Auto Loan Finance: Guide to Smart Financing

Introduction: The Significance of the Auto Loan

For the vast majority of consumers, a vehicle is the second most expensive purchase they will ever make, trailing only the purchase of a home. However, while mortgage processes are highly regulated and standardized, the auto finance industry is a complex landscape of varying interest rates, hidden fees, and aggressive sales tactics. Understanding the nuances of auto finance is not just about getting a lower monthly payment; it is about protecting your net worth and ensuring that a depreciating asset does not become a permanent anchor on your financial future.

Preparing for an Auto Loan – The Foundation

Assessing Financial Readiness

Before you ever browse an online inventory or set foot on a dealership lot, you must conduct a rigorous internal audit of your finances. Many consumers make the mistake of working “backward”—they find a car they love and then try to squeeze the payment into their budget. Financial success requires the opposite approach.

1. Calculating Take-Home Income and Recurring Expenses Your “take-home” pay is your net income after taxes, health insurance, and retirement contributions. This is your actual liquid capital. To establish a safe car payment, you must first list all non-negotiable expenses: housing, utilities, groceries, student loans, and existing insurance.

2. The 10-15% Total Cost Rule A common pitfall is budgeting only for the loan payment. A vehicle’s true cost includes fuel, maintenance, registration, and a significant jump in insurance premiums. A safe monthly range for the entire transportation category is 10-15% of your net income. If you bring home $4,000 a month, your total car-related spend should cap at $600. If insurance is $150 and gas is $100, your loan payment should not exceed $350.

Defining Purchase Limits

The Danger of “Payment Shopping” Dealerships will often ask, “What monthly payment are you looking for?” This is a trap. By extending the loan term to 72 or 84 months, a dealer can fit an expensive car into a “low” monthly payment, while the consumer ends up paying thousands more in interest. Always define your limit by the Total Purchase Price.

The Role of the Down Payment The down payment serves as an immediate equity shield. Because a new vehicle can depreciate by 20% the moment it leaves the lot, a 20% down payment ensures you are not “underwater” (owing more than the car is worth) on day one. For used vehicles, 10% is often sufficient, but more is always better to reduce the total finance charge.

Credit & Loan Readiness

Your credit score is the single most powerful factor in determining your interest rate. A “Prime” borrower (720+) might see an APR of 5%, while a “Subprime” borrower (<600) could face 15% to 20%.

- Pre-approval: Before visiting a dealer, secure a pre-approval from a credit union or bank. This transforms you into a “cash buyer” in the eyes of the dealer, stripping them of the ability to mark up the interest rate for extra profit.

Evaluating Vehicle Costs – New vs. Used

Financing a New Vehicle

New vehicles come with the allure of the latest technology and the security of a manufacturer’s warranty. From a finance perspective, they often qualify for the lowest interest rates—sometimes even 0% APR during promotional periods.

However, the “Hidden Tax” of a new vehicle is Depreciation. Depreciation is a non-cash expense, but it is real. If you finance $40,000 for a car that is worth $25,000 three years later, you have “lost” $15,000 in wealth. When financing a new car, the loan term should never exceed the warranty period; otherwise, you may find yourself paying for a car that requires expensive out-of-pocket repairs.

Financing a Used Vehicle

Used vehicles (pre-owned) offer a superior value proposition because the previous owner has already absorbed the steepest part of the depreciation curve.

- The Interest Trade-off: Lenders charge higher interest rates for used cars. This is because the collateral (the car) is riskier. If the car breaks down and the owner can’t afford the repair, they are more likely to default on the loan.

- Maintenance Budgeting: A used car loan must be accompanied by an emergency repair fund. If your used car payment is $100 cheaper than a new car payment, that $100 should be directed into a savings account for future tires, brakes, and mechanical issues.

New vs. Used Decision-Making

The “Best Value” is often a 2-3 year old vehicle that has just come off a lease. These vehicles are usually well-maintained, have lower mileage, and have already lost the initial 30-40% of their value, yet they are still modern enough to be reliable.

Navigating the Purchase Process

Negotiation Fundamentals

Negotiation is not just about the price of the car; it is about the Out-the-Door (OTD) Price. The OTD price includes the vehicle cost, sales tax, documentation fees, and registration.

Dealer Pricing Strategies: Dealers use “loss leaders” (cars priced at or below cost) to get you into the building, then make their profit on financing, trade-ins, and add-ons. To counter this:

- Negotiate the car price first.

- Negotiate the trade-in value second.

- Negotiate the financing last (using your pre-approval as a floor).

Avoiding Costly Mistakes

- Emotional Attachment: Salespeople are trained to build “mental ownership.” Once you imagine yourself driving the car, you are less likely to walk away from a bad financial deal.

- The Trade-In Trap: Dealers may offer you a great price on your new car but underpay you for your trade-in. Always check the independent market value (e.g., KBB or NADA) for your current vehicle before the meeting.

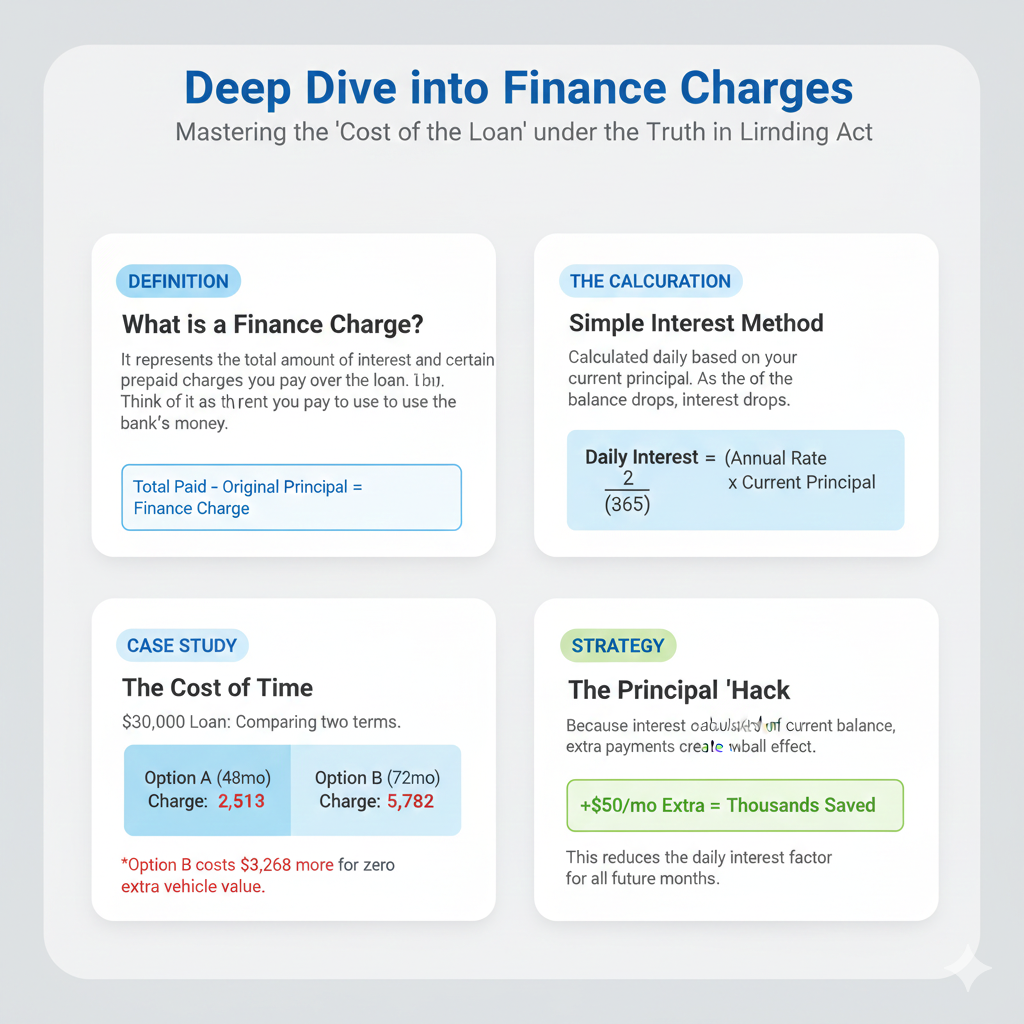

Deep Dive into Finance Charges

What exactly is a Finance Charge?

Under the Truth in Lending Act, lenders must disclose the Finance Charge. This is the “cost of the loan” expressed as a dollar amount. It represents the total amount of interest and certain prepaid finance charges you will pay over the life of the loan, assuming you make every payment on time.

How Finance Charges are Calculated: The Simple Interest Method

Most modern auto loans use the Simple Interest method. Unlike a credit card (which uses average daily balance) or some older “pre-computed” loans, simple interest is calculated based on the principal balance on the day the payment is received.

The Mathematical Formula

To understand your finance charge, we first look at the daily interest factor:

Because the principal balance drops every month, the amount of your monthly payment going toward interest decreases, while the amount going toward the principal increases. This process is called Amortization.

Step-by-Step Calculation of Total Finance Charge

- Determine the Monthly Payment ($M$): Using the standard amortization formula:

- P = Principal (Loan Amount)

- r= Monthly Interest Rate (Annual Rate / 12)

- n = Total Number of Months

2. Calculate Total Payments:

- Total Paid = M*n

3. Identify the Finance Charge:

- Finance Charge = Total Paid – Original Principal

Comprehensive Example

Imagine you are purchasing a vehicle with a $30,000 loan amount. You are offered two different loan terms:

Option A: 48-Month Loan at 4% APR

Monthly Payment: $677.37

Total Paid: $677.37 × 48 = $32,513.76

Finance Charge: $2,513.76

Option B: 72-Month Loan at 6% APR

(Rates are usually higher for longer terms)

Monthly Payment: $496.98

Total Paid: $496.98 × 72 = $35,782.56

Finance Charge: $5,782.56

The Lesson: By choosing the “lower” monthly payment in Option B, you are paying $3,268.80 more in finance charges. This is money that provides zero value to the vehicle itself—it is purely the cost of the time you are taking to pay it back.

Finalizing the Loan & Contract

Reviewing the Loan Agreement

Before signing, you must verify that the numbers on the contract match the verbal agreement.

- The Federal Truth in Lending Disclosure: This box at the top of the contract lists four critical numbers: APR, Finance Charge, Amount Financed, and Total of Payments.

- Check for “Add-ons”: Often, items like “Window Etching,” “Paint Protection,” or “Identity Theft Protection” are slipped into the principal balance. These increase your finance charge because you are now paying interest on these extras.

Optional Products: Value vs. Cost

- GAP Insurance: If your loan is for more than 80% of the car’s value, GAP insurance is vital. It covers the “gap” between what you owe and what insurance pays if the car is totaled. However, buying this through your own insurance provider is often 50-70% cheaper than the dealer’s price.

- Extended Warranties (VSCs): A Vehicle Service Contract can be useful for used cars, but read the exclusions. Many “bumper-to-bumper” warranties exclude the parts most likely to break.

Post-Purchase Management

Strategic Repayment

Because auto loans use simple interest, you can “hack” the finance charge. By paying just $50 extra toward the principal each month, you reduce the balance faster. Since the next month’s interest is calculated on that smaller balance, more of your future payments go toward the principal, creating a snowball effect of savings.

Refinancing

If your credit score improves significantly after 12 months of on-time payments, you can refinance your auto loan with a different lender (usually a credit union) to secure a lower APR. This can save hundreds in remaining finance charges.

Final Knowledge Check: Key Takeaways

- Budgeting: Use take-home pay, not gross income. Aim for the 10-15% total transportation cost rule.

- Credit: Your credit score is the primary lever for the Finance Charge. Pre-approval is your best defense.

- Finance Charges: These are the total cost of borrowing. Longer terms = higher charges.

- Simple Interest: Interest is calculated daily. Paying early or paying extra reduces the total interest paid.

- Contract Review: Never sign a contract where the OTD price or APR differs from what was discussed.

By treating auto finance as a mathematical exercise rather than a shopping experience, you ensure that your vehicle remains a tool for freedom rather than a source of financial stress.