How to Maximize Credit Score Benefits with Rent Reporting: The Effortless way to Building Credit

Your credit score is one of the most powerful financial tools you have—it shapes your ability to qualify for loans, secure credit cards, rent an apartment, and even land certain jobs. But here’s the truth: millions of Americans have lower scores or thin credit files not because they’re financially careless, but because the traditional credit system ignores a key part of their financial responsibility—on-time rent payments. That’s where smart strategies to maximize credit score benefits come in. By leveraging rent reporting, you can turn your consistent monthly payments into a proven tool for building stronger credit, faster—without changing your spending habits or taking on new debt.

One of the most overlooked yet impactful ways to build or improve your credit score? Rent reporting.

Unlike credit cards or loans, rent payments have historically been invisible to credit bureaus — even though most people pay their rent on time, every month. But that’s changing. With rent reporting services, you can now turn your consistent rent payments into a legitimate credit-building tool. In this guide, we’ll show you exactly how to maximize credit score benefits from rent reporting — and do it the right way.

Why Rent Reporting Matters for Your Credit Score

Before diving into strategies, it’s important to understand why rent reporting is such a game-changer.

The average American spends about 30% of their income on rent. For many, rent is their largest monthly financial obligation — and often, the one payment they never miss. Yet, until recently, that financial responsibility didn’t count toward building credit.

Now, thanks to advancements in credit reporting technology and growing consumer demand, rent reporting is becoming mainstream. Services like Axcessrent, Experian Boost, RentTrack, PayYourRent, and LevelCredit allow tenants to report their rental payments to one or more of the three major credit bureaus: Experian, Equifax, and TransUnion.

But here’s the key: Not all rent reporting services are created equal. Some report to only one bureau, others to all three. Some use newer credit scoring models (like FICO Score 9 or 10), while others may not impact older models at all.

So if you’re serious about improving your credit, you need a strategic approach — not just a one-time sign-up.

The Power of On-Time Payments: The Foundation of Credit Health

Let’s start with the basics: on-time payments are the single most important factor in your credit score.

According to FICO, payment history accounts for 35% of your FICO Score — making it the biggest contributor to your overall creditworthiness. This includes credit cards, loans, and now, rent.

When you consistently pay your rent on time, and that payment is reported to the credit bureaus, you’re adding a long-term, positive payment history to your credit file. Over time, this can:

- Increase your credit score

- Strengthen your credit mix

- Demonstrate financial reliability to lenders

Real-World Impact: A 2020 study by Experian found that consumers who added on-time rent payments to their credit reports saw an average score increase of 24 points within just three months — with some seeing gains of over 50 points.

But here’s the catch: only consistent, on-time payments deliver results. Missed or late payments can do more harm than good.

How to Choose the Right Rent Reporting Service

Not all rent reporting platforms are equally effective. To maximize credit score benefits, you need to pick a service that:

- Reports to all three credit bureaus – The more bureaus that see your payment history, the greater the impact on your overall credit profile.

- Uses FICO- and VantageScore-friendly models – Make sure the service is compatible with widely used scoring systems.

- Offers historical reporting – Some services allow you to report up to 24 months of past on-time payments, giving your score an instant boost.

- Is landlord-approved or tenant-initiated – Some services require landlord cooperation, while others let tenants self-report.

Combine Rent Reporting with Other Alternative Data

Here’s where most people stop — but the smartest credit builders go further.

Rent is just one part of your monthly financial picture. To truly maximize your credit score, combine rent reporting with other forms of alternative data, such as:

- Utility bills (electricity, water, gas)

- Phone and internet payments

- Streaming subscriptions (if reported through certain services)

Yes — you read that right. You can now report your Netflix or phone bill to boost your credit.

Why this works: Alternative data helps build a more complete picture of your financial responsibility. For people with limited credit history (like young adults or immigrants), this can be a lifeline.

FICO Score 9 and 10 now factor in certain types of alternative data, and VantageScore 4.0 has included it for years. The more positive data you add, the stronger your credit profile becomes.

Example: Jane, a 25-year-old renter with no credit cards, started using Axcessrent to report her rent, phone bill, and electricity payments. Within six months, her credit score jumped from 580 to 670 — enough to qualify for a low-interest auto loan.

Action Steps:

- Use a service that reports multiple types of payments (e.g., Experian Boost or LevelCredit).

- Focus on consistent, on-time payments across all bills.

- Avoid services that charge high fees or only report to one bureau.

Avoid Missed or Partial Payments — And Know How They’re Reported

This is critical: a single missed or late rent payment can undo months of progress.

While most rent reporting services only report on-time payments, some may report late payments — especially if they’re 30+ days past due. And once a late payment hits your credit report, it can stay there for up to seven years.

Even worse: partial payments can be flagged as delinquent. If you pay $500 of a $1,500 rent bill, some services may report the account as “not paid in full,” which can hurt your score.

How to protect yourself:

- Set up automatic payments – Link your bank account to your rent reporting service to ensure you never miss a due date.

- Communicate with your landlord – If you’re facing financial hardship, talk to your landlord before the due date. Some may allow payment plans without reporting delays.

- Verify reporting policies – Ask your service: Do you report late payments? After how many days? Can I dispute an error?

- Avoid partial payments – Pay the full amount, even if it means adjusting your budget.

Red Flag: Some third-party payment platforms (like certain rent apps) may not report payments accurately or may delay reporting, creating confusion on your credit report.

Always double-check that your payments are being reported correctly — and dispute any errors immediately.

Monitor Changes in Your Credit Score Regularly

You wouldn’t drive a car without checking the gas gauge. So why manage your credit without monitoring your score?

After enrolling in rent reporting, track your credit score monthly to see how your efforts are paying off.

Why monitoring matters:

- It shows you the real impact of rent reporting

- Helps you catch errors or fraud early

- Lets you adjust your strategy if results are slow

Best Tools for Monitoring:

- Credit Karma – Free VantageScore from TransUnion and Equifax

- Experian Free Credit Monitoring – Free FICO Score 8 from Experian

- myFICO – Paid access to all three bureau scores and FICO versions

- Credit Sesame – Free score tracking and alerts

What to Look For:

- Is your score increasing month-over-month?

- Are your rent payments appearing on your credit report?

- Are there any unexpected negative marks?

Case Study: Mark started reporting rent payments through in January. By March, he noticed a 15-point increase in his Experian score. But his Equifax and TransUnion scores hadn’t changed. He contacted another and learned his landlord only authorized reporting to Experian. He switched to another, which reports to all three bureaus, and saw his other scores rise within 60 days.

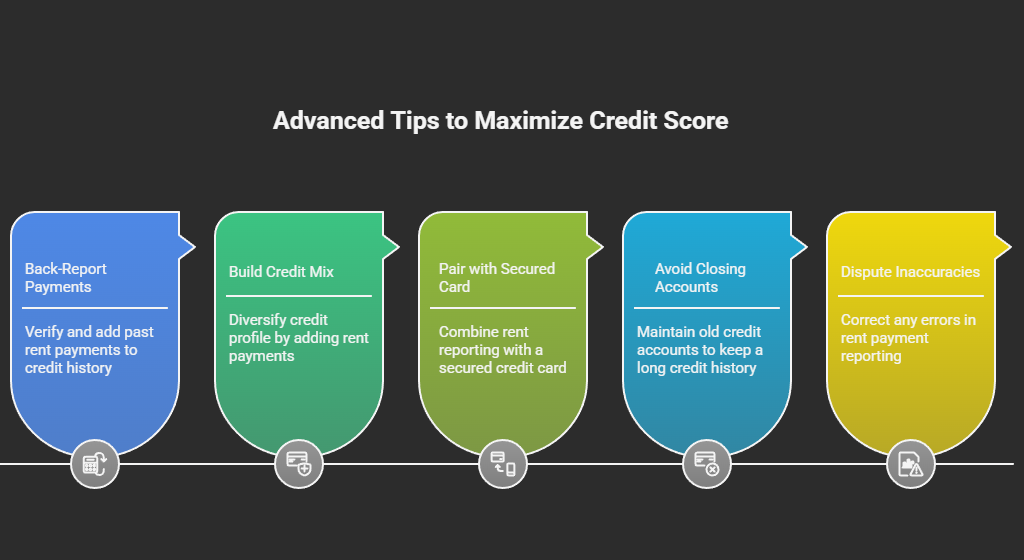

Advanced Tips to Maximize Credit Score benefits

Now that you know the basics, let’s go deeper. Here are pro-level strategies to get the most out of rent reporting:

1. Back-Report Up to 24 Months of On-Time Payments

Many services let you verify past rent payments (with bank statements or landlord confirmation) and add them to your credit history. This can instantly boost your score by showing a longer track record of responsibility.

Tip: Gather 12–24 months of bank statements showing rent transfers before signing up.

2. Use Rent Reporting to Build Credit Mix

Credit mix — the variety of credit types you use — accounts for 10% of your FICO Score. By adding rent (a non-traditional installment-like payment), you diversify your profile, which can improve your score over time.

3. Pair Rent Reporting with a Secured Credit Card

If you’re new to credit, combine rent reporting with a secured credit card. Use it for small purchases and pay it off in full each month. This builds both payment history and credit utilization — two major scoring factors.

4. Avoid Closing Old Accounts

While rent reporting helps, don’t neglect your existing credit. Keep old credit card accounts open (even if unused) to maintain a long average account age — another key scoring factor.

5. Dispute Inaccurate Reporting Immediately

If a rent payment is marked late when you paid on time, file a dispute with the credit bureau and the reporting service. Provide proof (bank statements, receipts) to get it corrected.

Common Myths About Rent Reporting — Debunked

Let’s clear up some confusion:

❌ Myth: Rent reporting is only for people with bad credit.

✅ Truth: It helps everyone — from credit newcomers to those with excellent scores who want to strengthen their profile.

❌ Myth: All rent payments automatically get reported.

✅ Truth: Unless you or your landlord use a reporting service, rent payments are not included in your credit report.

❌ Myth: Rent reporting can hurt your score.

✅ Truth: Only if late payments are reported. Most services only report on-time payments — so if you pay on time, you’re safe.

❌ Myth: It’s too expensive.

✅ Truth: Cost less than $1.95/month with Axcessrent— less than a single streaming subscription. The long-term credit benefits far outweigh the cost.

Final Thoughts: Rent Reporting Is a Smart, Sustainable Way to Build Credit

For decades, the credit system ignored one of the most consistent financial behaviors: paying rent. That’s changing — and you can be one of the first to take full advantage.

By reporting your on-time rent payments, combining them with other alternative data, avoiding late payments, and monitoring your progress, you’re not just boosting a number — you’re building real financial power.

Your rent is already part of your budget. Now, make it part of your credit story.