Account Fundamentals: Mastering Checking Accounts for Financial Control

Managing your money effectively begins with mastering your checking account. This account is more than just a place to hold cash; it is the central operational hub for your entire financial life, facilitating payments, tracking spending, and helping you avoid bank fees.

This ultimate guide will break down the essential functions of a checking account, explain how debit cards work, and detail the critical federal protections in place to safeguard your funds.

Essential Functions of a Checking Account

Checking accounts are the command center of your daily financial life. They provide the most liquid funds for routine expenses, offer essential documentation for tax purposes, and are critical for avoiding bank fees and managing cash flow.

A checking account is crucial for secure, modern financial management. It allows you to:

- Pay Bills Securely: Facilitates electronic and paper payments, eliminating the need to handle large amounts of cash and providing a traceable record for dispute resolution.

- Track Expenses: Provides a clear, documented record of all money flowing in and out of your possession, which is vital for budgeting and tax preparation.

- Establish Banking History: Creates a history of responsible use, which can be necessary for opening other financial products like savings accounts or securing loans.

- Receive Direct Deposits: Get your paycheck, tax refunds, or government benefits deposited automatically, often up to 2 days earlier than paper checks, improving cash flow.

Debit Cards: Your Digital Cash

Debit Cards Explained: Immediate Deduction

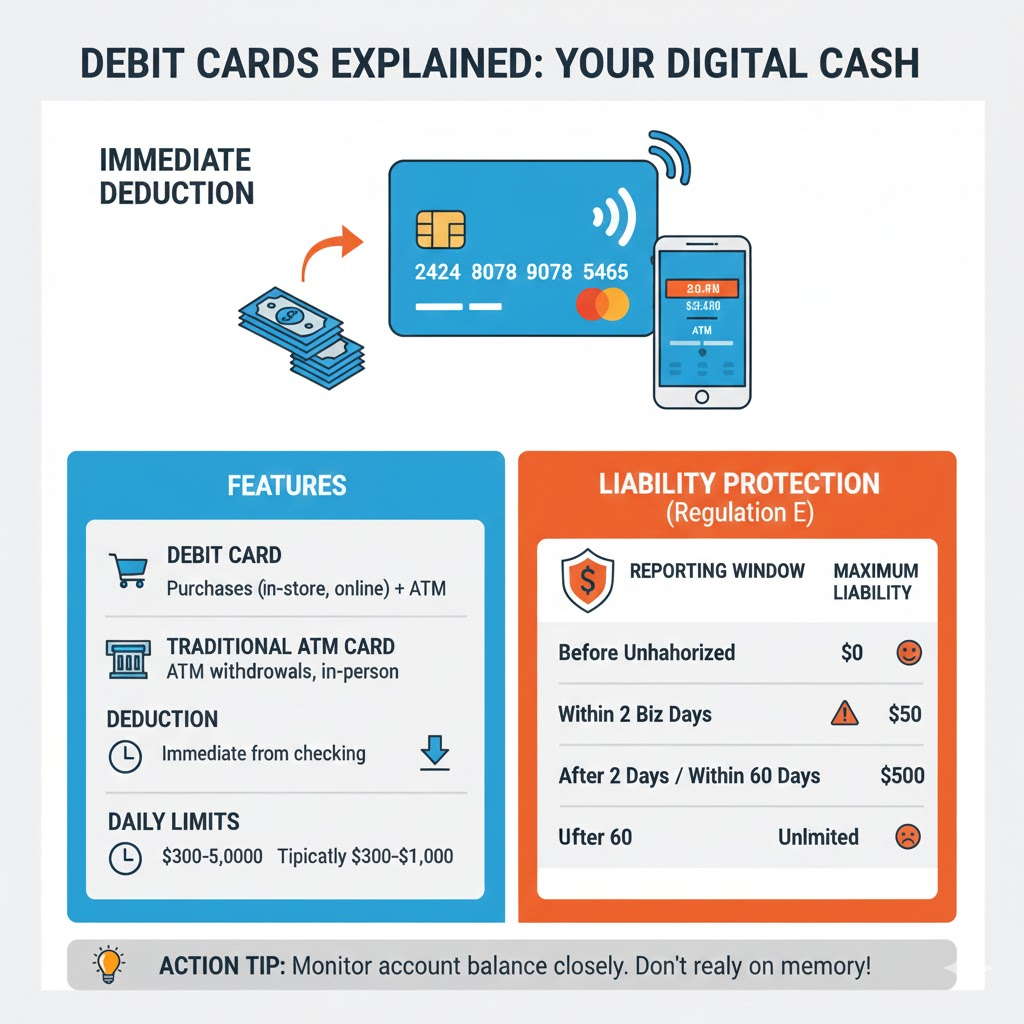

A debit card is a payment instrument issued by your bank that is directly linked to your checking account balance. When you use a debit card, the funds are immediately deducted from your available balance. This process is known as immediate deduction, and it means you are spending the funds you currently possess, unlike a credit card, which uses borrowed money.

| Feature | Debit Card | Traditional ATM Card |

|---|---|---|

| Usage | Purchases (in-store, online) and ATM withdrawals | ATM withdrawals and sometimes in-person bank transactions |

| Deduction | Immediate deduction from checking account | Immediate deduction from checking account |

| Liability | Limited (see liability limit below) | Highly variable, often less protected |

| Daily Limits | $300–$5,000 depending on bank | Typically lower, often $300–$1,000 |

Debit Card Liability Protection (Regulation E)

It is a common misconception that debit cards offer no fraud protection. Federal law, specifically Regulation , provides robust consumer protections if your debit card is lost or stolen. The speed at which you report the loss dictates your maximum financial liability:

| Reporting Window | Maximum Liability |

|---|---|

| Before Unauthorized Transactions | $0 Liability |

| Within 2 Business Days of learning about loss/theft | $50 Maximum |

| After 2 Business Days but within 60 Days of statement showing transfer | $500 Maximum |

| After 60 Days from statement date | Unlimited Liability (you could be responsible for all losses) |

Action Tip: Always monitor your account balance, especially after using your debit card for purchases. Relying solely on your memory or a single check of the balance days after a transaction is the fastest way to incur fees or exceed your liability protection window.

Choosing the Right Account Type

Not all checking accounts are created equal. Different accounts are designed to serve different financial needs, risk tolerances, and activity levels. Choosing the right one is a key step in managing checking account effectively.

| Account Type | Best For | Typical Requirements | Key Feature/Drawback |

|---|---|---|---|

| Basic Checking | First-time account holders, minimal transactions, or those with past banking issues. | Low or no minimum balance requirement. | Few fees, but typically offers no interest. |

| Interest-Bearing | Those who maintain higher average balances and wish to earn yield. | High minimum balance (e.g., $1,500+) or high activity (e.g., 20+ debits per month). | Earns interest, but fees for falling below the minimum can be substantial. |

| Student Account | College students, first banking experience, limited income. | Proof of current enrollment (Student ID). | Low or no monthly maintenance fees until a specified date (often graduation). |

| Senior Account | Adults aged 55 or older. | Age 55+, sometimes requires maintaining a minimum deposit balance. | Reduced fees, free basic checks, and often slightly higher interest rates. |

| Online Checking | Tech-savvy users who rarely visit physical branches. | No in-person branch access required. | Often features higher interest rates and lower fees due to reduced overhead costs for the bank. |

Mastering Daily Account Management

Choosing the right account type is only the first step. True financial control comes from mastering daily habits that prevent costly errors.

The Importance of Reconciliation

Reconciling your account (comparing your bank’s statement against your personal records) should be a weekly or bi-weekly habit. This process:

- Confirms Transaction Accuracy: Ensures every transaction listed is one you authorized.

- Identifies Bank Errors: Catches mistakes made by the bank itself.

- Prevents Overdrafts: Allows you to identify pending debits or outstanding checks that have not yet cleared, providing a more accurate “true” available balance.

Understanding Check Float Risk

In the past, customers would “float” a check—writing a check today and relying on the 3- to 5-day delay (the “float”) before the check physically cleared to deposit funds.

Why this is dangerous now: Modern electronic processing, image clearing, and instant ACH transfers have virtually eliminated the float time. If you write a check today, it can be electronically deposited and debited from your account immediately. Relying on the float is a high-risk way to incur a Non-Sufficient Funds (NSF) fee when the check bounces.

The Most Effective Strategy: Automation and Monitoring

To maximize successful managing checking account while minimizing fees:

- Automate Fixed Bills: Set up auto-pay for utilities, rent, and loan payments directly from your checking account. Schedule the payments to draft 3-5 days before the due date.

- Set Up Low Balance Alerts: Use your bank’s mobile app to receive instant alerts if your account balance drops below a set threshold (e.g., $100).

- Separate Savings: Keep your emergency fund and long-term savings in a dedicated high-yield savings account. This prevents accidental spending and allows your checking account to function purely as a transaction hub.

By understanding the rules of the checking account—especially the difference between immediate deduction and the protection provided by Regulation E—you create a secure and stable financial foundation.

Frequently Asked Questions (FAQ)

What is the minimum balance I should keep in my checking account to avoid fees?

This depends entirely on your bank’s fee schedule. Most banks waive monthly maintenance fees if you maintain a certain daily minimum balance (e.g., $500 or $1,500) or meet specific activity requirements (e.g., direct deposit). Always review your account’s terms and conditions. As a general rule, maintain at least $100–$200 above your expected monthly expenses as a buffer against unexpected charges or timing mismatches between income and bills.

How long does it take for a deposited check to clear and be available in my account?

Federal law requires banks to make the first $225 of a deposited check available by the next business day. For the remaining funds, the standard wait time is usually 2 to 5 business days, though checks over $5,525 may be subject to longer holds. Always confirm your bank’s specific hold policy.

If I have an NSF fee, is it better to close the account immediately?

No. Closing an account while it has an unpaid negative balance is a guarantee that the bank will report you to the consumer banking database (ChexSystems), which will prevent you from opening a new account at almost any other major institution for up to five years. You must pay the full negative balance and all fees before closing the account formally.

How can I get an NSF fee waived by my bank?

You should call your bank immediately, apologize for the oversight, and politely request a “one-time courtesy waiver.” Banks often grant this if you are a long-time customer with a history of good account management and if this is your first NSF fee.

Is it safer to use a debit card or a credit card for online purchases?

A credit card is generally safer for online purchases. With a credit card, you are using the bank’s money, and your maximum liability for fraud is typically $0 by policy. With a debit card, fraudsters gain access to your actual checking funds, which, although protected by Regulation E, can cause immediate financial disruption while the fraud claim is processed.

I reconcile my account with my mobile app. Is a checkbook register still necessary?

While your mobile app shows posted transactions, a physical or digital checkbook register is still recommended for tracking pending transactions (like recent debits or written checks) that have not yet cleared the bank’s system. This prevents you from overdrawing the account based on the mobile app’s balance alone.

What specific negative actions will land me in the ChexSystems database?

The primary action that leads to a ChexSystems report is failing to pay off a negative balance (due to overdraft fees, NSF fees, or service charges) when the bank closes your account. Misuse, chronic overdrafts, or suspected fraud can also lead to reporting.

If I lose my debit card, what are the first two things I should do immediately?

- Call your bank immediately to report the card lost or stolen.

- Review your most recent transactions for any unauthorized activity. Reporting the loss within two business days is crucial to limiting your liability to just $50.

How often should I check my checking account balance?

Ideally, you should check your balance daily, especially if you use a debit card or have automated payments set up. Consistent, daily monitoring is the best defense against unexpected fees, unauthorized transactions, and overdrafts.

Knowledge Check

Test your understanding of checking account management with these 8 questions.