How College Financial Aid Works and How to Qualify?

The cost of higher education has outpaced inflation for decades, transforming the search for financial aid from a simple paperwork exercise into a high-stakes strategic operation. To navigate this landscape successfully, one must move beyond a surface-level understanding and master the three pillars of funding: Grants, Scholarships, and Loans. This guide provides an exhaustive analysis of these categories and a tactical roadmap for where and how to secure them.

Discover the key types of college financial aid, how to navigate applications, and strategies to increase your chances of qualifying for support.

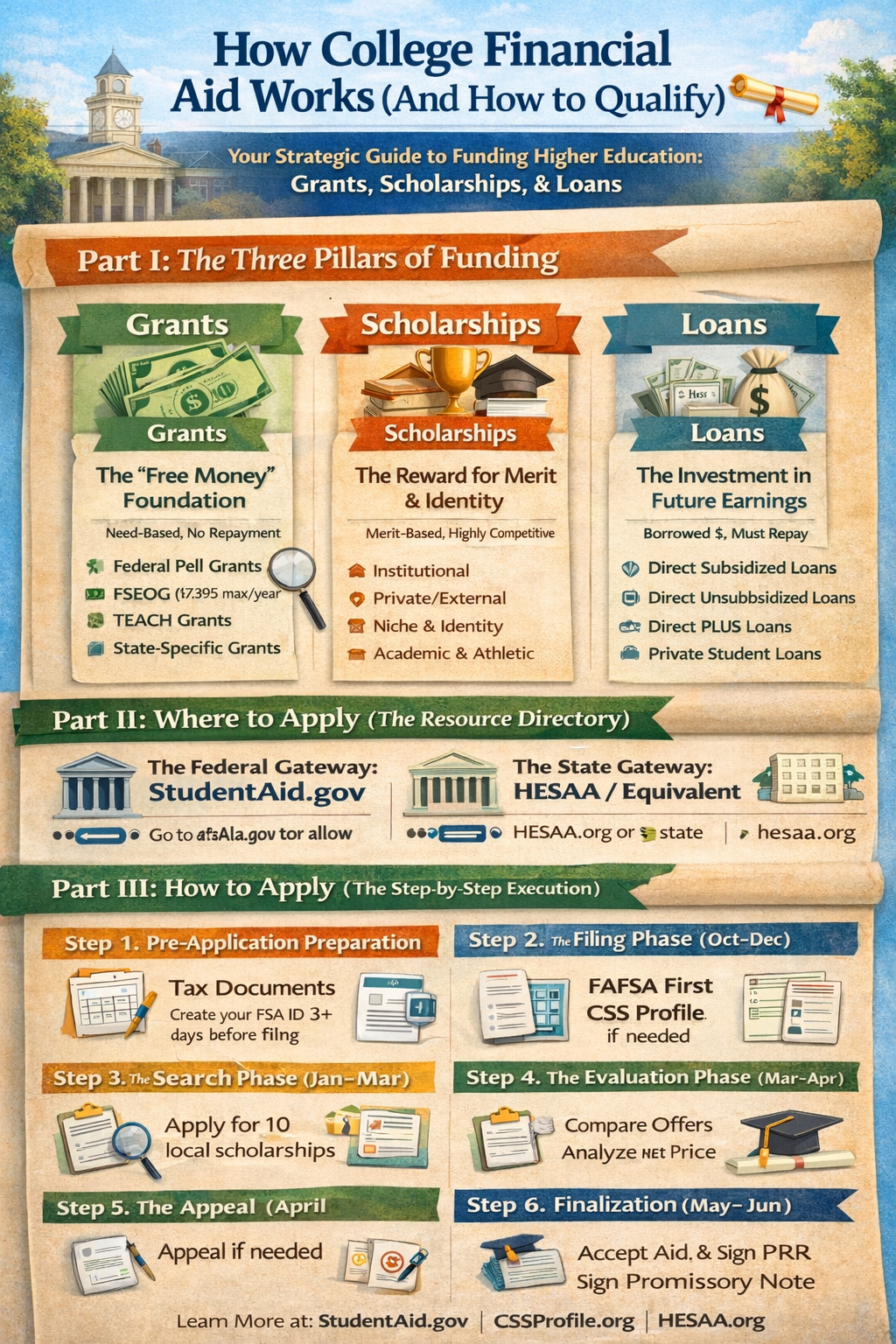

Part I: The Three Pillars of Funding

1. Grants: The “Free Money” Foundation

Grants are typically need-based forms of financial aid that do not require repayment. They are the bedrock of accessibility for low-to-middle-income families.

- Federal Pell Grants: The most significant source of federal grant aid. The amount changes annually; for the 2024–2025 award year, the maximum is $7,395. It is only available to undergraduate students who display exceptional financial need and have not earned a bachelor’s or professional degree.

- Federal Supplemental Education Opportunity Grant (FSEOG): This is a campus-based aid program. Unlike the Pell Grant, which is guaranteed to every eligible student, FSEOG funds are limited. Each participating school receives a certain amount; once it’s gone, no more awards are made for that year.

- Teacher Education Assistance for College and Higher Education (TEACH) Grants: These are unique because they require a service obligation. You must agree to teach in a high-need field in a low-income area for at least four years. If you fail to meet this obligation, the grant converts into a Direct Unsubsidized Loan with back-dated interest.

- State-Specific Grants: Most states offer grants to residents attending in-state colleges. For example, the Cal Grant in California or the TAP grant in New York. These often have strict GPA requirements in addition to financial need.

2. Scholarships: The Reward for Merit and Identity

While grants focus on “need,” scholarships focus on “merit” or “characteristic.” They are highly competitive and require proactive searching.

- Institutional Scholarships: These are awarded by the college itself. They are often the largest source of funding outside of federal aid. “Full-ride” or “Full-tuition” scholarships usually fall into this category.

- Private/External Scholarships: These come from corporations (like the Coca-Cola Scholars Program), non-profits, or community groups. They range from $500 to $50,000.

- Niche and Identity Scholarships: These are based on specific traits—ethnicity, religion, sexual orientation, or even unique hobbies (like the famous scholarship for duck calling).

- Academic and Athletic Scholarships: Reserved for top-tier students or athletes. Note that athletic scholarships are often “one-year renewable” contracts, meaning they can be revoked if a student is injured or leaves the team.

3. Loans: The Investment in Future Earnings

Loans are borrowed money that must be repaid with interest. Understanding the nuances of loan types is critical to avoiding a lifetime of debt.

- Direct Subsidized Loans: The “Best” Loan. The U.S. Department of Education pays the interest while you’re in school at least half-time, for the first six months after you leave school, and during a period of deferment.

- Direct Unsubsidized Loans: Available to both undergraduate and graduate students; there is no requirement to demonstrate financial need. You are responsible for paying the interest during all periods.

- Direct PLUS Loans: These are for parents of dependent undergraduate students or for graduate students. They have higher interest rates and require a credit check.

- Private Student Loans: Issued by banks or credit unions. These should be a last resort, as they lack the flexible repayment plans and forgiveness programs (like Public Service Loan Forgiveness) offered by federal loans.

Part II: Where to Apply (The Resource Directory)

Success in financial aid is determined by knowing which “gatekeepers” hold the funds. There are four primary locations you must visit:

1. The Federal Gateway: StudentAid.gov

This is the “Control Center.” Here, you will:

- Create your FSA ID (a legal electronic signature).

- Submit the FAFSA.

- Complete Entrance Counseling for loans.

- Sign your Master Promissory Note (MPN).

2. The Institutional Gateway: The CSS Profile

Managed by the College Board, the CSS Profile is used by roughly 400 private colleges and universities to award their own institutional wealth. Unlike the FAFSA, which is free, the CSS Profile has a fee (though waivers are available for low-income families).

3. The State Gateway: Higher Education Student Assistance Authority (HESAA/Equivalent)

Every state has its own agency. For example, if you live in New Jersey, you use the HESAA portal. If you live in Texas, you look at the “College for All Texans” website. These portals often require a separate application after the FAFSA is processed.

4. The Scholarship Aggregators

To find private scholarships, you should use “Search Engines” rather than just Google:

- Fastweb: The oldest and most robust database.

- College Board BigFuture: Excellent for matching with scholarships based on your profile.

- Going Merry: A “Common App” for scholarships that allows you to apply to multiple awards with one form.

Part III: How to Apply (The Step-by-Step Execution)

Step 1: Pre-Application Preparation (August – September)

Before the forms even open, you must gather your “Prior-Prior” year tax returns. If you are applying for college in Fall 2025, you need your 2023 tax data.

- Action: Create your FSA ID at least 3 days before you plan to file. The Social Security Administration needs time to verify your identity.

Step 2: The Filing Phase (October – December)

- FAFSA First: Complete the FAFSA as soon as it opens. Use the IRS Direct Data Exchange (DDX) tool to automatically pull your tax information into the form. This reduces errors and the likelihood of being selected for “Verification.”

- CSS Profile Second: If your schools require it, file this simultaneously. Be prepared to answer questions about your home’s value, retirement savings, and medical expenses.

Step 3: The Search Phase (January – March)

While you wait for your college acceptance letters, focus on external scholarships.

- The “Rule of 10”: Aim to apply for 10 local scholarships. These have a much higher ROI than national scholarships because you are only competing against students in your town or county.

- Check Portals: Log into the “Financial Aid Portal” of every college you applied to. They often have separate, internal scholarship applications with deadlines in February.

Step 4: The Evaluation Phase (March – April)

You will receive a Financial Aid Award Letter from each school that accepts you.

- Analyze the “Net Price”: Do not look at the total aid amount. Look at the Sticker Price minus Gift Aid (Grants/Scholarships). This is your “Net Price.”

- Compare Work-Study: See if you were offered Federal Work-Study. This is a job on campus that helps pay for books and personal expenses.

Step 5: The Appeal (April)

If your top-choice school gave you less money than a competitor, or if your family’s income has dropped since 2023, you must write an Appeal Letter.

- How: Contact the Financial Aid Office. Provide “Documentation of Changed Circumstances” (e.g., layoff notice, medical bills). Be polite but firm.

Step 6: Finalization (May – June)

- Acceptance: Log into the portal of the school you chose and “Accept” the grants and subsidized loans. You can “Decline” the unsubsidized loans or parent loans if you don’t need them.

- Master Promissory Note: If taking loans, you must sign this legal document agreeing to pay them back.

Part IV: Critical Pitfalls to Avoid

- Missing Deadlines: Many states have “Priority Deadlines” as early as December or January. Missing these can cost you $5,000+ in state grants.

- Paying for the FAFSA: The first “F” in FAFSA stands for Free. Any website asking for money to file the FAFSA is a scam.

- Underestimating the “Gaps”: Some colleges “gap” students—they admit you but don’t give you enough money to attend. Always have a “financial safety school” (usually a community college or state school) where you know the aid will cover the cost.

- Ignoring the SAI: Your Student Aid Index (SAI) is a number the FAFSA gives you. Understanding this number allows you to predict your aid before you even apply. A lower SAI equals more aid eligibility.

Conclusion

Financial aid is not a gift; it is a system that must be managed. By strategically utilizing the FAFSA for grants, targeting local scholarships for merit aid, and using federal subsidized loans as a last resort, you can minimize the financial burden of your degree. Start early, document everything, and never accept the first offer as final.

Frequently Asked Questions (FAQs)

Q: Do I need to be a straight-A student to receive financial aid?

No. While “merit-based” scholarships often require high GPAs or test scores, “need-based” aid (like Pell Grants and Federal Loans) is primarily based on your family’s financial situation. However, you must maintain “Satisfactory Academic Progress” (usually a 2.0 GPA) to keep your aid once you are in college.

Q: My parents make too much money for a Pell Grant. Should I still file the FAFSA?

Absolutely. Even if you don’t qualify for need-based grants, most colleges require a FAFSA on file to award institutional merit scholarships. Furthermore, the FAFSA is the only way to access Federal Direct Loans, which offer lower interest rates and better protection than private bank loans.

Q: What is the difference between an “Independent” and “Dependent” student?

Most students under 24 are considered “Dependent,” meaning their parents’ income must be reported. You are only “Independent” if you are 24 or older, married, a veteran, a graduate student, or meet specific criteria like being an orphan or ward of the court. Living on your own or paying your own bills does not make you independent in the eyes of the Department of Education.

Q: If I win a $1,000 private scholarship, does my college reduce my other aid?

This is called “Scholarship Displacement.” Some colleges will reduce your “Self-Help” aid (loans or work-study) first, which is good. Others might reduce your institutional grants. Always check with the school’s financial aid office about their policy on outside awards.

Q: Can I get financial aid for Summer classes?

Yes, but it is limited. Most students use their full year’s worth of Pell Grants and loans during the Fall and Spring semesters. If you plan to attend Summer school, you may need to “save” some of your aid eligibility or apply for a Year-Round Pell Grant if you meet specific credit-hour requirements.

Q: What happens to my financial aid if I transfer schools?

Financial aid does not “follow” you automatically. You must add the new school’s code to your FAFSA, and the new school will calculate a completely new aid package based on their own available funds and tuition costs.

Q: Do I have to pay taxes on my scholarships?

Scholarship money used for tuition, fees, books, and required equipment is usually tax-free. However, any portion of a scholarship used for “Room and Board” (housing and food) is considered taxable income by the IRS.