Mastering Loan Repayment: A Stress-Free Guide to Your Financial Freedom

Let’s face it loans are part of adulting. Whether you’re financing your education, buying wheels, or stepping into your first home, borrowing money is often necessary. That initial excitement of getting approved? It fades fast when the first payment reminder hits your inbox. Suddenly, that helpful loan becomes very real debt you need to manage.

The good news? With the right approach (and tools like a loan repayment calculator), you can tackle your debt without losing sleep. This guide will walk you through everything from understanding repayment basics to using a student loan repayment calculator to find your best payoff strategy.

Key Takeaways:

- Actionable tips to pay off debt faster

- Why loan repayment feels overwhelming (and how to simplify it)

- How a loan repayment calculator gives you control

- Special strategies for student loan repayment

What Is Loan Repayment? (And Why It Matters More Than You Think)

At its core, loan repayment means paying back the money you borrowed—but there’s more to it than just writing a check each month. It’s about staying financially healthy and in control. Here’s what it really involves:

- Repaying the principal – the original amount you took out

- Paying the interest – the fee you pay for borrowing the money

- Following a schedule – making consistent payments to avoid late fees, penalties, or credit issues

Managing loan repayment well helps you avoid stress, build credit, and protect your financial future.

What Happens If You Fall Behind?

Falling behind on your loan repayment can snowball quickly. At first, it might just mean a late fee an extra charge that eats into your budget. But if missed payments continue, it can seriously damage your credit score, making it harder (and more expensive) to get future loans, credit cards, or even rent an apartment.

In more severe cases, continued non-payment could lead to default. This is when the lender takes serious action, like sending your account to collections or even garnishing your wages. The best way to avoid this stress is to stay organized: track your due dates, understand your interest rates, and always know how much you owe. A little planning goes a long way toward protecting your finances and peace of mind.

Why Loan Repayment Feels So Overwhelming (And How to Fix It)

If you’ve ever stared at your loan statement and thought, “How am I ever going to pay this off?”—you’re not alone. Here’s why it feels so stressful:

Interest Adds Up Fast

One of the most overlooked aspects of loan repayment is how quickly interest can accumulate. For example, if you borrow $30,000 in student loans at a 6% interest rate, you could end up paying over $10,000 in interest alone over a 10-year period. That’s money that could have gone toward savings, travel, or starting a business. The takeaway? The longer you take to repay your loan, the more it will cost you in the long run. Making extra payments even small ones—can significantly reduce the total interest you’ll pay.

Life Gets in the Way

Even the most well-planned repayment strategy can get thrown off by real life. Unexpected medical bills, car repairs, or family emergencies can make it tough to stick to your monthly schedule. A sudden job change or a dip in income can turn manageable payments into a major financial burden. That’s why flexibility and planning are crucial. Creating a buffer in your budget or adjusting your repayment plan early can help you stay on track when life throws you a curveball.

Too Many Options (Especially for Student Loans)

Student loan borrowers often face a maze of confusing repayment options. From income-driven repayment plans to forgiveness programs and deferment or forbearance, it can be overwhelming to know which path is right. Each option has its own benefits, drawbacks, and eligibility requirements. Without guidance, it’s easy to pick the wrong one—or miss out on valuable benefits. Taking the time to research, or using a student loan repayment calculator, can help you make a smarter, more informed decision.

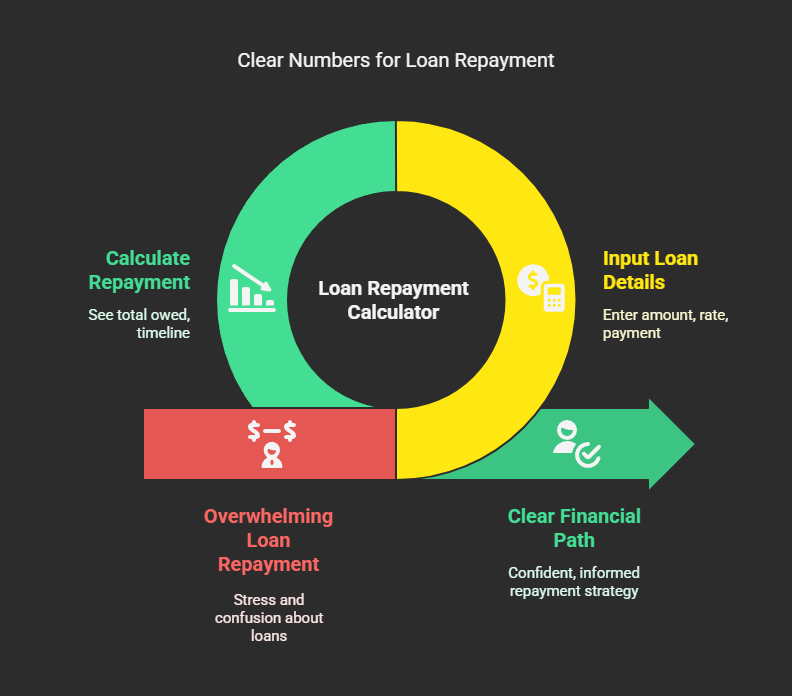

The Solution? Get Clear on Your Numbers

This is where a loan repayment calculator becomes your best friend. Instead of guessing how long it’ll take to pay off your loan—or how much interest you’re racking up you get a clear picture of your financial path. A good calculator helps you plug in your loan amount, interest rate, and monthly payment so you can see exactly what you’ll owe and when you’ll be debt-free. It’s a simple tool, but it can save you thousands and help you build a smarter repayment strategy with confidence.

How a Loan Repayment Calculator Saves Your Sanity

Imagine knowing exactly how much you’ll pay each month, how long it’ll take to be debt-free, and how much extra payments could save you. That’s what a loan repayment calculator does.

What It Tells You:

✅ Monthly payment breakdown (how much goes to principal vs. interest)

✅ Total loan cost (spoiler: It’s usually more than you borrowed)

✅ Impact of extra payments (even $50 more a month can cut years off your loan)

✅ Comparison of different terms (should you do 10 years or 20?)

Student Loan Repayment Calculator: A Must for Grads

If you’re a recent graduate, a student loan repayment calculator isn’t just helpful it’s essential. These tools allow you to compare different repayment options, including the standard 10-year plan versus income-driven repayment plans that adjust based on your earnings. They also help you explore whether loan forgiveness programs could reduce what you owe in the long run. And if you’re still within your grace period, the calculator can help you plan ahead so you’re financially ready when payments begin. It’s the smart way to take control of your student debt.

Student Loan Repayment: What Makes It Different

Student loans come with their own set of rules—very different from credit cards or personal loans. If you’re navigating repayment, here are four critical things to understand:

1. Grace Periods – Your Head Start After Graduation

Most federal student loans offer a six-month grace period after you graduate. That’s your chance to breathe before the first bill arrives. Use it wisely—secure a job, build your budget, and research the best repayment strategy for your situation. This early planning sets the tone for the years ahead.

2. Income-Driven Repayment – Pay What You Can Afford

Struggling with a low income? Plans like IBR, PAYE, and REPAYE allow you to make payments based on your earnings—usually 10–20% of your discretionary income. These plans can ease your financial stress, especially early in your career. However, they stretch your loan term to 20–25 years, and while any leftover balance may be forgiven, it might be taxable. It’s relief—but with fine print.

3. Loan Forgiveness – Relief for Public Servants and Teachers

Programs like Public Service Loan Forgiveness (PSLF) let you erase your remaining balance after 10 years of work in the nonprofit or government sector. Teachers working in qualifying schools can receive up to $17,500 in forgiveness. The catch? The paperwork must be perfect. Many are denied due to technical errors—so stay vigilant and organized.

4. Refinancing – Risk vs. Reward

Thinking of refinancing to lower your interest rate? It could save you money—but there’s a tradeoff. Refinancing federal loans turns them into private loans, meaning you lose benefits like income-driven repayment, forgiveness options, and deferment protections. Make sure the savings are worth the loss of flexibility.

5 Real-Life Tips to Make Loan Repayment Easier

1. Automate Payments (Set It and Forget It)

- Late payments hurt your credit. Auto-pay ensures you never miss one.

- Bonus: Some lenders (like federal student loan servicers) give a 0.25% interest rate discount for auto-pay.

2. Pay Extra When You Can (Even Small Amounts Help)

- Example: On a $30k student loan at 6% interest:

- Paying just $50 extra/month saves $4,400+ and cuts 3 years off repayment.

- Strategy: Use tax refunds, bonuses, or side hustle cash for extra payments.

3. Refinance (But Only If It Makes Sense)

- Good if: You have high-interest private loans and strong credit.

- Bad if: You have federal loans and need income-driven plans.

4. Use the Debt Snowball or Avalanche Method

- Snowball: Pay off smallest debts first for quick wins.

- Avalanche: Tackle highest-interest loans first to save money.

- Pick what keeps you motivated.

5. Revisit Your Plan Every Year

- Got a raise? Adjust payments.

- Struggling financially? Switch to an income-driven plan.

- A loan repayment calculator helps you adapt.

Calculate Your Loan Repayments Easily

Managing loan repayments can feel overwhelming, whether it’s a personal loan or a student loan. That’s why we created this simple, easy-to-use calculator that helps you figure out your monthly payments and compare different repayment options quickly.

Use the dropdown below to select either the general Loan Repayment Calculator or the Student Loan Repayment Calculator tailored for income-based plans. This tool empowers you to plan your finances better and avoid surprises along the way. Just enter your details, and get instant, clear results!

Loan Repayment Calculator

Final Thought: You Can Beat Your Loans

Yes, loan repayment is a marathon, not a sprint. But with the right tools (like a student loan repayment calculator) and a solid strategy, you can take control.

Your Action Plan:

- Know your loans (balances, interest rates, due dates).

- Use a loan repayment calculator to see your best payoff path.

- Pick a repayment strategy (standard, income-driven, aggressive payoff).

- Automate payments and throw extra money at debt when possible.

- Check in yearly—adjust as life changes.

Debt doesn’t have to own you. Every payment is a step toward financial freedom. Start today you’ve got this.

FAQs

1. What is loan repayment?

Loan repayment is the process of paying back the money you borrowed—plus interest—based on a set schedule. It includes monthly payments that reduce both the principal and the interest owed.

2. Why is loan repayment important?

Staying on top of your loan repayment helps you avoid late fees, protect your credit score, and prevent serious consequences like default or collections. It also ensures long-term financial health.

3. How do I know how much I owe each month?

Your loan servicer or lender will provide a repayment schedule. You can also use a loan repayment calculator to estimate your monthly payments and total cost over time.

4. What happens if I miss a loan payment?

Missed payments can result in late fees, a drop in your credit score, and eventually loan default. For student loans, missed payments could also disqualify you from forgiveness or deferment programs.

5. What is a student loan repayment calculator?

A student loan repayment calculator helps you compare different repayment plans, estimate monthly payments, and see how changes in income or interest rates affect your total repayment amount.

6. Can I pay off my loan early?

Yes! Most loans allow early repayment without penalties. Paying more than the minimum each month can reduce interest and help you become debt-free faster.

7. What’s the difference between federal and private student loans in repayment?

Federal student loans offer more flexible repayment options, including income-driven repayment and forgiveness programs. Private loans typically have stricter terms and fewer protections.

8. How do grace periods work for student loans?

Most federal student loans offer a six-month grace period after graduation before payments are due. Use this time to organize your finances and choose the right repayment plan.

9. Should I refinance my student loans?

Refinancing can lower your interest rate, but it also removes federal protections like income-based repayment and loan forgiveness. Only refinance if you’re sure you won’t need those benefits.

10. What’s the best way to keep track of loan repayment?

Use digital tools, like budgeting apps or a loan repayment calculator, to track payments, interest, and due dates. Staying organized helps prevent missed payments and financial stress.