Your Credit in Retirement: Why It Still Matters and How to Protect It

Retirement is often thought of as a time to relax, slow down, and enjoy the fruits of decades of hard work. You’ve spent your working years building a nest egg, planning for the future, and managing your money wisely. But even in this new chapter of life, credit in retirement remains surprisingly important. Now that you’re no longer tied to a 9-to-5, it might seem like things like credit scores and financial profiles don’t really matter anymore. After all, if you’re not applying for big loans or buying a new house, why worry about your credit, right?

But here’s the truth: your credit score continues to play an important role even after you retire. It can affect everything from your ability to rent a new apartment, qualify for a car loan, or get approved for a credit card in an emergency. It can even influence your insurance rates or how easily you can sign up for utilities. In some cases, your credit health could determine how prepared you are for the unexpected.

Even if you don’t anticipate needing new credit anytime soon, keeping your score in good shape gives you peace of mind and flexibility—two things that are invaluable in retirement. In this guide, we’ll explore why credit still matters after retirement, what affects it in your golden years, and how you can protect and maintain it without adding stress to your life.

Why Credit Still Matters After You Retire

When you retire, your daily routine may shift. Your job changes from earning a paycheck to managing your savings, investments, and possibly pension or Social Security income. But just because your income changes doesn’t mean your financial needs disappear—and that’s where your credit score can still make a difference.

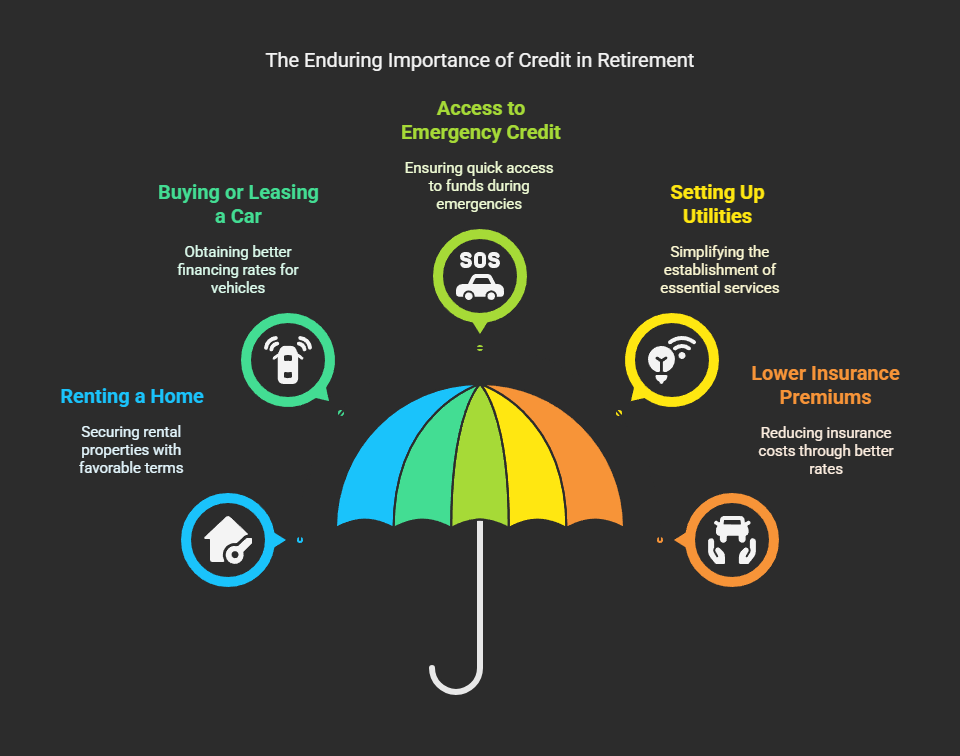

Here are some very real situations in which good credit in retirement is essential for retirees:

Renting a Home or Apartment

Many retirees choose to downsize after the kids move out or relocate to a new city or state for better weather, lower taxes, or to be closer to family. If you’re moving into a rental property, most landlords will run a credit check as part of their application process. A strong credit score can make you a more attractive tenant and help you avoid having to pay a larger security deposit or needing a co-signer.

Buying or Leasing a Car

Whether your current car is on its last legs or you simply want something more comfortable or fuel-efficient, you may still need to finance a vehicle in retirement. And that means a credit check. The better your credit, the lower the interest rate you’ll likely receive—potentially saving you hundreds or even thousands of dollars over the life of the loan.

Access to Emergency Credit

Life is unpredictable. Medical expenses, home repairs, or helping a loved one in a bind can create sudden financial strain. If your savings don’t cover an emergency, a credit card or personal loan could become your backup plan. Good credit ensures you can access those resources quickly and at a lower cost.

Setting Up Utilities and Services

Did you know that utility companies, internet providers, and even cellphone carriers often run credit checks before approving service? Poor credit can mean higher deposits—or even a flat-out denial. Maintaining a decent score helps you keep life’s basics simple.

Lower Insurance Premiums

In many states, insurance companies use credit-based insurance scores to determine your rates for home and auto insurance. Better credit can lead to lower premiums—another way your score can save you money in the long run.

Does Retirement Itself Affect Your Credit Score?

The simple answer is no—retirement itself does not directly impact your credit score. Credit scoring models, like FICO and VantageScore, do not consider whether you’re working or retired. They don’t know your age or your job status. What they care about is how you manage the credit you have.

However, what does change in retirement is how you use credit. And those changes can influence your score.

For example:

- If you start relying more on credit cards to supplement a fixed income, your credit utilization might go up, which could hurt your score.

- If you close old credit cards to “simplify” your accounts, you might reduce your credit history length or available credit, which also impacts your score.

- If your income drops significantly, you might be more likely to miss a payment or carry a balance—two things that negatively affect your credit.

In other words, your lifestyle in retirement—not retirement itself—is what can influence your credit standing.

How to Maintain and Protect Your Credit Score in Retirement

Luckily, maintaining good credit in retirement isn’t complicated. With a few smart strategies and some routine habits, you can keep your score healthy without much effort.

1. Keep Paying Bills on Time

Even one late payment can have a lasting impact on your credit score. Set up autopay for recurring bills or use reminders on your phone or calendar. If you’re helping a spouse or aging parent manage bills, consider consolidating accounts or simplifying the payment process to avoid missing due dates.

2. Watch Your Credit Utilization

Try to keep your credit card balances low—ideally under 30% of your total credit limit, and under 10% if possible. For example, if you have a total credit limit of $10,000, aim to keep your total monthly balance below $3,000 (or even $1,000 for optimal results).

3. Don’t Close Your Oldest Accounts

Your oldest credit accounts help anchor your credit history, which makes up about 15% of your score. Unless an old card has high fees or security risks, keeping it open—even if you rarely use it—can help your credit profile.

4. Limit New Credit Applications

Every time you apply for a new credit card or loan, a “hard inquiry” appears on your credit report. Too many hard inquiries in a short time can make lenders nervous. Only apply for new credit when absolutely necessary.

5. Use Tools Like Rent Reporting

If you’re renting in retirement, services like AxcessRent can help you build and maintain your credit score by reporting your on-time rent payments to the credit bureaus. It’s a great way to boost your score without taking on debt.

6. Monitor Your Credit Regularly

Check your credit reports at least once a year. You can do this for free at AnnualCreditReport.com. Look for errors, unfamiliar accounts, or any suspicious activity. Catching fraud early can save you major headaches.

7. Protect Against Identity Theft

Seniors are often targeted by scammers and fraudsters. Consider placing a credit freeze with the three major credit bureaus if you’re not planning to apply for new credit. This prevents unauthorized access to your credit file.

Why Good Credit Still Matters—Even If You Own Your Home Outright

You might think that once your mortgage is paid off and you’re not planning to borrow again, your credit score no longer matters. But that’s not quite true. Good credit is still an important part of financial wellness by building credit in retirement. Even if you don’t need a loan, credit checks can happen when you sign up for utilities, open a new cell phone plan, apply for homeowner’s or auto insurance, or even rent a car. A strong credit profile can make these tasks smoother and may even help you avoid deposits or extra fees. Think of your credit as a financial safety net—it’s there when you need it, and it’s best to keep it in good shape just in case.

Does Lower Retirement Income Affect Your Credit Score?

It’s a common concern among retirees: “Will my reduced income hurt my credit score?” Fortunately, the answer is no. Credit scoring models like FICO and VantageScore don’t consider your income when calculating your score. What they do evaluate, however, is how you use the credit available to you—your payment history, your credit utilization, and how consistently you manage your accounts. While a lower income won’t hurt your score directly, it could make it harder to stay current on bills or keep balances low, which can indirectly affect your credit. That’s why careful budgeting and responsible credit use are especially important during retirement.

Final Thoughts: Credit Is a Lifelong Asset

Your credit history is more than just a number—it’s a reflection of years of financial behavior, discipline, and trustworthiness. And that doesn’t stop once you retire.

A strong credit profile gives you freedom, flexibility, and protection in retirement. Whether it’s lowering your insurance costs, securing housing, or simply having options when life throws you a curveball, credit can be a powerful tool—especially when used wisely.

At AxcessRent, we’re committed to helping people of all ages build, maintain, and protect their credit through rent reporting and helpful education. Because no matter where you are in life, good credit is always worth protecting.