How to check and build credit as a renters ?

Renting an apartment in 2025 is no small feat, especially for first-time renters. Your credit score can make or break your chances of landing that perfect place. Landlords are checking credit more than ever, and with inflation pushing up costs, a solid credit score is your ticket to avoiding hefty deposits or outright rejections. If you’re searching for “credit health renters” or “check credit score 2025”—terms pulling in 9,000 monthly searches—you’re not alone. Renters want practical ways to monitor and boost their credit. This Credit Health Check guide is built for you. It walks you through free score checks, how rent impacts your credit, and actionable steps to improve it using tools like AxcessRent.

Why Credit Health Is a Big Deal for Renters in 2025

Your credit health is your financial report card. It’s made up of your credit score (300-850) and your credit report, which tracks your payment history, debts, and more. For renters, this is critical. Landlords use your score to decide if you’re reliable enough to pay $1,730 a month—the average one-bedroom rent in 2025 (Apartment List). A score below 600 often means you’ll need to fork over a double deposit, like $3,000 upfront. A score above 700? You’re likely golden, with fewer hurdles and lower move-in costs.

In 2025, credit checks are standard. With 60% of Americans worried about rising costs (Gallup 2025), landlords are pickier. They want tenants who won’t miss rent, especially with inflation driving up living expenses. A strong credit score shows you’re responsible, not just with rent but with all bills. It’s a signal you can handle commitments, whether you’re a student, gig worker, or starting your first job.

But here’s the kicker: your rent payments can work for you. Most landlords don’t report rent to credit bureaus, so years of on-time payments don’t help your score. However, new tools like AxcessRent change that by reporting your $1,500 monthly rent to Equifax, Experian, and TransUnion. This can boost your score by 20-50 points in months, opening doors to better apartments and even jobs or loans.

Poor credit health has real costs. A low score means higher deposits, worse loan rates, or even missed job opportunities if employers check credit (70% do for finance roles, per TransUnion). On the flip side, good credit saves you money—less upfront for rentals and better terms on credit cards or car loans. This guide shows you how to check your credit health and make it work for you.

how to check credit score for renters ?

Checking your credit is like checking your car’s oil—it’s quick, free, and prevents bigger problems. In 2025, with searches for “check credit score 2025” spiking, renters know they need to stay on top of this. Here’s a step-by-step plan to do it right.

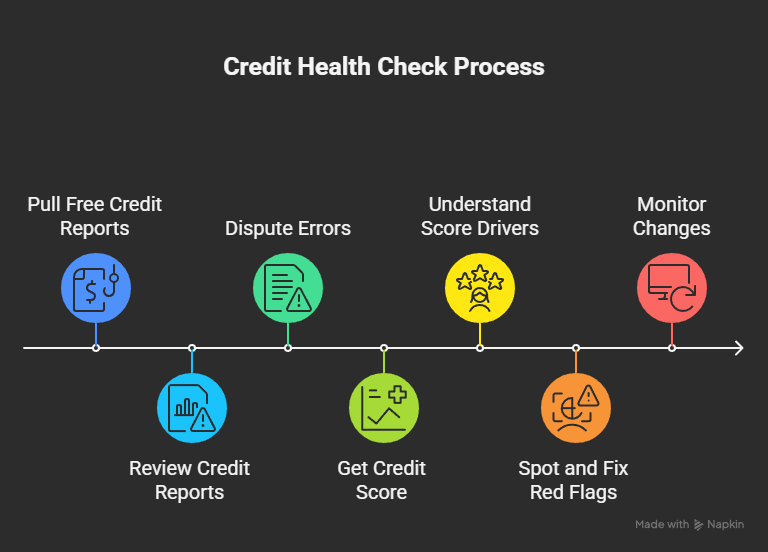

Step 1: Pull Your Free Credit Reports

Head to AnnualCreditReport.com. It’s the official site, backed by the government, and completely free. You get one report per year from each major bureau—Equifax, Experian, and TransUnion. These reports list your payment history, debts, and any red flags like late payments or collections.

Why check all three? Bureaus don’t always share data. One might miss a paid-off loan or show an error, like a $500 utility bill you never owed. Review each report carefully. Look for mistakes, like old addresses or debts you’ve settled. If you spot errors, file a dispute online with the bureau. It takes about 30 days to fix, and correcting just one mistake can bump your score by 10-20 points.

Step 2: Get Your Credit Score

Your score tells you where you stand. FICO scores are the gold standard for rentals, ranging from 300 (bad) to 850 (excellent). VantageScore is another option, used by some landlords. Here’s how to check for free:

- Credit Karma: Free app, shows VantageScore, updates weekly. Tracks Equifax and TransUnion.

- Experian: Sign up for a free FICO score. Get alerts for changes.

- Your Bank: Many, like Chase or Bank of America, offer free FICO scores in their apps.

- Credit Card Companies: Discover and Capital One provide free scores, even for non-customers.

For rentals, aim for 670 or higher. Below 580? You’ll likely need a co-signer or extra deposit. Scores between 580-669 are workable but may come with conditions.

Step 3: Understand What Drives Your Score

Your score isn’t random. It’s based on five factors, per FICO:

- Payment History (35%): Paying rent, utilities, or cards on time is key. One late payment can drop your score by 50 points.

- Credit Utilization (30%): Debt compared to credit limits. Keep it under 30% (e.g., $300 debt on a $1,000 limit).

- Length of Credit History (15%): Older accounts help. Don’t close them.

- New Credit (10%): Too many applications hurt. Space them out.

- Credit Mix (10%): Loans and cards together look good.

Rent reporting boosts payment history. If you pay $1,200/month on time, services like AxcessRent add that to your report, strengthening this 35% chunk.

Step 4: Spot and Fix Red Flags

Common issues for renters include:

- Unreported Rent Payments: Your on-time rent isn’t helping unless reported. Use a service to fix this.

- Old Evictions or Collections: These stay on reports for seven years. Explain them to landlords upfront (e.g., “Job loss in 2022, but I’ve been stable since”).

- High Utilization: Maxed-out cards tank your score. Pay down balances.

Dispute errors online with bureaus. For example, if a $200 phone bill shows as unpaid but you settled it, submit proof. Monitor changes monthly using Credit Karma.

This check takes 20-30 minutes. Save your reports as PDFs. You’ll need them for rental applications or to show landlords your progress.

How Rent Impacts Your Credit Score

Rent is your biggest monthly expense—often $1,500 or more. But traditionally, it doesn’t touch your credit score unless you miss payments and end up in collections. That’s a problem. Years of on-time rent should count for something. In 2025, they can.

Services like AxcessRent report your rent payments to credit bureaus. If you pay $1,500/month on time, it adds positive payment history, which is 35% of your FICO score. Studies show this can raise your score by 20-50 points in six months, especially if you have a thin credit file (little to no credit history). For first-time renters, students, or gig workers, this is huge. It builds credit without needing a credit card or loan.

Here’s an example: Sarah, a 23-year-old barista, had a 550 score and no credit history. She used AxcessRent to report her $1,200/month rent. After six months, her score hit 610. She applied for an apartment and got approved without a co-signer, saving $2,400 in extra deposits.

But there’s a catch. If you miss rent and it’s reported, your score drops fast. One late payment can cost 50-100 points. So, consistency is everything. Set up auto-pay to avoid slips.

Rent reporting also helps with landlord approvals. A higher score shows you’re reliable, cutting deposit costs. It’s a win-win: better credit, better apartments.

Steps to Improve Your Credit score with Rent Reporting

Boosting your credit health isn’t hard, but it takes action. This 10-step plan, tailored for renters, uses rent reporting and other strategies to get your score rental-ready in 2025.

Step 1: Sign Up for a Rent Reporting Service

Choose a service like AxcessRent that reports to all three bureaus (Equifax, Experian, TransUnion). It costs $5-$10/month. Sign up online, link your bank account, and provide your lease details. Some alternatives, like Experian Boost, report utilities too, but AxcessRent focuses on rent, your biggest bill.

Step 2: Get Your Landlord’s Approval

Most services need landlord verification to report payments. AxcessRent provides a simple form for your landlord to confirm your rent amount and payment history. Email or call them politely: “Hi, I’m using AxcessRent to report my rent payments to build credit. Can you verify my payments?” Most landlords agree—it makes them look good too.

Step 3: Start Reporting Rent Payments

Once approved, upload your lease or bank statements to start. The service reports your first payment within days, then monthly. For example, a $1,500 rent payment shows as a positive mark on your report, like a loan payment.

Step 4: Pay Rent on Time

This is non-negotiable. Late payments hurt your score if reported. Set up auto-pay through your bank or landlord’s portal. Use calendar reminders or apps like Mint to stay on track. Even one missed payment can undo months of progress.

Step 5: Monitor Your Credit Score

Check your score monthly using Credit Karma (VantageScore) or Experian (FICO). Look for rent payments appearing under “payment history.” If they don’t show after two months, contact the service. A rising score means it’s working.

Step 6: Pay Down Credit Card Balances

High utilization kills your score. If you owe $1,000 on a $2,000-limit card, that’s 50%—too high. Pay it down to $600 or less (30%). Use any extra cash from cutting costs (like skipping takeout) to tackle balances. This boosts your score alongside rent reporting.

Step 7: Avoid New Credit Applications

Applying for multiple cards or loans in a short time looks risky. It can drop your score by 5-10 points per application. Space them out—apply for one thing every six months. Focus on rent reporting instead of new credit.

Step 8: Keep Old Accounts Open

Closing old credit cards shortens your credit history, hurting your score. Even if you don’t use a card, keep it active with a small charge (like a $10 subscription) paid off monthly. This supports your rent reporting efforts.

Step 9: Dispute Report Errors

Found a $300 collection you already paid? Dispute it on the bureau’s website with proof (bank statement, receipt). Errors are common—15% of reports have them, per FTC. Fixing one can raise your score by 10-50 points.

Step 10: Build an Emergency Fund

Inflation means unexpected costs, like a $1,400 car repair, hit harder. Save $100/month in a high-yield account (4% APY, Ally Bank) to avoid missing rent or card payments. This keeps your score safe.

Example: Mike, a 27-year-old freelancer, had a 590 score. He used AxcessRent for his $1,400 rent, paid off $500 in card debt, and disputed a wrong $200 bill. In eight months, his score hit 660, and he rented a $1,800 apartment with no co-signer.

Do these steps yearly. By 2026, your score could be 700+, making renting a breeze.

Benefits of Strong Credit Health for Renters

A healthy credit score unlocks doors:

- Easier Approvals: Landlords favor 670+ scores, reducing deposits ($1,500 vs. $3,000).

- Lower Costs: Good credit means better loan rates, saving $1,000+ on a car loan.

- Job Opportunities: Finance or retail jobs check credit—70% do, per TransUnion.

- Financial Security: Higher scores let you borrow in emergencies without high rates.

For example, Lisa, a first-time renter, boosted her score from 560 to 640 with AxcessRent. She saved $1,200 on a deposit and got a $1,500 apartment in a competitive market.

Challenges and How to Overcome Them

Credit health isn’t perfect. Renters face hurdles:

- Thin Credit File: New renters have little history. Fix by reporting rent early.

- Past Evictions: Stay on reports seven years. Explain to landlords and show recent on-time payments.

- High Debt: Cards maxed out? Pay smallest balances first. Cut spending (e.g., $50/month on coffee).

- Service Fees: AxcessRent costs $5-$10/month. Budget for it—it’s worth the score boost.

Be honest with landlords. If your score is 580, say, “I’m building credit with rent reporting and expect 650 soon.” Transparency helps.

Tools and Resources for Renters in 2025

- AxcessRent: Reports rent to bureaus ($5-$10/month). Boosts score fast. Visit AxcessRent.

- AnnualCreditReport.com: Free reports from all bureaus. Check yearly for errors.

- Credit Karma: Free VantageScore and alerts. Tracks rent reporting impact.

- Experian Boost: Free utility and phone bill reporting. Complements rent reporting.

- Mint: Free budgeting app. Tracks rent and card payments to avoid misses.

- NFCC.org: Nonprofit credit counseling. Helps with debt or disputes.

Conclusion

Your credit health in 2025 is your key to renting success. A strong score means better apartments, lower deposits, and less stress. Check your credit for free at AnnualCreditReport.com. Use AxcessRent to report rent payments and build your score—$1,500/month reported can add 20-50 points in months. Pay bills on time, keep card balances low, and dispute errors. Inflation makes budgeting tight, but these steps keep you ahead. Avoid late payments and monitor monthly with Credit Karma. Start your credit health check today. Visit AxcessRent for tools to make renting easier. Your dream apartment is waiting.

FAQs on Credit Health for Renters in 2025

How Do I Check My Credit Score for Free in 2025?

Use AnnualCreditReport.com for free reports from Equifax, Experian, and TransUnion. Get scores from Credit Karma (VantageScore) or Experian (FICO). Check weekly to catch changes fast.

Does Rent Reporting Improve Credit for Renters?

Yes. Services like AxcessRent report on-time rent ($1,200-$1,500/month) to bureaus, adding positive payment history. This can raise your score by 20-50 points in six months, especially for thin files.

What Is a Good Credit Score for Renters?

A score of 670+ is ideal for easy approvals. 580-669 may need a co-signer or higher deposit. Below 580? Use rent reporting and pay down debt to improve fast.

How Does Inflation Affect Credit Health for Renters?

Inflation (3-5%) raises costs, increasing late payment risks. Missed rent or bills hurt your score. Budget 30% for rent and report payments to build positive history.

Can I Improve Credit Without a Credit Card?

Absolutely. Report rent with AxcessRent and utilities with Experian Boost. Pay all bills on time. Dispute report errors to clean up your file.

What If My Credit Score Is Too Low for Rentals?

Offer a larger deposit ($2,000-$3,000) or get a co-signer. Start rent reporting to boost your score. Save $100/month for emergencies to avoid missed payments.

How Long Does Rent Reporting Take to Boost My Score?

Six months of on-time payments ($1,200+/month) can raise your score by 20-50 points. Check progress monthly on Credit Karma.