How to Remove Late Payments from Your Credit Report

Introduction

Late payments show up on your credit report when you miss a bill by 30 days or more. They can drop your score fast. One late might cut it by 60 to 100 points. If your score was good, the hit feels bigger. Lenders look at these marks. They charge higher rates or say no to loans.

You can remove late payments. If they are wrong, dispute them. The Fair Credit Reporting Act lets you do this for free. Accurate ones are harder. They stay seven years. But a goodwill letter might work. It asks the creditor to erase it as a favor.

This guide covers it all. We look at what late payments are. How long they last. Steps to fight errors. How to write goodwill letters. Ways to handle fraud. Tips to stop them next time. By the end, you will know your options. Check your report first. Act soon. Small steps help your score recover.

In 2025, rules have not changed much. The FCRA still protects you. Credit bureaus must check disputes in 30 days. Creditors report to Equifax, Experian, and TransUnion. Get free reports weekly at AnnualCreditReport.com. Spot issues early.

Many people face this. A job loss or medical bill causes a slip. Do not panic. You have tools. Disputes fix errors. Goodwill builds on good history. Start with facts. Pull your reports. Note every late. Gather proofs like bank statements. Then pick your path.

Recovery takes time. New on-time payments help. Scores rise after six months of good habits. But removing a late speeds it up. Lenders forgive old marks more. Focus on what you can control.

What Are Late Payments?

A late payment is any bill missed past its due date. Credit cards, loans, utilities—they all count. Creditors wait 30 days before reporting. Pay in that window, and it stays off your report.

- Reports come in tiers. 30 days late is mild. 60 or 90 days looks worse. Over 90, it might go to collections. That adds another mark.

- Not all lates show the same. A one-day miss triggers fees but not reports. Interest builds if unpaid. Balances grow. Creditors report monthly. Timing varies. One bureau might show it first.

- Check your statements. Match dates. Errors happen. A glitch posts payment late. Or mail delays. These are fixable.

- Late payments tie to payment history. It makes 35% of your FICO score. Miss one, and it drags the rest down. Multiple lates compound it.

Why Do Late Payments Matter?

- They signal risk to lenders. A late says you might miss again. Scores drop. Good scores get 700 or above. Lates push you under.

- Real effects hit hard. Higher car loan rates add thousands over time. Mortgages cost more. Renters face denials. Jobs check credit too. Some fields like finance care.

- Insurance rises. Auto premiums jump 20% or more after a late. It stays seven years. But fresh ones hurt most. After two years, impact fades.

- If scores were low already, one more late stings less. But build from there. On-time payments rebuild trust.

In 2025, economy feels tight. Inflation lingers. More folks miss bills. Reports show 3.5% of accounts late in Q2. Up from last year. Do not let it define you.

How Long Do Late Payments Stay on Your Credit Report?

- Seven years from the first miss. That is the date of delinquency. Pay later, it does not reset the clock. The mark lingers.

- Closed accounts stay 10 years if paid off current. But the late drops at seven. For example, miss in October 2025. It falls off October 2032.

- Collections follow the same. Original date counts. Not when sent to agency.

- Impact lessens yearly. Year one hurts most. By year three, half gone. Scores recover with good habits.

Check yearly. Some marks vanish early if disputed. But accurate ones stick.

Can You Remove Accurate Late Payments?

- No, by law. FCRA says accurate info stays. You cannot force removal.

- But try goodwill. It worked for some in 2025. Creditors like Chase or Capital One respond if you are loyal.

- Explain the why. Job loss? Illness? Be brief. Show it was one time.

- No guarantees. Smaller banks say yes more. Big ones get thousands of requests.

- Odds better for first late. Or if hardship proved. Attach docs.

- If denied, ask why. Follow up. Or try credit counselor.

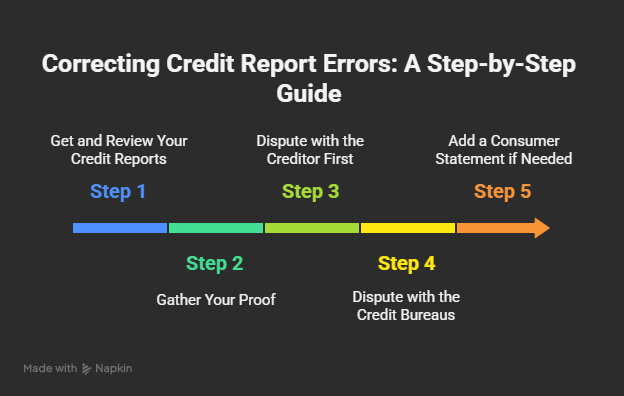

Step-by-Step Guide to Removing Inaccurate Late Payments

Errors pop up. Wrong dates. Mix-ups. Fight them.

Step 1: Get and Review Your Credit Reports

- Pull free reports from AnnualCreditReport.com. Do all three bureaus. Look at every account.

- Spot lates that do not match. Note account number. Date reported. Amount due.

- Differences happen. Fees add up. But if you paid on time, it is an error.

Step 2: Gather Your Proof

- Dig out records. Bank apps show transfers. Emails confirm payments. Canceled checks prove mail.

- Timeline matters. Due date to payment date. Under 30 days? No report needed.

- Save copies. Scan them. You need them for disputes.

Step 3: Dispute with the Creditor First

- Call or write the lender. Say it is wrong. Send proofs.

- They have 30 days to check. If agree, they tell bureaus. Mark gone.

- Track it. Note call dates. Names. Follow up if slow.

Example: Your card says 30 days late in June. But app shows paid May 28. Send screenshot. They fix it.

Step 4: Dispute with the Credit Bureaus

- If creditor ignores, go to bureaus. Each one separate.

- For Experian: Online dispute center. Pick item. Say “not late.” Upload files.

- Equifax: Similar. Mail or phone too.

- TransUnion: App or letter.

- They contact creditor. 30 days max. No proof? Item deleted.

- Get results in mail. Updated report free.

Step 5: Add a Consumer Statement if Needed

- If denied but you disagree, add 100-word note. It explains your side. Shows on reports.

- Lenders see it. Helps context.

Common Pitfalls in Disputes

- Do not skip proofs. Vague claims fail. Be specific.

- One bureau fixed? Check others. Reports differ.

- Wait full cycle. Changes lag.

- If fraud, add police report.

Using Goodwill Letters for Accurate Late Payments

Real lates need a different tack. Goodwill letter asks nice.

What Makes a Goodwill Letter Work?

- It shows remorse. Highlights good history. Promises better.

- Send certified mail. Keep copy.

- Target right person. Billing address or “credit department.”

- Time it. Soon after late. Or on anniversary.

Key Tips for Your Letter

Short. One page. Polite tone.

- Start with account info.

- Admit fault. No blame.

- Explain once. Keep brief.

- List positives. Years on time. High limits.

- Say changes. Autopay set.

- End with clear ask. Remove from all bureaus.

Proofs help. Hardship letter if job loss.

Click Here to Download Goodwill Letter to Remove Late Payments from Your Credit Report

Success stories: Reddit user got Chase to drop a 2019 late in 2025. Said “polite persistence.” Another with Wells Fargo after hardship proof.

If no, try again in six months. Or switch servicers.

Handling Late Payments from Fraud or Identity Theft

Fraud changes everything. You are not liable.

- File police report. Get FTC affidavit at IdentityTheft.gov.

- Send to creditor fraud team. They close account. Tell bureaus to delete.

- Mark gone fast. No seven years.

- Mixed files? Dispute as “not mine.”

- Freeze credit too. Stops new fraud.

The Real Impact of Late Payments on Your Credit Score

- FICO weights payment 35%. VantageScore same.

- One 30-day late: 60-110 point drop. From 750 to 650.

- Multiple: Worse. 90-day: 100+ drop.

- Recovery: Three months of on-time lifts 20-50 points.

- Old lates barely move needle. Under 700 score? Less relative hit.

- Build mix. New card with on-time.

Common Mistakes When Trying to Remove Late Payments

- Rushing disputes without proof. Fails every time.

- Ignoring one bureau. Fix all three.

- Chasing scams. “Credit repair” firms charge for free rights.

- Forgetting follow-up. Calls log progress.

- Assuming goodwill always works. It does not. Have backup plan.

When to Get Professional Help

- DIY first. Free and easy.

- Stuck? Non-profits like NFCC.org. Counselors guide disputes.

- Lawyers for big fraud. But rare.

- Avoid paid repair. CFPB warns of scams.

Tips to Avoid Future Late Payments

- Autopay minimums. Covers basics.

- Alerts: Text or email due dates.

- Buffer fund. One month bills saved.

- Call early. Ask deferral for hardship.

- Bill apps track all. Mint or YNAB.

- Pay twice monthly. Keeps balance low.

Conclusions

Late payments hurt your credit, but you can fix some. Pull free reports from AnnualCreditReport.com. Dispute errors with creditors or bureaus—they must check in 30 days. For real lates, send a polite goodwill letter. Explain once, show your good history, and ask nicely. It works sometimes, like with Chase if you’re loyal. Fraud? File a police report and FTC affidavit—marks vanish fast. Pay on time now. Set autopay and alerts. Your score rises in months. Better credit means lower rates and more yeses from lenders. Check weekly. Small steps add up. Stay steady.

FAQs

How long does a late payment affect my score?

Up to seven years. But most damage in first two. On-time helps quick.

Can I remove lates over seven years old?

They drop auto. Check reports to confirm.

What if dispute denied?

Ask evidence. Resubmit with more proof. Or CFPB complaint.

Do goodwill letters work in 2025?

Yes, sometimes. Better for one-offs. Prove loyalty.

How to dispute online?

Go to bureau site. Upload docs. Takes 10 minutes.

What if late from medical debt?

Dispute errors. Goodwill for accurate. Hospitals offer aid.

Does paying off old late remove it?

No. Mark stays. But stops collections.

Can I add my side to report?

Yes. 100-word statement. Explains context.

How to check if late reported yet?

Wait 30 days. Pull report then.

What counts as hardship for goodwill?

Job loss, illness, divorce. Attach proof.