How Lenders Evaluate Risk: Credit Utilization, Refinancing, and Secured Loans Explained

Introduction: Why Risk Matters to Lenders

In the financial world, risk is everything. Every loan or credit card approval is essentially a calculated bet on a borrower’s future behavior. Lenders make money only when borrowers repay both the principal and interest as agreed. When a borrower defaults, the lender doesn’t just lose profits—it can lose the capital itself.

Your credit behavior—how much debt you carry, how responsibly you manage it, and whether your loans are secured—acts as a financial blueprint. This blueprint helps lenders predict how likely you are to repay what you borrow.

This guide explains:

- What a lender is

- Which credit utilization rate lenders prefer

- Why secured loans are less risky

- Whether you can refinance a car loan with the same lender

- How lenders combine these factors into a risk profile

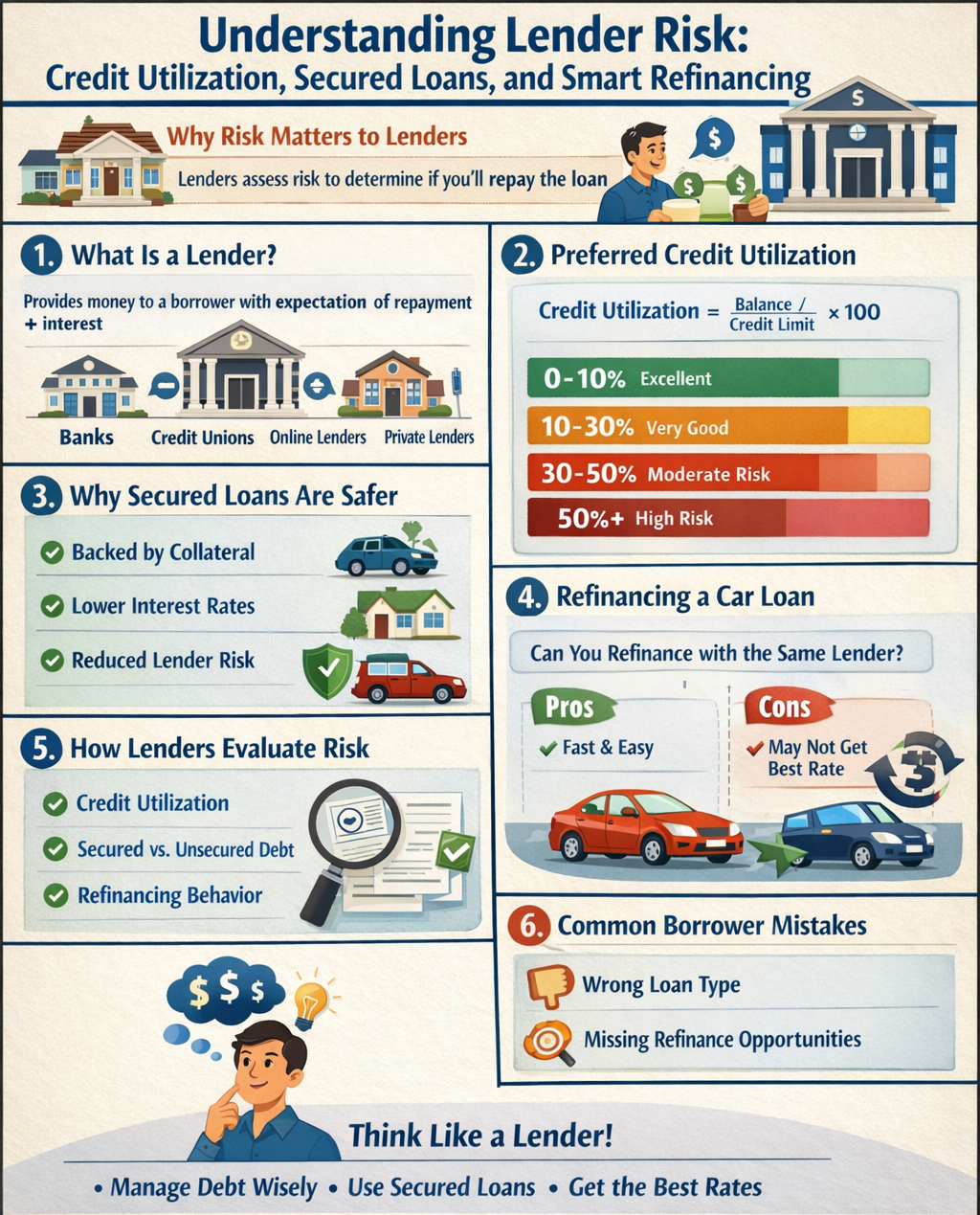

1. What Is a Lender?

Definition of a Lender

A lender is an individual or financial institution that provides money to a borrower with the expectation of repayment, plus interest. Interest is the cost of borrowing money and compensates the lender for taking risk.

Types of Lenders

Different lenders serve different borrower profiles:

- Retail Banks – Traditional banks that use customer deposits to fund loans. They usually offer lower rates but stricter approval standards.

- Credit Unions – Member-owned, non-profit institutions that often provide lower interest rates and flexible underwriting.

- Online Lenders (FinTech) – Algorithm-driven lenders offering fast approvals, often targeting borrowers with limited credit history.

- Dealership Lenders – Manufacturer-backed finance companies created to support vehicle sales.

- Private Lenders – Individuals or firms offering capital, often at higher rates and for specialized situations.

How Lenders Make Money

Lenders earn revenue through:

- Interest charges

- Fees, such as origination fees, late fees, and processing costs

Difference Between Lender and Creditor

While often used interchangeably, there is a subtle distinction. A lender usually refers to an entity providing a specific loan (like a mortgage or auto loan). A creditor is a broader term encompassing any entity to which money is owed, including credit card issuers or service providers (like utility companies) that provide services before payment is received.

2. Which Credit Utilization Rate Do Lenders Prefer?

What Is Credit Utilization?

Credit utilization is a ratio that compares the amount of revolving credit you are currently using to the total amount of revolving credit available to you. It is expressed as a percentage.

Credit Utilization Formula

Credit Utilization Rate = (Total Outstanding Credit Card Balances ÷ Total Available Credit Limits) × 100

Example:

A $1,000 balance on a $5,000 limit = 20% utilization

Ideal Credit Utilization Rates (From a Lender’s Perspective)

Ideal Credit Utilization Rates (Lender’s Perspective)

Lenders view utilization as a “stress test” of your monthly finances.

- 0–10% (Excellent): This range signals that you use credit as a tool, not a crutch. Lenders see you as highly liquid and low-risk.

- 10–30% (Very Good): This is the “sweet spot” preferred by most lenders. It shows active credit use (which generates some interest for them) without suggesting financial strain.

- 30–50% (Increasing Risk): Crossing the 30% threshold is often the first “yellow flag.” It suggests you may be relying on credit to cover cost-of-living increases.

- 50%+ (High-Risk Signal): High utilization suggests “maxing out.” In the eyes of a lender, a borrower with 90% utilization is one unexpected expense away from a total default.

Why Lenders Prefer Low Credit Utilization

Lenders favor low utilization because it correlates with Credit Capacity. If you lose your job, a borrower with 10%utilization has 90% of their credit lines left to survive on, making them less likely to immediately default on other obligations. Furthermore, low utilization is the most significant factor in the “Amounts Owed” category of FICO scores, which accounts for 30% of the total score.

Low utilization shows:

- Unused credit capacity, which acts as a buffer during financial stress

- Better performance in the “Amounts Owed” category, which makes up 30% of FICO scores

For maximum credit score optimization, maintaining 1–9% utilization often performs better than 0%, as it shows active and responsible credit use.

3. Why Are Secured Loans Considered Less Risky?

What Is a Secured Loan?

A secured loan is a debt instrument backed by an asset. This asset, known as collateral, serves as a secondary source of repayment for the lender.

Common examples:

- Auto loans (vehicle as collateral)

- Mortgages (home as collateral)

- Secured credit cards (cash deposit as collateral)

Reasons Secured Loans Are Less Risky

- Collateral Reduces Loss (LGD): In finance, lenders calculate “Loss Given Default” (LGD). If a borrower stops paying a $20,000 unsecured personal loan, the LGD is nearly 100%. If they stop paying a $20,000 auto loan, the lender repossesses the car and sells it for $15,000, reducing the LGD to only $$5,000 plus costs.

- The “Incentive to Pay”: Borrowers are psychologically and practically more motivated to pay secured loans. Losing a home or the car needed to get to work has immediate, devastating consequences, whereas an unpaid credit card just results in phone calls and credit score damage.

- Predictable Loan Structures: Secured loans are almost always “closed-end” credits with fixed terms and clear amortization schedules, making them easier for lenders to manage on their balance sheets compared to unpredictable revolving lines of credit.

Benefits for Borrowers

Because the risk to the lender is lower, the benefit is passed to the borrower in the form of:

- Lower Interest Rates: The “Risk Premium” added to the base rate is significantly smaller.

- Easier Approval: Borrowers with lower credit scores can often get a car loan when they would be denied a credit card.

- Higher Limits: Lenders are willing to lend hundreds of thousands of dollars for a home (secured) but rarely more than $20,000–$50,000 on a credit card (unsecured).

4. Can You Refinance a Car Loan With the Same Lender?

Short Answer: Yes, but it’s not guaranteed.

While you can refinance with your current lender, many large banks have policies against “internal refinancing” because it reduces their profit margin on an existing contract without adding new assets to their books.

When Same-Lender Refinancing Is Possible

- Improved credit score

- Strong banking relationship

- Loan restructuring to avoid default

When Lenders Usually Say No

If market rates drop significantly, lenders have little incentive to lower your rate unless you’re prepared to move your loan elsewhere.

When They Usually Don’t

Lenders are businesses. If you have a 7% interest rate and market rates drop to 4%, the lender has no financial incentive to give you a 3% discount out of the goodness of their heart. They would rather you keep paying the 7%. Usually, they will only match a lower rate if you prove you are ready to move the loan to another bank.

Pros & Cons of Same-Lender Refinancing

- Pros:

- Speed: They already have your VIN, personal details, and title information.

- Unified Dashboard: You don’t have to set up a new online portal or auto-pay system.

- Cons:

- Lax Competition: They may offer you a “better” rate that is still higher than what a hungry credit union across the street would offer.

- Fees: Some lenders charge “internal modification” fees that negate the savings.

Pro Tip: Always get a quote from an external credit union first. Use that quote as leverage. Tell your current lender, “I’d like to stay with you, but Bank X offered me 4%. Can you beat it?”

Get an external quote first—especially from a credit union—and use it as leverage.

5. How Lenders Evaluate Risk Holistically

Lenders combine multiple data points to build a risk profile:

- Credit utilization → Current cash flow health

- Secured vs. unsecured debt → Asset-backed safety

- Refinancing behavior → Financial awareness and borrower loyalty

Using risk-based pricing, low-risk borrowers get the lowest rates, while high-risk borrowers pay more—or are denied.

6. Common Borrower Mistakes to Avoid

Reporting Date Confusion

Credit card balances are reported on the statement closing date, not the due date.

Applying for the Wrong Loan Type

Borrowers with weaker credit often qualify more easily for secured loans than unsecured personal loans.

Ignoring Refinancing Opportunities

Even a 3% APR difference can cost thousands over the life of a loan.

7. Frequently Asked Questions (FAQ)

Is 0% credit utilization bad?

Not bad, but less effective than 1–9% for scoring purposes.

How long does it take utilization to update?

Usually 30–45 days after payment.

Does refinancing hurt credit?

Short-term dip (5–10 points), but long-term savings usually outweigh it.

Do secured loans help build credit?

Yes—especially for beginners or thin credit files.

Conclusion: Think Like a Lender to Win Better Rates

Lenders don’t look for perfect borrowers—they look for predictable, low-risk borrowers. By keeping your credit utilization below 30%, using secured loans strategically, and refinancing intelligently, you position yourself as a borrower banks want to compete for.

Understanding how lenders think transforms you from someone asking for money into a customer with leverage—and that’s where the best financial deals begin.