How long does bankruptcy stay on your credit ?

Filing for bankruptcy is a significant financial decision, often taken as a last resort to gain relief from overwhelming debt. It’s natural to be concerned about the long-term consequences, especially its impact on your credit. The most common question people have is, “How Long Does Bankruptcy Stay on Your Credit Report?”

The short answer is that a bankruptcy can remain on your credit report for 7 to 10 years, depending on the chapter you file. However, that timeline isn’t the whole story. Understanding the nuances is key to managing your financial future.

This definitive guide will break down the exact timelines for different types of bankruptcy, explain how it affects your credit score, and provide a clear, actionable roadmap for rebuilding your credit long before it falls off your report.

What Is Bankruptcy?

Bankruptcy is a legal process to handle debt you can’t pay. It stops collections and may discharge debts. But it stays on your credit report, signaling risk to lenders.

Why People File for Bankruptcy

Common reasons: medical bills (62% of cases), job loss, divorce. It provides relief but has long-term effects.

How Bankruptcy Affects Your Credit

It lowers your score a lot. Chapter 7 drops 200+ points if score was high. Recovery takes time, but possible with good habits.

Understanding Credit Reports and Public Records

Before we dive into the specifics of bankruptcy, it’s crucial to understand where this information comes from. Your credit report is a detailed history of your credit accounts, payment history, and certain public records, maintained by the three major credit bureaus: Equifax, Experian, and TransUnion.

Bankruptcy is a legal proceeding that becomes a public record. The credit bureaus regularly collect data from court records, which is how the bankruptcy appears on your credit file. This entry is one of the most serious negative items you can have, but its impact lessens over time.

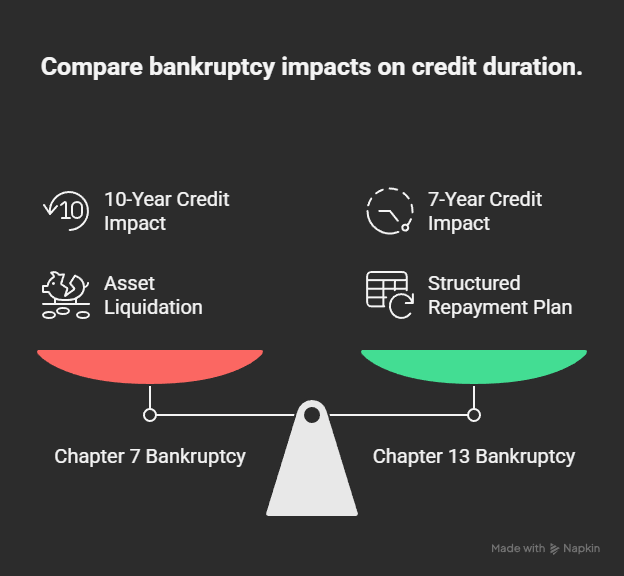

The Standard Timelines: Chapter 7 vs. Chapter 13 Bankruptcy

The length of time a bankruptcy remains on your credit report is federally regulated by the Fair Credit Reporting Act (FCRA). The timeline depends primarily on the type of bankruptcy you file.

What is chapter 7 bankruptcy?

Chapter 7 bankruptcy, also known as “liquidation” or “straight bankruptcy,” involves the court-appointed trustee selling your non-exempt assets to pay back your creditors.

- How Long It Stays: A Chapter 7 bankruptcy will remain on your credit report for 10 years from the filing date of the petition.

- Why It’s Longer: Because Chapter 7 involves the discharge of unsecured debts (like credit cards and medical bills) without a repayment plan, it is considered a more severe event by credit scoring models.

What is chapter 13 bankruptcy?

Chapter 13 bankruptcy, often called a “wage earner’s plan,” involves creating a court-approved repayment plan to pay back all or a portion of your debts over a 3 to 5-year period.

- How Long It Stays: A Chapter 13 bankruptcy will remain on your credit report for 7 years from the filing date.

- Why It’s Shorter: Since you’re making a concerted effort to repay your debts under a structured plan, the credit reporting system treats Chapter 13 more favorably.

Important Note: If you dismiss your Chapter 13 case before completing the plan, the 7-year timeline may reset from the dismissal date, and it could be reported for longer.

Other Types

Chapter 11 for businesses, similar to 13, 7-10 years. Chapter 12 for farmers, rare, same durations.

Bankruptcy Duration Table

| Bankruptcy Type | Duration on Credit Report | Key Features |

|---|---|---|

| Chapter 7 | 10 years | Liquidation, full discharge |

| Chapter 13 | 7 years | Repayment plan, keep assets |

| Chapter 11 | 7-10 years | Business reorganization |

how does bankruptcy work ?

The initial impact of a bankruptcy on your credit score is severe. It’s not uncommon to see a drop of 130 points or more, depending on your starting score. A bankruptcy entry on your report signals to future lenders that you were unable to meet your previous credit obligations.

However, the impact is not static. Its effect diminishes over time. A bankruptcy that is 6 years old will hurt your score far less than one that is 6 months old, especially if you’ve begun establishing a new, positive credit history.

Can You Remove a Bankruptcy Early from Your Credit Report?

Under normal circumstances, you cannot remove a accurately reported bankruptcy before its designated timeline (7 or 10 years). The credit bureaus are legally permitted to report it for that period.

However, there are specific situations where early removal might be possible:

- Inaccurate Reporting: If the bankruptcy is reported incorrectly—for example, the wrong chapter, filing date, or included accounts—you can dispute the error with the credit bureaus. If the information cannot be verified within 30 days, it must be removed.

- Fraudulent Bankruptcy: If a bankruptcy was filed using your identity without your knowledge (identity theft), you can have it removed by filing an identity theft report and disputing it with the bureaus.

Be wary of any company that promises to “erase” accurate bankruptcy information from your credit report for a fee. These are often scams. The only legitimate way to remove an accurate entry is to wait for the legal reporting period to expire.

Your Action Plan: Rebuilding Credit After Bankruptcy

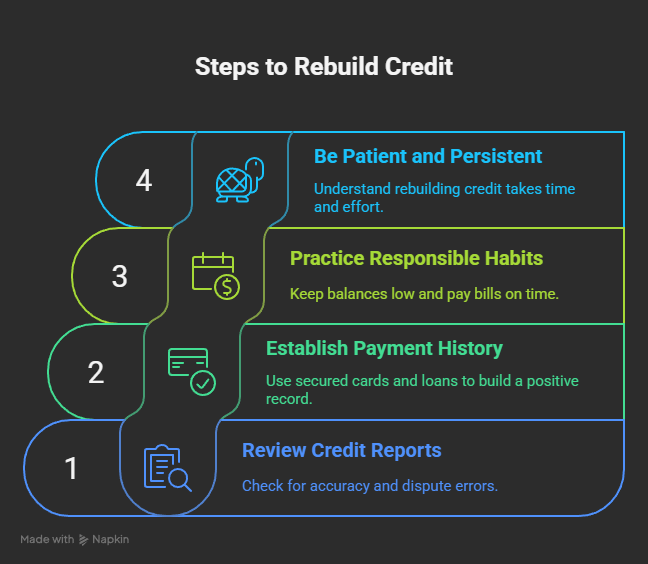

Waiting 7 or 10 years for a bankruptcy to disappear is not a strategy. The most powerful thing you can do is proactively rebuild your credit. Here’s how to start.

1. Review Your Credit Reports Thoroughly

After your bankruptcy is discharged, get free copies of your reports from AnnualCreditReport.com. Check that all accounts included in the bankruptcy are correctly reported as “discharged” or “included in bankruptcy” with a $0 balance. Dispute any inaccuracies.

2. Establish a New Positive Payment History

Your payment history is the most important factor in your credit score. You need to demonstrate that you can manage new credit responsibly.

- Get a Secured Credit Card: This is the most accessible tool post-bankruptcy. You provide a cash deposit as collateral, which typically becomes your credit limit. Use it for small purchases and pay the balance in full every month.

- Consider a Credit-Builder Loan: Offered by many credit unions and community banks, these loans hold the borrowed amount in an account while you make payments. Once paid off, you receive the money, and the positive payment history is reported to the bureaus.

3. Practice Responsible Credit Habits

- Keep Balances Low: Even with a small credit limit, aim to use less than 30% of it. This shows you can manage credit without maxing it out.

- Pay Every Bill on Time: This includes utilities, rent, and your new credit accounts. Consistent, on-time payments are the bedrock of a good credit score.

4. Be Patient and Persistent

Rebuilding credit is a marathon, not a sprint. You likely won’t qualify for prime rates immediately, but after 12-24 months of responsible credit behavior, you may see significant improvements and qualify for better loan products.

Alternatives to Bankruptcy

Before filing for bankruptcy, explore other options. These alternatives can help manage debt without the long-term credit damage bankruptcy causes. They may save money and stress in the long run.

Debt Consolidation

Debt consolidation combines multiple debts into one loan with a single payment. It often lowers interest rates and simplifies finances. Unlike bankruptcy, it doesn’t harm your credit score. You need decent credit to qualify. Payments are more manageable, but you must stick to the plan.

Debt Settlement

Debt settlement involves negotiating with creditors to pay less than you owe. It can reduce debt significantly but hurts your credit score, typically by 50-100 points. It’s less damaging than bankruptcy. You may need a lump sum to settle. It takes time but can work.

Credit Counseling

Credit counseling through nonprofit agencies creates a debt management plan (DMP). They negotiate lower interest rates and fees with creditors. You make one monthly payment. It doesn’t involve filing for bankruptcy, so your credit stays safer. It requires discipline to follow the plan.

Case Studies: Life After Bankruptcy

Bankruptcy isn’t the end. These stories show how people recover. With effort, you can rebuild credit and achieve goals like homeownership or financial stability after bankruptcy.

Chapter 7 Success

Maria, 40, filed Chapter 7 in 2020. Her credit score dropped to 550. She got a secured credit card and paid bills on time. By 2025, her score rose to 680. She bought a home. Hard work and smart financial choices helped her recover.

Chapter 13 Journey

Ben, 35, filed Chapter 13 in 2018. He followed a repayment plan for five years. By 2025, the bankruptcy was removed from his credit report. His score went from 500 to 720. Consistent payments and budgeting made it possible.

Conclusion: Looking Beyond the Bankruptcy

While a Chapter 7 or Chapter 13 bankruptcy can stay on your credit report for up to 10 years, its power to derail your financial life fades much sooner. By understanding the timelines and taking immediate, consistent action to rebuild, you can begin to restore your creditworthiness within a couple of years.

The bankruptcy on your report is a record of your past financial struggles—it does not have to define your financial future. Use the fresh start that bankruptcy provides to build new, healthier financial habits that will serve you for a lifetime.

Frequently Asked Questions

Here are answers to common bankruptcy questions. They explain how it affects credit and life. Knowing the facts helps you make better decisions.

How Long Does Chapter 7 Bankruptcy Stay on Your Credit Report?

Chapter 7 bankruptcy stays on your credit report for 10 years from the filing date. It impacts your ability to get loans or credit cards. Rebuilding credit takes time but is possible with effort.

How Long Does Chapter 13 Bankruptcy Stay on Your Credit Report?

Chapter 13 bankruptcy stays on your credit report for 7 years from filing. It’s shorter than Chapter 7 because you repay some debt. Good financial habits can improve your score during this time.

Does Bankruptcy Affect All Credit Bureaus the Same?

Yes, all major credit bureaus—Equifax, Experian, TransUnion—report bankruptcy the same way. They get the same public record data. The impact on your score is consistent across all three bureaus.

Can Bankruptcy Be Removed Early If Paid Off?

No, bankruptcy stays on your credit report for the full duration—7 or 10 years—regardless of paying debts. Early removal isn’t allowed. Focus on rebuilding credit to lessen its impact.

How Does Bankruptcy Affect Getting a Job?

Bankruptcy can affect job prospects, especially in finance or roles requiring credit checks. Some employers view it as a red flag, but many don’t check. Be honest if asked, and focus on your skills.