Length of Credit History: What Is a “Good” Credit Age?

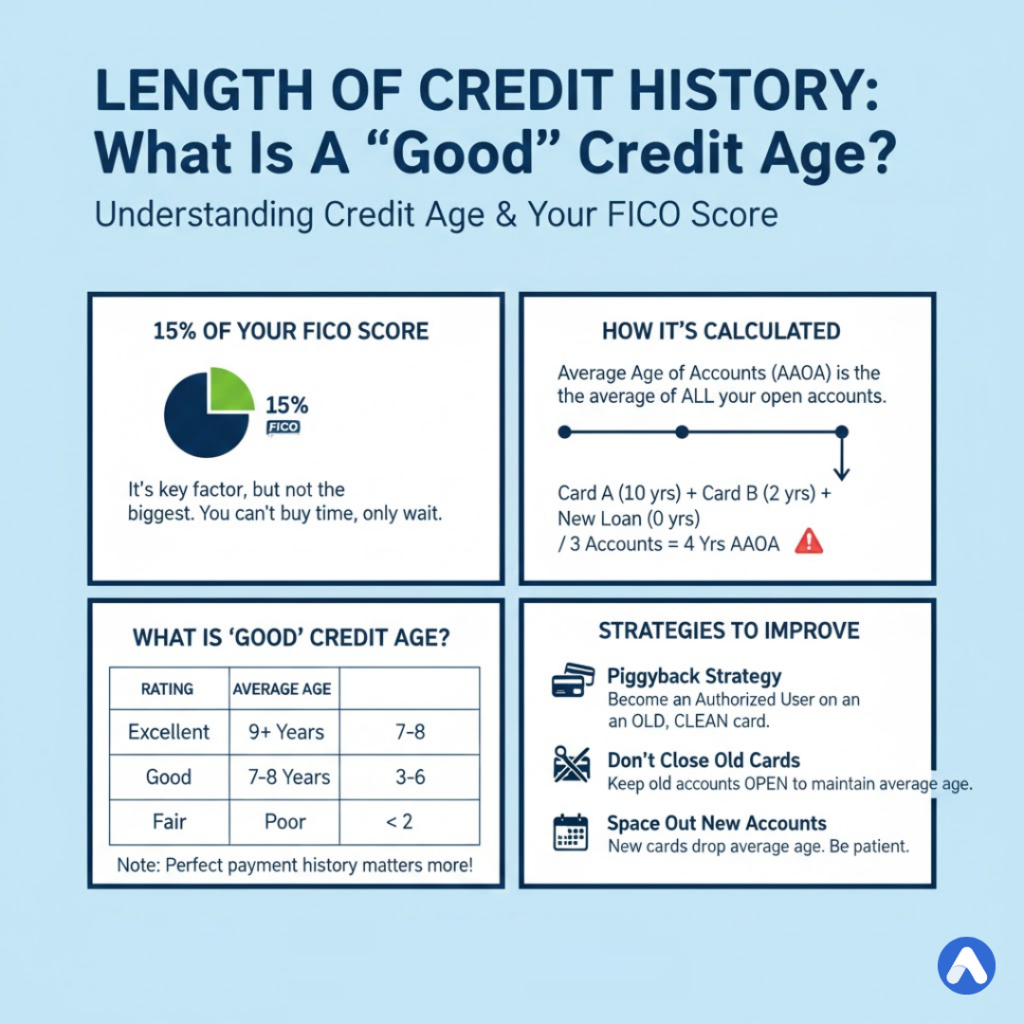

When you check your credit score, you might see a grade for “Length of Credit History” (also called Credit Age). While it isn’t the biggest factor in your score—it accounts for 15% of your FICO score—it is often the hardest to improve because you cannot “buy” time. You simply have to wait for it.

However, understanding how this factor is calculated can save you from making common mistakes, such as closing old credit cards, which can accidentally shorten your history and drop your score.

What Is Length of Credit History?

Length of Credit History measures how much experience you have managing credit over time. Lenders view a long history as a sign of stability. A borrower who has paid bills on time for 20 years is statistically less risky than someone who opened their first credit card six months ago.

It is not just about your single oldest account. FICO and VantageScore algorithms look at three distinct time measurements:

- Age of Oldest Account: The date you opened your very first loan or credit card.

- Age of Newest Account: The date of your most recent application.

- Average Age of Accounts (AAoA): The mathematical average of all your open accounts.

How Is Credit History Calculated?

The Average Age of Accounts (AAoA) is the metric that usually confuses people. It is calculated by adding up the age of every account on your credit report and dividing by the total number of accounts.

Example Calculation:

- Card A: 10 years old

- Card B: 2 years old

- Auto Loan: 0 years (Just opened)

Calculation: (10 + 2 + 0) ÷ 3 accounts = 4 Years Average Age

This is why opening a new credit card can hurt your score. You are adding a “0-year” account to the pile, which drags down your average immediately.

Credit History Ranges: What is “Good”?

While FICO does not publish a strict “pass/fail” chart, industry data gives us clear benchmarks for what lenders consider a “good” length of credit history.

| Rating | Average Age of Accounts |

|---|---|

| Excellent | 9+ Years |

| Good | 7 – 8 Years |

| Fair | 3 – 6 Years |

| Poor | Less than 2 Years |

Note: You can still have an 800 credit score with a “Fair” credit age (e.g., 4 years) if your payment history and utilization are perfect. Length of history is a supporting factor, not the main driver.

How to Improve and Increase Credit History

Since you cannot fast-forward time, improving this factor requires strategy and patience.

1. The “Piggybacking” Strategy (Fastest Method)

This is the only shortcut. If you have a parent or spouse with a credit card that is 10+ years old and has a perfect payment record, ask them to add you as an Authorized User.

- How it works: The entire history of that 10-year-old card gets “copied” to your credit report. Suddenly, the algorithm thinks you have been managing that account for a decade, instantly boosting your average age.

2. Do Not Close Old Credit Cards

If you have an old credit card you rarely use (like a starter card with a small limit), do not close it.

- Why: That card is anchoring your history. If you close a 10-year-old card, you lose that “age” from your average calculation (eventually), and your score will drop.

- The Fix: Put a small recurring charge on it (like a $5 streaming subscription) and set it to auto-pay just to keep the account active.

3. Space Out New Applications

Every time you open a new account, your average age drops. Avoid “churning” (opening many cards at once) if you are planning to apply for a mortgage soon. Lenders prefer to see a stable history, not a frantic opening of new accounts.

Frequently Asked Questions (FAQ)

Does closing a credit card hurt my history immediately?

For FICO scores, no. Closed accounts with positive history stay on your report for 10 years and continue to count toward your average age. However, for VantageScore (used by Credit Karma and others), closed accounts may stop counting toward your age much sooner, potentially showing a drop immediately.

What is the minimum history needed for a credit score?

To generate a FICO score, you must have at least one account that has been open for six months or more, and at least one account that has been reported to the credit bureau within the last six months.

Can I have an 800 score with a short history?

It is difficult but possible. If you have a “thin file” (short history), you need near-perfection in every other category: 0% late payments, very low utilization (under 5%), and a good mix of credit types. However, a “thick file” (long history) is much more resilient to small mistakes.

Why did my credit age drop when I paid off my car?

When you pay off an installment loan (like a car or student loan), that account is closed. While it stays on your report for 10 years, some scoring models (especially VantageScore) may weigh active, open accounts more heavily than closed ones, leading to a slight dip in points.