IDR plans, forbearance options, and PSLF. This should only be done if you are absolutely certain you will never need federal protections.

The Decision Matrix: Should I Consolidate My Debt?

Before you apply, answer these questions honestly.

| Scenario | Recommendation | Rationale |

|---|---|---|

| High-Interest Debt | YES. If your average APR is over 15%, consolidation is mathematically smart. | The interest savings alone will accelerate your payoff by months or years. |

| Habit Issue | NO. If you have a history of running up card balances after paying them down. | Consolidation will give you more debt capacity, which you will likely use, resulting in double the debt. Address spending first. |

| Need for Simplicity | YES. If you are constantly missing due dates and incurring fees. | The benefit of having one bill outweighs minor fees or marginal interest savings. |

| Federal Student Loans | YES (Carefully). Consolidate federally to qualify for IDR or PSLF. | Do not consolidate federal loans into a private loan unless you are absolutely sure about the repayment. |

| Good Credit Score | YES. If your score is 670 or higher. | You will qualify for the best personal loan rates (often single-digit APRs), maximizing your savings. |

| Poor Credit Score | NO (Wait). If your score is below 600. | You will likely be offered a high-interest consolidation loan (e.g., 25%+ APR), making the move pointless or even detrimental. |

Frequently Asked Questions (FAQ)

1. Does consolidating debt hurt my credit score?

Initially, yes, slightly. When you apply for a new loan, the lender performs a hard inquiry, which temporarily drops your score by a few points. However, the overall effect is usually positive in the long run because:

- You replace revolving credit utilization with an installment loan (a better “credit mix“).

- Your overall credit utilization (amounts owed) drops as you pay off the principal.

2. Can I consolidate secured debt (like a car loan)?

You can, but it is rarely recommended. Secured debts (auto loans, mortgages) already have low interest rates because they are backed by collateral. Consolidating them into a higher-rate personal loan to save on interest is almost impossible and carries no benefit.

3. What is the best type of consolidation loan?

The best option for consumer debt is usually a personal loan from a credit union or an online lender. These loans are unsecured, have fixed interest rates, and provide a clear, fixed end date for your debt.

4. How long does debt consolidation take to pay off?

Most personal consolidation loans offer terms ranging from 3 to 7 years. The total time depends on your loan amount and the term you choose. By contrast, credit card debt, when only paying the minimum, can take 20 to 30 years to pay off.