How to Get Approved for a Loan ?Guide to Home, Car, and Personal loan

Securing financing—whether it’s for a new home, a vehicle upgrade, or consolidating high-interest debt—can feel like navigating a complex maze. But the loan approval process, while specific to the type of loan you seek, relies on a universal set of financial principles.

Lenders evaluate risk, and your preparation determines whether you are deemed a safe investment. By focusing on your credit health, stability, and documentation, you can confidently answer the question: How to get approved for a loan?

This guide breaks down the essential pre-approval steps, the core factors lenders evaluate, and the specific requirements for car, home, and personal loans.

Phase 1: The Foundation of Loan Approval

Before you ever speak to a lender, you must understand the two most critical factors that determine your eligibility for any type of loan.

1. Master Your Credit Profile

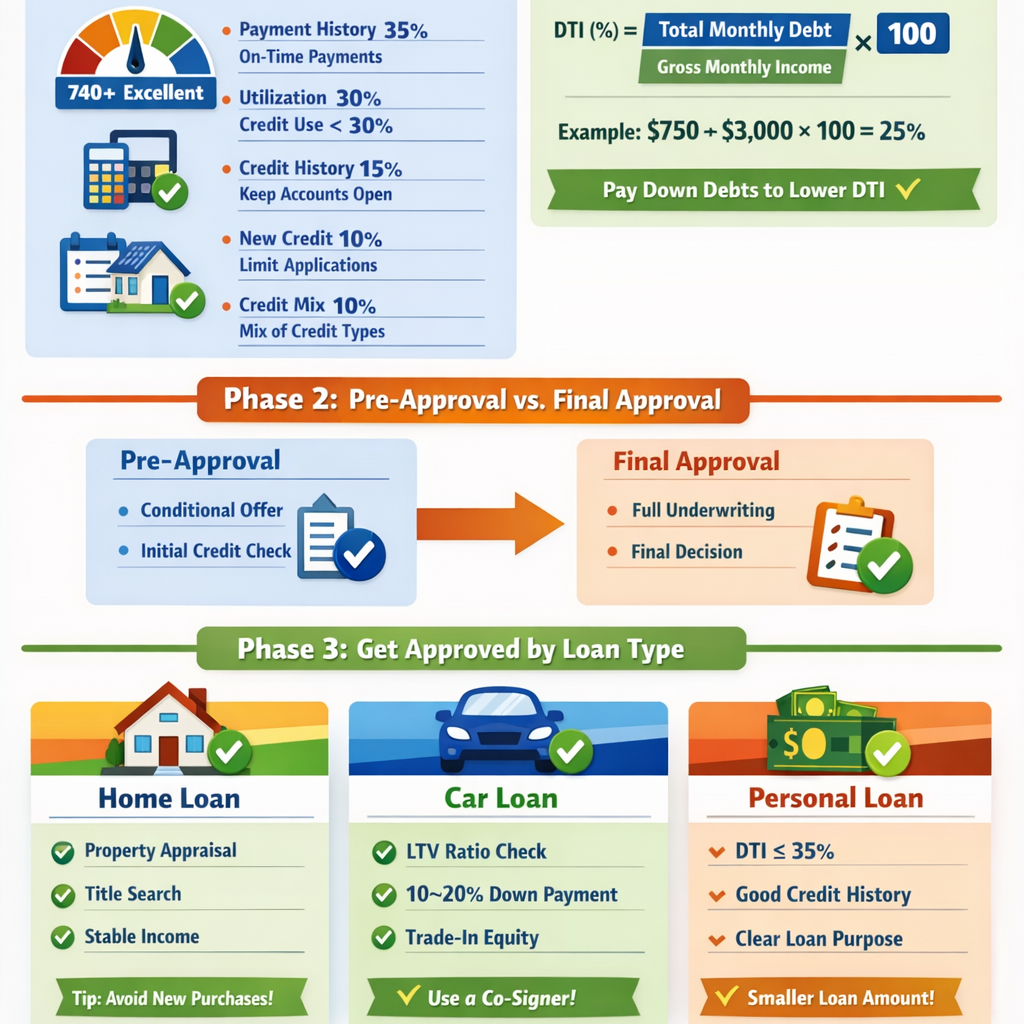

Your credit score (typically FICO or VantageScore) is a numerical summary of your financial character. A high score grants access to better interest rates, which directly translates into thousands of dollars in savings over the life of a loan.

| FICO Factor | Weight | Action for Approval |

|---|---|---|

| Payment History | 35% | Never miss a payment. This is the single most important factor. Set up auto-pay if necessary. |

| Amounts Owed (Utilization) | 30% | Keep your revolving credit utilization below 30 % (ideally below 10%. Maxing out cards is a major red flag. |

| Length of Credit History | 15% | Do not close old, healthy accounts, even if you don’t use them. Age adds stability to your profile. |

| New Credit | 10% | Avoid applying for multiple lines of credit simultaneously (especially 30–90 days before a major loan application). |

| Credit Mix | 10% | Demonstrate you can manage different types of credit (revolving like credit cards, and installment like a student loan). |

Approval Thresholds:

- Excellent: 740+ (Best rates for mortgages and cars)

- Good: 700–739 (Generally strong approval odds)

- Fair: 620–699 (May qualify, but rates will be higher)

2. Optimize Your Debt-to-Income Ratio (DTI)

The Debt-to-Income (DTI) ratio is perhaps the most important metric for large loans, especially mortgages. It measures the percentage of your gross monthly income that goes toward paying your recurring monthly debt obligations.

DTI Formula

DTI (%) = (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100

Example: If your monthly debts are $750 and gross income is $3,000:

DTI = (750 ÷ 3000) × 100 = 25%

Where:

- Total Monthly Debt Payments = all recurring debt obligations (credit cards, auto loans, student loans, mortgages, personal loans, etc.)

- Gross Monthly Income = total income before taxes (salary, bonuses, rental income, etc.)

Action: Before applying, pay down credit card balances or personal loans to reduce your total monthly debt load, thereby lowering your DTI.

Phase 2: Understanding Pre-Approval vs. Final Approval

Many applicants confuse pre-approval with final approval. Understanding the difference is key to a smooth process.

What is Pre-Approval?

Pre-approval is a conditional commitment from a lender, providing a preliminary confirmation of the loan amount you are likely to qualify for, based on a review of your finances.

- Purpose: It gives you a clear budget, locks in a potential interest rate (for home loans), and shows sellers/dealers that you are a serious and viable buyer.

- Process: Requires a formal application and documentation (pay stubs, tax returns, credit check).

How to Get Pre Approved for a Home Loan

Pre-approval is mandatory in competitive real estate markets. It shows you are serious and can close quickly.

- Select a Lender: Start with a mortgage broker, credit union, or national bank.

- Gather Documentation:

- Last two years of W-2s and tax returns.

- Last two months of bank statements (checking/savings).

- Recent pay stubs covering 30–60 days.

- Statements for retirement/investment accounts.

- Submit Application & Consent to Credit Check: The lender runs a hard inquiry to pull your full credit profile and determines your maximum qualified loan amount and estimated rate.

- Receive Pre-Approval Letter: This document states the maximum amount the lender is willing to lend you, contingent upon the property (appraisal) and final underwriting.

How to Get Pre Approved for a Car Loan

Car loan pre-approval is less rigorous than a mortgage and is vital for negotiating the vehicle price, as it separates the financing decision from the vehicle purchase.

- Choose a Lender: Approach your credit union or a bank before setting foot on a dealership lot.

- Simple Application: You typically provide income verification, employment history, and authorize a credit pull (often a hard inquiry).

- Get a Loan Offer: The lender provides a commitment letter with an interest rate and maximum loan amount.

- Use the Offer as Leverage: This external financing rate forces the dealership to beat or match it, ensuring you don’t overpay for the financing they offer.

Phase 3: Getting Approved for Specific Loan Types

While the foundation is the same, the path to final approval differs significantly depending on whether the loan is secured (home, car) or unsecured (personal).

1. How to Get Approved for a Home Loan (Mortgage)

Difficulty: Hard (Due to the complexity and reliance on property value.)

The final approval stage (underwriting) happens after you have an accepted offer on a property. Underwriting is a deep dive into your finances and the property itself.

Key Underwriting Hurdles:

- Appraisal: The property must be appraised by a neutral third party, and the value must meet or exceed the purchase price. If it appraises lower, the lender will only finance up to the appraised value.

- Title Search: A title company must verify that the seller legally owns the property and that there are no outstanding liens or claims against it.

- Income Stability: Underwriters verify your employment history (typically two years) to ensure income consistency. Large, unexplained gaps in employment are red flags.

- Reserves: Lenders check that you have sufficient reserves (savings) left over after closing to cover mortgage payments for several months.

Tip: Do not make any major purchases, apply for new credit, change jobs, or deposit large, unexplained sums of cash into your bank account between pre-approval and closing. Any change can jeopardize your final approval.

2. How to Get Approved for a Car Loan

Difficulty: Medium (Simpler underwriting, but still requires good credit/income.)

Car loans are secured loans, meaning the vehicle serves as collateral. The approval process is faster because the underwriting risk is partially mitigated by the asset’s value.

Key Factors for Car Loan Approval:

- LTV Ratio (Loan-to-Value): Lenders check the vehicle’s value against established indices (like Kelley Blue Book or Black Book). They want to ensure the loan amount is not significantly higher than the car’s worth.

- Down Payment: A larger down payment (e.g., 10%–20%) lowers your Loan-to-Value (LTV) ratio, reducing lender risk and improving your approval chances and interest rate.

- Trade-in Equity: If you are trading in an old vehicle that is worth more than you owe on it (positive equity), this cash equity acts like an immediate down payment.

Tip: If your credit is poor, applying with a qualified co-signer (who has better credit and a low DTI) can significantly improve your chances of approval and lower your interest rate.

3. How to Get Approved for a Personal Loan

Difficulty: Hard (Unsecured, meaning no collateral to back the debt.)

Personal loans are typically unsecured, used for purposes like debt consolidation, weddings, or home improvements. Because the lender has no collateral to seize if you default, they rely entirely on your credit history and income stability.

Key Factors for Personal Loan Approval:

- Income Stability & DTI: Lenders review your income and DTI ratio; for unsecured loans, a DTI ≤ 35% and stable, predictable income are crucial for approval.

- Credit History: Lenders prefer borrowers with a long history of managing revolving debt responsibly. They want assurance that you won’t use the personal loan to immediately max out credit cards.

- Loan Purpose: While not always required, sometimes stating a clear purpose (like “debt consolidation”) helps the lender understand that the funds are being used to reduce overall financial risk, rather than increase spending.

- Lower Loan Amounts: If you struggle with approval, try applying for a smaller amount. The lower the loan principal, the lower the risk to the lender.

The Ultimate Approval Checklist

Whether you are seeking a pre-approval for a new car or the final underwriting for a mortgage, preparing these three areas will significantly increase your likelihood of success:

| Financial Pillar | Checklist Item | Why it Matters |

|---|---|---|

| Credit | Pay down credit card balances to keep utilization below 30%—ideally around 10%—to boost your credit score. | Immediately boosts your score (affects 30% weight). |

| Debt & Income | Calculate your current Back-End DTI. | Lenders universally use DTI to cap your maximum borrowing limit. |

| Documentation | Gather 2 years of W-2s/tax returns and 60 days of bank statements. | This proves your income and ability to afford the down payment/closing costs. |

| Risk Reduction | Down Payment Savings: Aim for a minimum 3% for a home or 10% for a car to improve approval odds and lower lender risk. | Lowers the lender’s Loan-to-Value (LTV) risk. |

The core secret to loan approval is preparation. Start four to six months before you intend to apply. Use this time to clean up credit report errors, reduce high-interest debt, and stabilize your income. By demonstrating responsibility and minimizing risk, you position yourself as a prime candidate for the most competitive loan rates available.

FAQs

1. What is the most critical factor a lender looks at, and what is the maximum acceptable limit?

The most critical factor, especially for mortgages, is the Debt-to-Income (DTI) Ratio. This ratio measures your total monthly debt payments against your gross monthly income.

The ideal back-end DTI is ≤36%, but lenders typically allow ≤43% for mortgages and 40–50% for personal loans.

2. What is the difference between pre-approval and final approval?

Pre-approval is a conditional commitment based on a preliminary review of your credit and income documentation. It gives you a maximum budget and potential rate.

Final approval occurs during the underwriting stage. It is a deep dive that verifies all documents, and critically, requires the collateral (home or car) to meet the lender’s criteria (e.g., successful home appraisal or car valuation).

3. How does a “hard inquiry” affect my credit when seeking pre-approval?

A hard inquiry occurs when you formally apply for a loan (like for a mortgage pre-approval or car loan). It allows the lender to pull your full credit report. Hard inquiries can cause a small, temporary dip in your credit score, typically less than 5 points, and they remain on your report for up to two years.

4. Why is a down payment so important for a car loan?

A 10–20% down payment lowers the Loan-to-Value (LTV) ratio, reducing lender risk and improving approval odds and interest rates. TV is the ratio of the loan amount to the car’s market value. A lower LTV reduces the lender’s risk, which, in turn, improves your approval odds and secures a better interest rate.

5. Why are personal loans considered “Hard” to get, even for applicants with good credit?

Personal loans are typically unsecured, meaning there is no collateral (like a house or car) for the bank to seize if you default. Because the lender relies entirely on your promise to pay, they scrutinize your income stability and DTI ratio much more closely than they would for a secured loan.

6. What major financial actions should I avoid after receiving pre-approval for a home loan?

Once you are pre-approved, you must maintain financial stability until closing. You should not do the following:

- Make any large purchases (e.g., furniture, appliances).

- Apply for new credit (e.g., opening a new credit card or taking out a new car loan).

- Change jobs or quit your current job.

- Deposit large, unexplained sums of cash into your bank account.

7. What credit score range is considered the “Excellent” standard for securing the best interest rates?

A credit score of 740+ is typically considered Excellent. This range places you in the best tier for securing the lowest available interest rates for major financing like mortgages and car loans. Scores in the 700–739 range are considered “Good” and generally secure strong approval odds, though the rate may be slightly higher.