Budgeting on a Low Income: Simple & easy Budgeting Hacks

Living on a low income can feel overwhelming. When paychecks barely cover necessities, saving money or planning for the future might seem impossible. But here’s the truth: budgeting is even more important when money is tight. By creating a plan, tracking expenses, and using the right tools, you can stretch your dollars further, reduce stress, and build financial stability over time.

This in-depth guide will cover everything you need to know about budgeting on a low income, from practical tips to tools and strategies that make it work. Whether you’re living paycheck to paycheck or simply want to gain better control over your money, these insights will help you make every dollar count.

Why Budgeting Matters on a Low Income

Many people think budgeting is only for those with extra money, but it’s the opposite. If you have limited income, budgeting ensures that you:

- Cover your essentials first.

- Avoid unnecessary debt.

- Identify wasteful spending.

- Save (even a small amount) consistently.

- Gain peace of mind knowing where your money is going.

Without a plan, small overspending can quickly spiral into financial stress. Budgeting is your roadmap — showing you how to use the money you have in the smartest way possible.

Key Components of Successful Budgeting

No matter your income level, every good budget has certain core elements. Here’s what you need:

1. Clear Understanding of Income : Know your exact take-home pay after taxes. If income varies (gig or hourly work), use a monthly average to budget more reliably.

2. List of Essential Expenses : Cover your must-haves first: rent, utilities, groceries, transportation, insurance, and debt payments. These are non-negotiable needs.

3. Tracking Non-Essential Spending : Monitor “wants” like dining out, entertainment, shopping, and subscriptions. Helps identify where you can cut back if money gets tight.

4. Savings & Emergency Fund : Start small — even $10–$20 a month builds the habit and grows over time. This fund protects you from unexpected expenses.

5. Debt Repayment Plan : List all debts, then create a payoff strategy (e.g., snowball or avalanche method). Tackling debt systematically frees up future income.

6. Regular Review : Check your budget weekly or monthly. Adjust for changes like income shifts or new expenses to stay on track.

Remember: Budgeting isn’t about being perfect — it’s about making steady progress and building consistency.

Zero-Based Budgeting: A Popular Approach

One highly recommended method for low-income households is zero-based budgeting. Here’s how it works:

- Every dollar you earn has a job.

- Income – Expenses = Zero.

- At the end of the month, all your money is allocated: to bills, savings, debt, or personal spending.

For example, if you earn $1,500, you might allocate:

- $700 for rent

- $200 for groceries

- $150 for utilities

- $100 for transportation

- $200 for debt repayment

- $100 for savings

- $50 for entertainment

The Drawback of Zero-Based Budgeting

The downside is that it can be rigid. If your income is irregular (common with hourly jobs, freelancing, or gig work), it may feel difficult to plan every dollar. In these cases, you may want to budget based on your lowest predictable monthly income, and treat extra money as a bonus to put toward savings or debt.

Budgeting Tools You Can Use

Budgeting doesn’t have to be complicated. There are plenty of tools to make it easier:

Free Tools

- Spreadsheets (Google Sheets, Excel): Create a simple budget template.

- Envelope System: Put cash into envelopes labeled for different expenses.

- Pen & Paper: Old-school, but effective for some.

Apps & Digital Tools

- Mint: Free, tracks spending and categorizes automatically.

- YNAB (You Need A Budget): Great for zero-based budgeting, though it has a fee.

- EveryDollar: Simple, user-friendly budgeting app.

- Goodbudget: Envelope budgeting in digital form.

The best tool is the one you’ll actually use consistently.

Why Budgeting Is Worth the Effort

Budgeting takes time and discipline, but the payoff is huge:

- Financial Clarity: Know where every dollar is going.

- Less Stress: No more wondering if you’ll make it until payday.

- Better Decision-Making: Helps you say yes or no with confidence.

- Savings Growth: Even small amounts add up over time.

- Improved Credit Health: Consistently paying bills on time helps your credit.

When budgeting becomes a habit, it changes your relationship with money. You stop reacting to money problems and start proactively managing them.

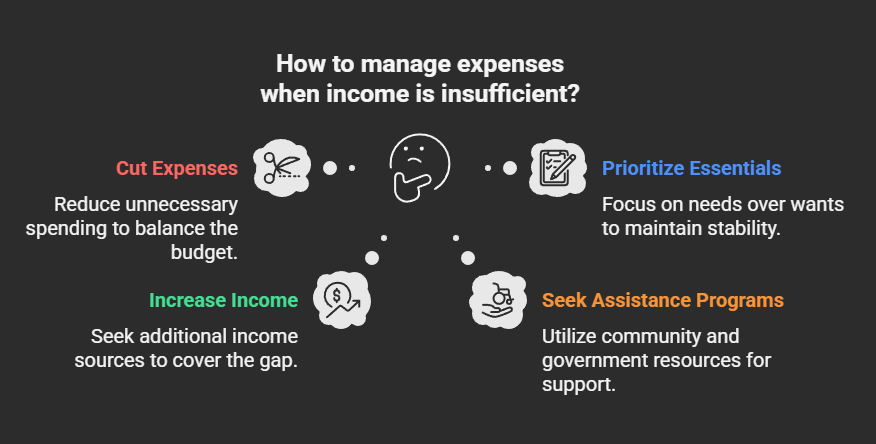

What to Do If Your Income Doesn’t Cover Expenses

Sometimes, even with the best budget, expenses outweigh income. If this is your situation, here’s what you can do:

1. Cut Expenses Where Possible

First step is reducing unnecessary spending. Look at what you can live without or find cheaper alternatives. Even small cuts add up.

- Cancel unused subscriptions (streaming, apps, memberships).

- Cook at home instead of eating out — it’s cheaper and healthier.

- Compare and switch to cheaper phone/internet plans.

- Use public transport, walk, bike, or carpool to save gas and parking.

2. Prioritize Essentials

Focus on needs, not wants. Essentials keep your life stable, while non-essentials can wait.

- Pay for housing (rent/mortgage) first.

- Cover food and groceries.

- Pay utilities (electricity, water, heat, internet if needed for work/school).

- Ensure transportation to work or school.

- Credit cards and loans are important, but if you’re short, contact lenders — many allow payment plans or temporary relief.

3. Find Ways to Increase Income

When expenses exceed income, the other side of the equation is earning more. Extra money helps cover the gap.

- Pick up part-time or gig work (rideshare, delivery, babysitting, tutoring).

- Offer freelance services online (writing, design, coding, admin tasks).

- Sell unused items (clothes, gadgets, furniture) on marketplaces.

- Ask your employer about overtime, extra shifts, or side projects.

4. Seek Assistance Programs

If income and expense cuts still aren’t enough, look into community and government help. These exist for tough times.

- SNAP (food stamps/EBT) for groceries.

- Housing vouchers to reduce rent costs.

- Utility payment help programs to prevent shut-offs.

- Local nonprofits, churches, or charities for food banks, rent help, or emergency grants.

If your income doesn’t cover expenses — cut costs, protect essentials, boost income, and use available resources. Small changes compound into big improvements.

What to Do If You’ve Got a Low Income

Budgeting on a low income requires creativity and persistence. Here are practical strategies:

- Automate Savings: Set up an automatic transfer, even for small amounts.

- Use Cash for Non-Essentials: This prevents overspending.

- Meal Planning: Saves money on groceries and reduces waste.

- Track Every Dollar: Awareness is power.

- Build Credit Smartly: Services like rent reporting can help you improve your credit without debt.

Final Thoughts: Making Every Dollar Count

Budgeting on a low income isn’t easy — but it’s possible. By tracking spending, using budgeting tools, cutting unnecessary expenses, and finding creative ways to save, you can take control of your finances. Over time, even small steps add up to big progress.

Remember: it’s not about how much money you make, it’s about how you manage the money you have.

Take the first step today. Create a simple budget, review it weekly, and stick with it. Consistency is the key to financial freedom, no matter your income level.

FAQs

1. Can you really save money on a low income?

Yes. Even if it’s only $5–$20 a month, savings build financial security and form a lifelong habit.

2. How much should I spend on rent if I have a low income?

The general rule is to keep rent under 30% of your income, but in high-cost areas this may not be realistic. Focus on affordability within your situation.

3. Should I focus on paying off debt or saving first?

Ideally, do both. Start with a small emergency fund ($500–$1,000), then focus on debt repayment while continuing small savings contributions.

4. What if my income changes every month?

Base your budget on your lowest reliable income, and treat anything extra as a bonus.

5. What’s the easiest budgeting method for beginners?

The 50/30/20 rule is simple:

- 50% for needs

- 30% for wants

- 20% for savings and debt