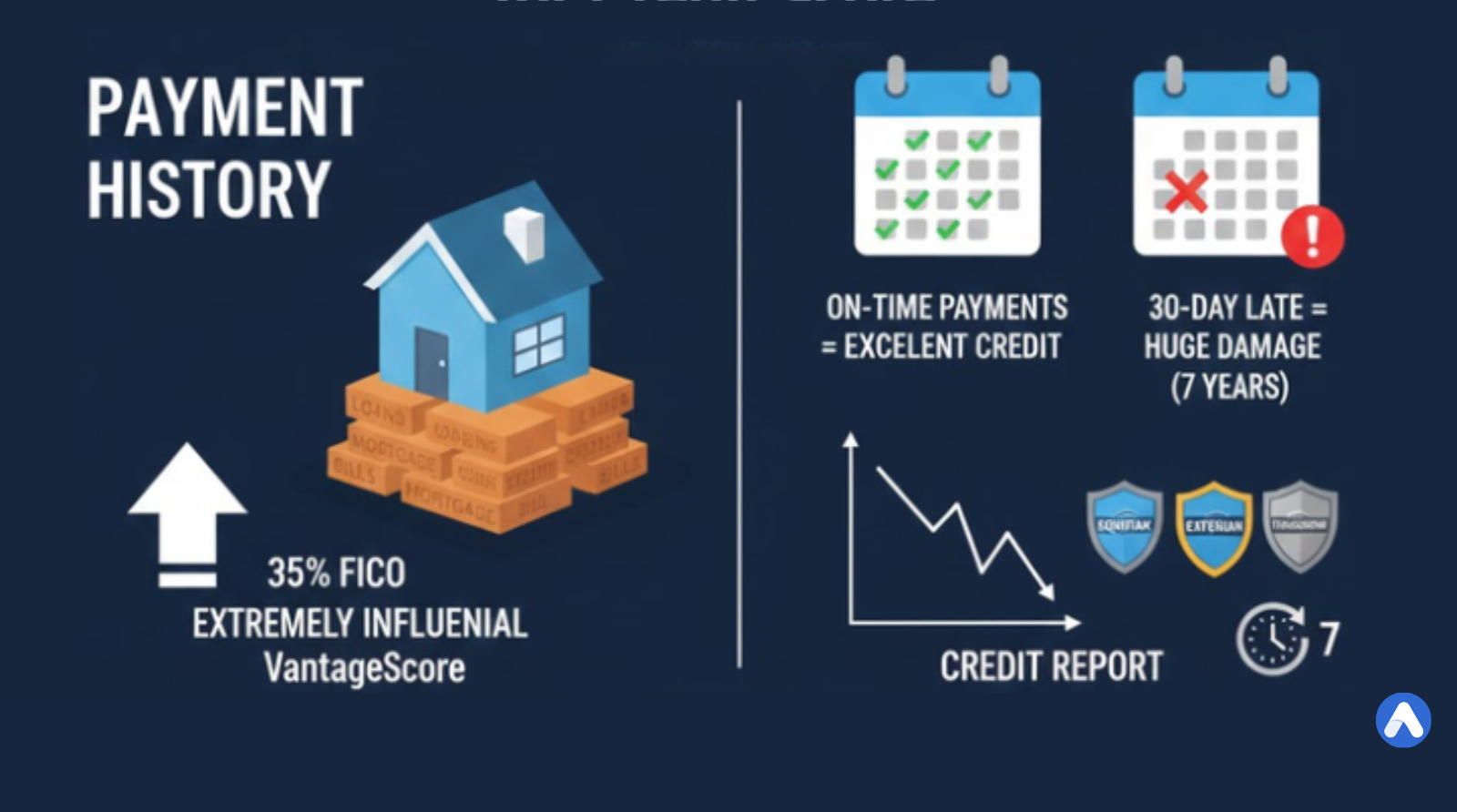

What Is Payment History and It’s importance for Credit Score

If your credit score were a house, your Payment History would be the foundation. It is the single most important factor determining your creditworthiness, making up the largest percentage of both FICO and VantageScore models.

A pristine payment history signals reliability and responsibility, granting you access to the best interest rates. Conversely, a single late payment can wipe out months—or even years—of effort, significantly raising your cost of borrowing.

What is Payment History?

Payment history is a comprehensive record of how you have repaid your debt obligations over time. Every major lender, credit card company, and installment lender reports your activity to the three major credit bureaus (Equifax, Experian, and TransUnion) every 30 to 45 days.

This history covers two main types of accounts:

- Revolving Accounts: Such as credit cards and lines of credit.

- Installment Accounts: Such as mortgages, car loans, student loans, and personal loans.

For each account, your history notes whether the payment was made on time or if it was marked as late, and by how many days.

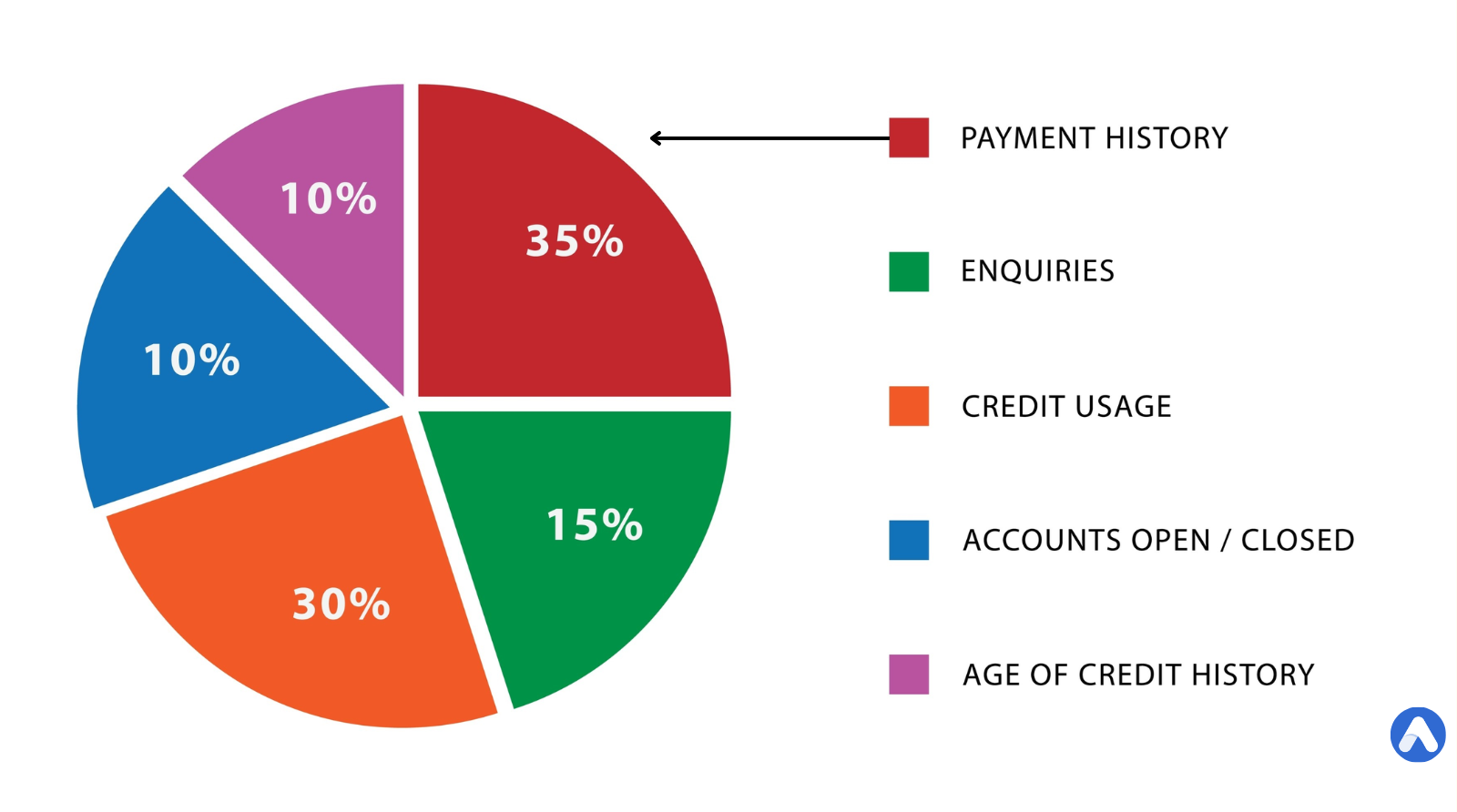

The Weight: Why Payment History is King

Payment history holds the largest weighting in the two primary scoring models used by lenders:

1. FICO Score

In the dominant FICO Score model (e.g., FICO Score 8), Payment History accounts for 35% of your total score. This high weighting emphasizes that lenders prioritize predictability above all else. They need assurance that they will get their money back on time.

2. VantageScore

In the VantageScore model, Payment History is labeled as “Extremely Influential,” its highest category. While VantageScore does not use specific percentages, it reinforces that prompt payment is the most critical element.

A perfect payment record is essential for achieving a score in the “Very Good” (740+) or “Exceptional” (800+) ranges.

How Long Does Payment History Stay on Your Credit Report?

Negative marks on your credit report are not permanent, but they do linger for a long time. The rule for almost all negative payment history items is seven years from the date of the first delinquency.

Negative Items and Their Timelines:

| Negative Item | Time on Report | Start Date for Removal |

|---|---|---|

| Late Payment (30, 60, 90 Days) | 7 years | Date the late payment occurred |

| Collection Accounts | 7 years | Date of first missed payment that led to collection |

| Charge-Offs | 7 years | Date of the charge-off |

| Chapter 13 Bankruptcy | 7 years | Date the bankruptcy was filed |

| Chapter 7 Bankruptcy | 10 years | Date the bankruptcy was filed (the longest mark) |

Important Note on Removal: Once the seven-year period passes, the credit bureaus are legally required to remove the negative mark from your report. This removal is often automatic, but it is wise to check your report and ensure expired negative marks have been deleted.

What about Good Payment History?

Positive payment history—all those “paid as agreed” marks—remain on your report indefinitely, as long as the account is open. Even after an account is closed, the positive history stays on your report, contributing to your credit score for up to 10 years, which helps build your Length of Credit History.

How to Fix and Improve Payment History

The goal for improving your payment history is two-fold: prevention for the future and correction for the past.

1. Prevention (The Long-Term Solution)

The best way to improve your payment history is to ensure 100% on-time payments going forward.

- Automate Payments: Set up automatic payments (AutoPay) from your checking account to cover at least the minimum due for all credit cards and loans. This eliminates human error.

- Set Reminders: If you prefer manual payments, set multiple calendar and phone reminders a few days before the due date.

- Change Due Dates: If possible, call creditors and ask to shift your due dates to align with your payday.

A good payment history percentage is anything above 99%. Lenders are looking for perfection.

2. Correction and Fixing Errors

You may be able to correct or mitigate damage from past late payments using these strategies:

A. Disputing Errors (The First Step)

Mistakes happen, especially if you had a credit identity theft event or if a creditor reports the wrong date. If you find a late payment, collection, or charge-off that is incorrect:

- Gather Evidence: Collect any canceled checks, bank statements, or written communication proving you made the payment on time.

- File a Dispute: File a dispute directly with the credit bureau (Experian, Equifax, TransUnion) and provide your evidence. The bureau is legally required to investigate and verify the information within 30 to 45 days. If the creditor cannot verify the late payment, it must be removed.

B. The Goodwill Letter (For Isolated Mistakes)

If you missed a payment legitimately due to a short-term financial hardship (medical bills, temporary job loss, etc.) and you have an otherwise stellar payment history (100% on-time for years), you can write a Goodwill Letter.

- The Strategy: Politely ask the creditor to make a “goodwill adjustment” by removing a single late payment as a courtesy, emphasizing your long history as a reliable customer.

- When to Use: This only works for isolated, minor issues (e.g., one 30-day late payment) and only after the account is current.

C. Pay-for-Delete (For Collection Accounts)

If an old debt has gone to collections, the collection agency may be willing to remove the negative entry in exchange for full payment (or an agreed-upon partial payment).

- Caution: Always get the “pay-for-delete” agreement in writing before you make the payment. If you pay the debt and they refuse to remove the entry, the damage remains, and you lose leverage.

Frequently Asked Questions (FAQ)

What is the difference between a 30-day and a 90-day late payment?

A 30-day late payment will significantly hurt your score, but a 90-day late payment is far more damaging. Missing the payment by 90 days shows an established pattern of default and can drop a high score by 100 points or more.

Does paying off an old collection account help my score?

Paying off an old collection account will update the status from “Unpaid” to “Paid in Full.” This looks much better to a new lender, but it does not remove the negative history. If you can get a “pay-for-delete” agreement, that is the ideal way to fix the issue.

If I pay my bill one day late, will it be reported?

Generally, no. Creditors usually do not report a payment as late until it is 30 days past the due date. Paying one or two days late usually results in a late fee but does not negatively impact your credit score. Always confirm the reporting threshold with your specific creditor.