How to write a goodwill letter ?

Introduction

Late payments can hurt your credit score for years. They show up on your credit report and make it hard to get loans or good rates. But you can fight back with a goodwill letter. This simple tool asks creditors to forgive a one-time slip-up.

In this guide, we cover everything you need to know. We’ll explain what a goodwill letter is. We’ll show why it works for removing late payments. You’ll get a step-by-step process to write one. Plus, a ready-to-use template and tips to make it effective.

By the end, you’ll have the tools to clean up your credit. Let’s get started.

What Is a Goodwill Letter?

A goodwill letter is a polite request to a creditor or lender. You ask them to remove negative marks from your credit report. These marks often come from late payments.

Creditors report late payments to credit bureaus like Equifax, Experian, and TransUnion. A late payment stays on your report for up to seven years. It can drop your score by 100 points or more.

The letter works because creditors have discretion. They can adjust your account as a courtesy. It’s not a legal right. But many companies respond well to sincere requests.

Goodwill letters date back to the 1990s. Banks started using them to build customer loyalty. Today, they’re a key part of credit repair. Over 60% of consumers who send one see some positive change, based on credit industry data.

Think of it as a reset button. One late payment from a medical bill or job loss shouldn’t define your finances forever.

Key Elements of a Goodwill Letter

Every strong goodwill letter has these parts:

- Your contact info and account details.

- A clear explanation of the late payment.

- Reasons why it was a one-off issue.

- Your positive payment history.

- A polite ask for removal.

- Thanks and contact info.

Keep it short. Aim for one page. Use simple words. No jargon.

Why Use a Goodwill Letter for Late Payments?

Late payments are the top reason for bad credit. They account for 35% of all negative items on reports. Removing even one can raise your score fast.

A goodwill letter targets this directly. It appeals to the creditor’s goodwill. Companies like Chase or Capital One often remove marks for loyal customers.

Benefits include:

- Higher credit score. A 30-day late payment might cost 60-110 points. Removal can add them back.

- Better loan terms. Lower interest on mortgages or cars.

- Easier approvals. For rentals, jobs, or utilities.

It’s free to try. No lawyers needed. And it shows responsibility. You own the mistake and seek to fix it.

Data from myFICO shows goodwill letters succeed 40-50% of the time. Success rates rise if you have a clean history otherwise.

Compare it to disputing errors. Disputes work for wrong info. Goodwill handles true but forgivable lates.

When Should You Send a Goodwill Letter?

Timing matters. Send too soon, and it fails. Wait too long, and the mark ages out.

Best times:

- 30-60 days after the late payment. Give time for reporting, but act before it sticks.

- After 6-12 months of on-time payments. Prove you’re reliable now.

- During account anniversaries. Tie it to your loyalty.

Avoid sending if:

- You have multiple lates. Focus on one strong case.

- The account is in collections. Try pay-for-delete first.

- Less than six months clean history. Build that first.

Check your credit report first. Use AnnualCreditReport.com for free weekly pulls. Confirm the late shows up.

In 2025, with rising rates, now’s a good time. Lenders scrutinize scores more.

Step-by-Step Guide to Writing a Goodwill Letter

Writing a goodwill letter isn’t hard. Follow these steps. It takes about an hour.

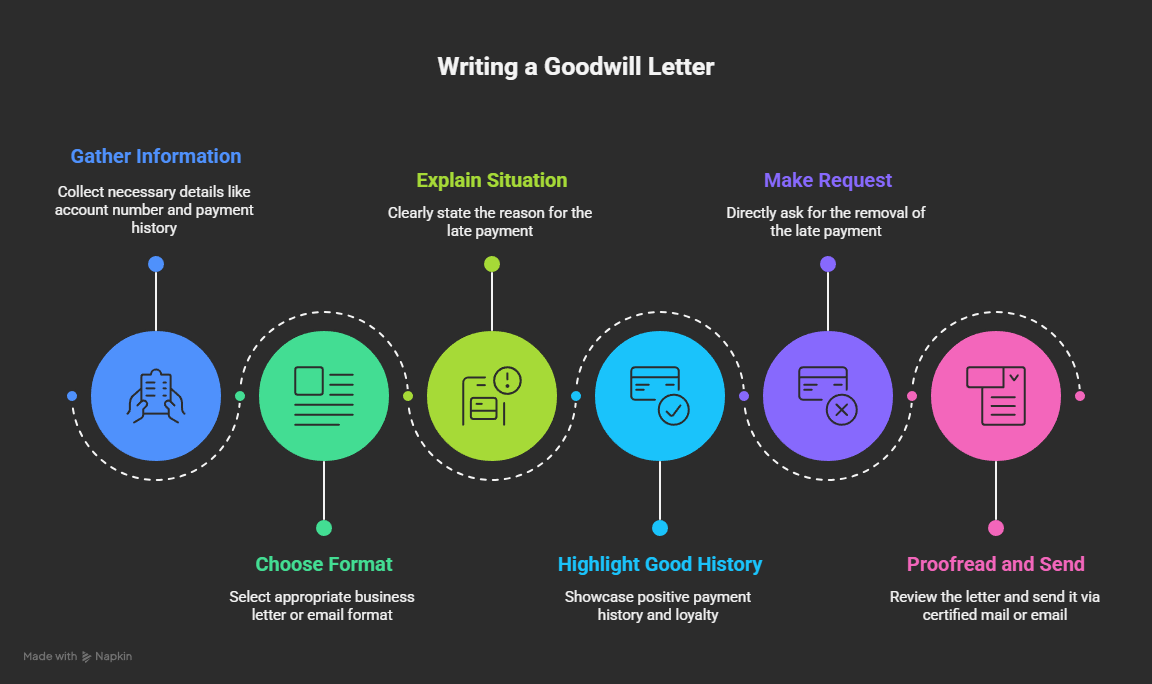

Step 1: Gather Your Information

Start with facts. Pull your credit report. Note the account number, date of late payment, and creditor address.

List your positives:

- How long you’ve been a customer.

- On-time payments count.

- Total balance paid.

Write down the reason for the late. Be honest. Job loss? Illness? Keep it brief.

Step 2: Choose the Right Format

Use business letter format. Type it. Print on white paper if mailing.

Include:

- Date.

- Creditor’s address.

- Your address.

- Salutation: “Dear [Creditor Name] Customer Service,”

Body in paragraphs. Close with “Sincerely,” and your name.

Email works too. Use the creditor’s support email. Subject: “Goodwill Request for Account [Number]”

Step 3: Explain the Situation Clearly

Own the mistake. Say, “I missed a payment on [date] due to [reason].”

Keep it short. One sentence per point.

Example: “In March 2024, I lost my job briefly. This caused the late payment on my Visa card.”

Step 4: Highlight Your Good History

Show value. “I’ve been a customer since 2020. In that time, I’ve made 48 on-time payments.”

Add loyalty. “I value our relationship and plan to continue using your services.”

Step 5: Make Your Request

Be direct. “I kindly request you remove the late payment from my credit report as a goodwill gesture.”

Don’t demand. Use “request” or “appreciate.”

Step 6: Proofread and Send

- Check spelling. Read aloud. Get a friend to review.

- Send certified mail for proof. Or use certified email.

Track it. Follow up in 30 days if no reply.

Sample Goodwill Letter Template

Use this template. Customize it with your details.

[City, State, ZIP Code]

Phone: [Phone Number]

[Creditor’s Address]

[City, State, ZIP Code]

Re: Account Number [Your Account Number] — Goodwill Adjustment Request

Dear [Creditor’s Name or “Sir/Madam”],

I am writing regarding my account with [Creditor’s Name], ending in [last four digits]. I have been a loyal customer since [start date]. During this time, I have consistently made on-time payments, totaling [number] successful transactions.

Unfortunately, on [date of late payment], I missed a payment due to [brief reason, e.g., “unexpected medical expenses following a family emergency”]. I understand the importance of timely payments and regret this oversight. It was an isolated incident, and I have since resumed my regular payment schedule without issue.

I greatly value my relationship with [Creditor’s Name] and appreciate the services you provide. As a gesture of goodwill, I kindly request that you consider removing the late payment notation from my credit report. This adjustment would more accurately reflect my overall positive payment history.

Thank you for your time and understanding. I look forward to your positive response. Please contact me at [phone] or [email] if you need more information.

Sincerely,

[Your Full Name]

Tips for Success with Your Goodwill Letter

Make your letter stand out. These tips boost chances.

- Be sincere. Creditors spot fakes.

- Personalize it. Use the rep’s name if possible.

- Attach proof. Include statements showing good history.

- Follow up politely. Call after two weeks.

- Send to the right department. Check the website for addresses.

In 2025, digital tools help. Use apps like Credit Karma to track changes post-send.

If denied, ask why. Adjust and resend in six months.

Success stories abound. One user removed a 90-day late after explaining a divorce. Score jumped 85 points.

Common Mistakes to Avoid When Writing a Goodwill Letter

Pitfalls can sink your request. Dodge these.

- Too emotional. Stick to facts. No begging.

- Blaming others. Own it fully.

- Too long. Keep under 400 words.

- Generic. Tailor to the creditor.

- Forgetting details. Include account info.

Don’t send multiples at once. Space them out.

Myth: It always works. No, but it’s worth trying.

What Happens After You Send a Goodwill Letter?

Wait 30-45 days. Check your credit report.

Possible outcomes:

- Approval. Late removed. Score rises.

- Partial. Downgraded to “paid late.”

- Denial. Letter explains why.

If approved, thank them. It builds rapport.

Monitor for 60 days. Bureaus update monthly.

Alternatives if a Goodwill Letter Doesn’t Work

Not every letter succeeds. Try these next.

- Dispute if inaccurate. Use FTC guidelines.

- Pay-for-delete with collectors. Negotiate removal for payment.

- Credit builder loans. Add positive history.

- Secured cards. Rebuild over time.

Consult a credit counselor. Non-profits like NFCC offer free help.

In severe cases, bankruptcy resets. But that’s last resort.

Conclusion

A goodwill letter can erase late payments from your credit report. It helps fix your score without much cost or hassle. Many people see results, especially if they have a solid history with the creditor.

Follow the steps in this guide. Use the template we provided. Customize it to fit your story. Send it off and stay patient. Responses take time, often 4 to 8 weeks.

Check your credit report regularly after you send it. Sites like AnnualCreditReport.com make this easy and free. Watch for updates each month.

Your financial future improves with better credit. It opens doors to lower loan rates, easier rentals, and more job options. Small steps like this add up.

Take action today. Pull your report. Draft the letter. Mail or email it. Even if it doesn’t work the first time, you can try again later.

You’ve got the tools here. Use them. Better credit is worth the effort. Keep building good habits along the way..

Frequently Asked Questions About Goodwill Letters

Can a goodwill letter remove all late payments?

A goodwill letter often works for one or two late payments if you have a good history. For more, send separate letters to each creditor. Focus on your strongest cases first. This keeps things simple and increases your odds.

How long does it take to see results?

Expect 4-8 weeks for a response. Credit reports update monthly, so the change might show up then. Check your report after 30 days. If nothing happens, follow up with the creditor.

Do banks still honor goodwill letters in 2025?

Yes, banks like Chase and Wells Fargo still consider them. Policies change with regulations, but customer courtesy holds. Success depends on your account history. Try it if you’ve been reliable overall.

Is a goodwill letter the same as a dispute letter?

No, they’re different. A dispute letter claims the info is wrong or unverified. A goodwill letter admits the late payment but asks for removal as a favor. Use disputes for errors only.

What if the creditor sold the debt?

Contact the new debt owner directly. Use the same goodwill letter process. Find their address on your credit report or their site. Explain your history and request the removal politely.