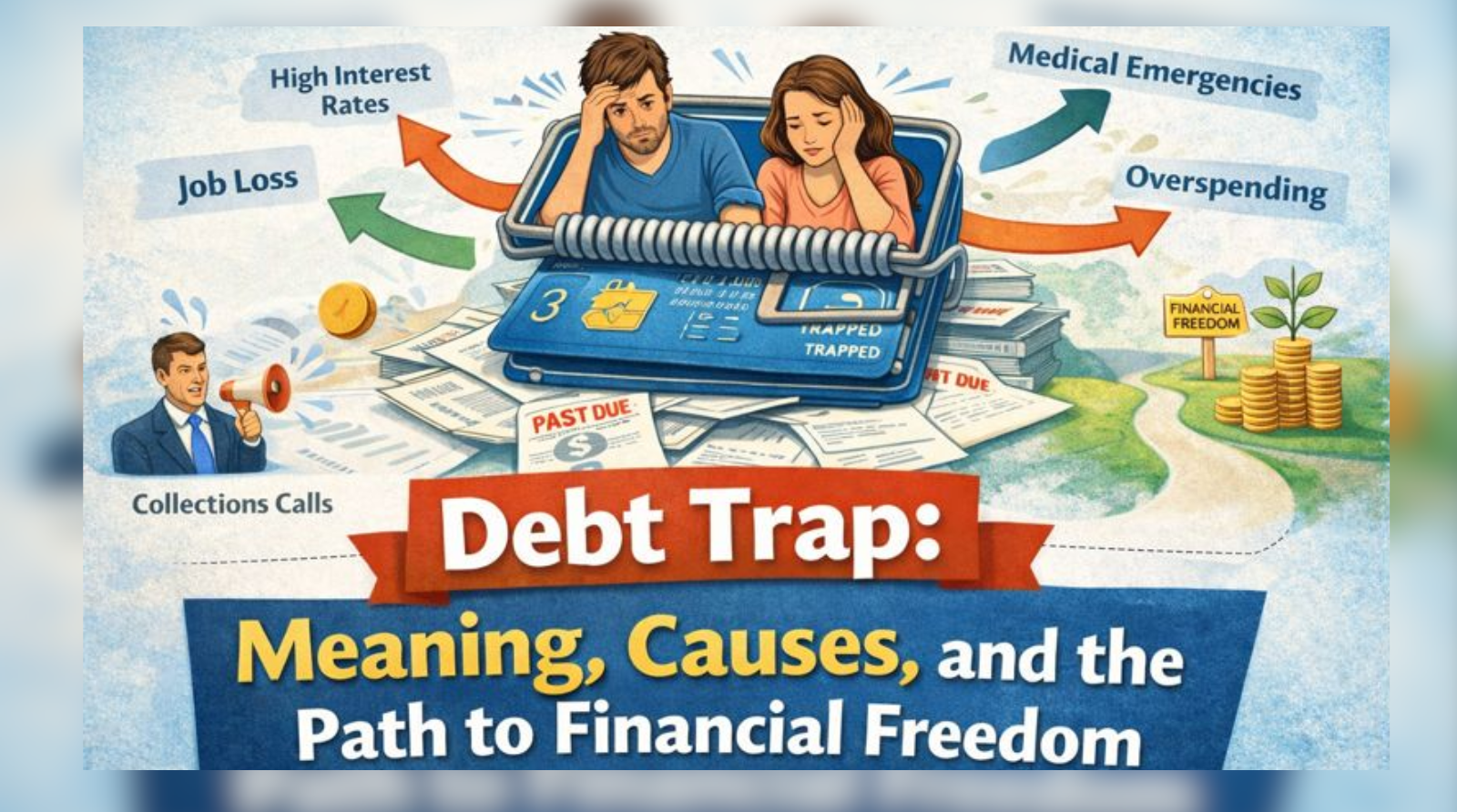

Debt Trap: Meaning, Causes, and the Path to Financial Freedom

In today’s fast-paced “buy now, pay later” economy, the line between healthy credit and a soul-crushing financial cycle is thinner than ever. We often hear the term “debt trap” thrown around in news headlines or financial blogs, but what does it actually feel like when you’re inside one?

A debt trap isn’t just a balance on a statement; it’s a systemic failure of cash flow where your obligations outpace your opportunities. Whether you are a student, a farmer, or a middle-class professional, understanding the mechanics of this phenomenon is the first step toward permanent financial sovereignty.

What is a Debt Trap? (Defining the Concept)

A debt trap is a situation where your debt obligations grow faster than your ability to pay them back. It is characterized by the need to borrow more money just to service the interest on existing loans. Imagine trying to bail water out of a sinking boat with a spoon while the hole in the hull keeps getting wider. That is the essence of a debt trap.

The core definition involves the Debt-to-Income (DTI) ratio. When your DTI exceeds 40-50%, and your interest rates are in the double digits, you are no longer building a future; you are merely funding your past.

The Anatomy of the Trap: Why it Happens

1. High-Interest Compounding

The biggest culprit is often the “minimum payment” trap. Credit card companies are experts at calculating a payment that covers the interest and perhaps 1% of the principal. If you have a $5,000 balance at 24% APR and only pay the minimum, you could be paying that debt for over 20 years.

2. The Psychology of Credit

We live in a world designed to separate us from our money. Digital wallets and “one-click” checkouts remove the “pain of paying.” When we don’t feel the physical loss of cash, our brains don’t register the long-term impact of the debt.

3. Stagnant Wages vs. Inflation

While the cost of living—housing, healthcare, and education—has skyrocketed, real wages for the average worker have remained relatively flat for decades. This “scissors effect” forces families to use credit to bridge the gap for basic necessities.

Specific Types of Debt Traps

The Student Loan Crisis

Higher education was once the “great equalizer.” Today, it is a primary entry point into the debt cycle. Many graduates enter the workforce with six-figure debt and entry-level salaries that barely cover the interest. Learn how to Navigate Federal Student Loan Repayment.

The Agricultural Debt Cycle

Farmers are uniquely vulnerable. They face high “input costs” (seeds, machinery, fertilizer) and unpredictable “output values” (crop prices). A single season of drought can lead to a lifetime of debt to local moneylenders.

Payday Loans and Predatory Lending

Perhaps the most malicious form of the trap, payday loans can carry APRs as high as 400%. These are designed to be “rolled over,” meaning the borrower pays a fee to delay the payment, which only compounds the total owed.

Identifying the Red Flags

How do you know if you are just “in debt” or truly “trapped”? Look for these warning signs:

- You use one credit card to pay off another.

- You are consistently late on utility bills to prioritize loan payments.

- You have no idea what your total debt balance actually is because you’re too afraid to look.

- Collection agencies have started calling your phone.

- You have zero emergency savings.

5 Steps to Break the Cycle Forever

Step 1: Radical Transparency

You cannot fight an invisible enemy. Open every envelope. Log into every portal. Create a spreadsheet that lists:

- The Creditor

- The Total Balance

- The Interest Rate (APR)

- The Minimum Monthly Payment

Step 2: The “Burn” Phase (Budgeting)

You must spend less than you earn. There is no magic trick. This might mean “lifestyle deflation”—cutting subscriptions, cooking at home, or selling items you don’t use.

Step 3: Choose Your Strategy (Snowball vs. Avalanche)

- The Debt Snowball: Pay the smallest balance first. The psychological win of seeing a debt disappear completely provides the “dopamine hit” needed to stay motivated.

- The Debt Avalanche: Focus on the debt with the highest interest rate. This is the mathematically superior method, saving you the most money over time.

Step 4: Negotiate and Consolidate

Call your banks. Tell them you are struggling. Often, they would rather lower your interest rate to 10% than have you default and give them nothing. Alternatively, look into a Debt Consolidation Loan, but only if the interest rate is significantly lower than your current cards.

Step 5: Increase Your “Gap”

To pay off debt faster, you need more income. Whether it’s a side hustle, overtime at work, or selling a car you can’t afford, every extra dollar should go directly to the principal of your debt.

The Role of Financial Literacy

Most people fall into debt traps because they were never taught how money works. Schools teach us how to solve for $X$ in an equation but not how to read a credit card statement. Understanding the Rule of 72 and the power of compound interest (working for you vs. against you) is essential for long-term wealth.

For more information on consumer rights and protections against predatory lending, you can visit the Consumer Financial Protection Bureau (CFPB) or check out the global debt statistics on the World Bank Database.

10 Frequently Asked Questions (FAQs)

1. Is all debt bad?

No. “Good debt” is typically low-interest and used to buy assets that grow in value, like a mortgage or a business loan. “Bad debt” is high-interest and used for depreciating assets like clothes or vacations.

2. How does a debt trap affect my credit score?

Initially, high utilization lowers your score. If you start missing payments, your score can tank by hundreds of points, making it harder to get lower-interest loans in the future.

3. Can I settle my debt for less than I owe?

Yes, it’s called debt settlement. However, it often requires you to be behind on payments first, which damages your credit, and the forgiven amount may be considered taxable income.

4. What is the “minimum payment trap”?

It is a tactic used by lenders where the required payment is just enough to keep the account current but not enough to significantly reduce the principal balance, keeping you in debt for decades.

5. Should I stop contributing to my 401k to pay off debt?

Usually, you should at least contribute enough to get your employer’s match—that’s a 100% return on investment. Anything above that can be redirected to high-interest debt.

6. Does filing for bankruptcy stop the debt trap?

Bankruptcy is a “reset button.” It stops collections and can discharge certain debts, but it remains on your credit report for 7-10 years and won’t fix the underlying spending habits.

7. Why do payday loans have such high interest?

Because they are “unsecured” and high-risk for the lender. They target individuals with poor credit who have no other options, creating a “poverty tax.”

8. Can debt be inherited?

In most cases, no. Your heirs are not responsible for your personal debts unless they co-signed. However, the debt will be paid out of your “estate” (your assets) before heirs receive anything.

9. How do I deal with the mental stress of debt?

Debt is a leading cause of anxiety and depression. The best remedy is a plan. Once you have a written path to freedom, the “unknown” factor disappears, reducing stress significantly.

10. How long will it take to be debt-free?

With a focused plan (like the Avalanche method), most people with moderate debt can become debt-free in 2 to 5 years. It requires consistency over intensity.

Final Thoughts

Escaping a debt trap isn’t just about math; it’s about a change in mindset. It’s moving from a “borrower” mentality to an “owner” mentality. By identifying the traps early, using proven repayment strategies, and educating yourself on the mechanics of interest, you can reclaim your financial future.

The path is long, but the peace of mind that comes with owning 100% of your paycheck is worth every sacrifice.