Debt Validation Letter: What It Is and How to Write One

Introduction

You get a letter or phone call saying you owe money — maybe for an old credit card, medical bill, or loan you barely remember. Panic sets in. But before you pay a dime or agree to anything, you have the right to ask one simple question:

“Can you prove I actually owe this debt?”

That’s where a Debt Validation Letter comes in.

A debt validation letter is your legal tool under the Fair Debt Collection Practices Act (FDCPA) that forces a debt collector to provide proof that the debt they’re trying to collect is valid, accurate, and legally enforceable.

In this complete guide, you’ll learn:

- What a debt validation letter is

- When and how to send one

- What to include in your letter

- How to use free templates and samples

- And what happens after you send it

Let’s protect your rights — and your wallet.

1. What Is a Debt Validation Letter?

A debt validation letter is a formal written request you send to a debt collector after they first contact you about an alleged debt.

It’s not just a formality — it’s your legal right.

Under the FDCPA (15 U.S.C. § 1692g), collectors must provide detailed proof of:

- The original creditor

- The total amount owed

- The date the debt was incurred

- Documentation that they have the right to collect it

When you request validation within 30 days of their initial contact, the collector must pause all collection activity until they verify the debt.

If they can’t verify it, they must stop contacting you altogether.

2. Why Sending a Debt Validation Letter Matters

Debt collectors handle thousands of accounts, and errors happen all the time — wrong amounts, old (expired) debts, or even debts that don’t belong to you.

Here’s why sending a validation letter is crucial:

- Protects you from paying the wrong debt

- Stops collection activity until proof is provided

- Gives you time to verify the debt’s accuracy

- Creates a written record in case of future disputes or lawsuits

- Prevents damage to your credit from unverified collections

Even if you think the debt might be yours, always verify before paying. Some debts may already be past the statute of limitations and legally uncollectible.

3. When to Send a Debt Validation Letter

Timing is everything. You have 30 days from the date you first hear from the debt collector to request validation. If you miss that window, you still can send a letter, but collectors are not legally required to stop collection activity while they respond.

If you receive a collection notice by mail, note the date on the letter and the postmark — that’s when your 30-day clock starts.

If you were contacted by phone, ask for written notice first (they’re required to send it within 5 days of their first call). Once you get that, send your debt validation letter promptly.

4. What Should Be Included in a Debt Validation Letter

Your letter doesn’t need to be complicated — it just needs to be clear, direct, and polite.

Here’s what you should include:

- Your full name and mailing address

- The date of the letter

- The name and address of the debt collector

- A statement that you’re requesting validation of the debt under the FDCPA

- A request for specific details, including:

- The amount of the alleged debt

- The name of the original creditor

- Documentation showing you agreed to the debt

- Proof the collector is authorized to collect it

- The date the debt was incurred

- A copy of any judgment (if applicable)

- A statement requesting all communication be in writing

- Your signature (optional) — some people omit it to prevent signature misuse.

5. Sample Debt Validation Letter (Template)

Below is a free debt validation letter template you can copy, customize, and send.

[Your Address]

[City, State ZIP]

Date: [Insert Date]

[Debt Collector’s Address]

[City, State ZIP]

Subject: Request for Debt Validation

Dear [Debt Collector’s Name],

I am responding to your recent communication about an alleged debt. Under the Fair Debt Collection Practices Act (FDCPA), 15 U.S.C. § 1692g, I am requesting full validation of this debt before any further collection activity.

Please provide the following information in writing:

- The name and address of the original creditor.

- The amount of the debt and a full itemized accounting of any fees or interest.

- Documentation proving I am legally obligated to pay this debt.

- Proof that your agency is licensed and authorized to collect in my state.

- A copy of any judgment, if applicable.

Until you provide this information, please cease all collection efforts, including calls, letters, or credit reporting.

Thank you for your cooperation.

[Your Name]

Tip: Send this letter via certified mail and keep a copy for your records.

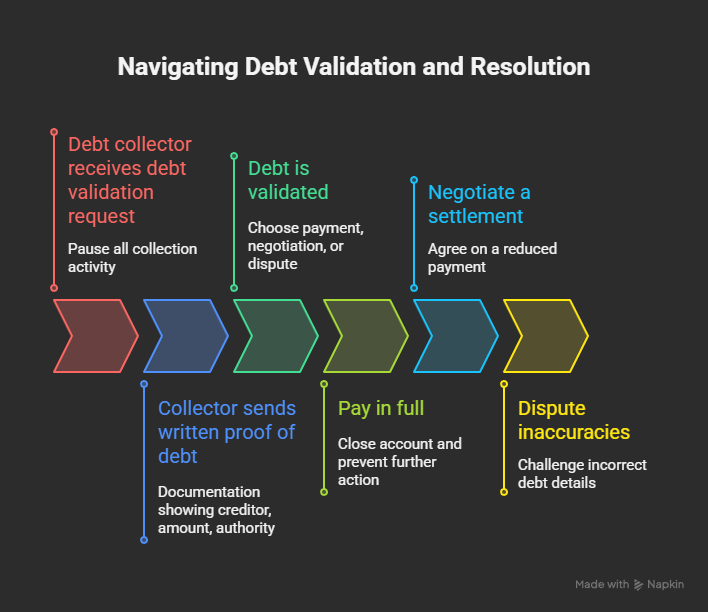

6. What Happens After You Send a Debt Validation Letter

Once the debt collector receives your request, they must pause all collection activity until they verify the debt.

That includes:

- No phone calls

- No letters

- No credit reporting

- No lawsuits

The collector must send written proof showing:

- Who the original creditor is

- How the amount was calculated

- Their legal authority to collect it

If they fail to provide proof, they are legally prohibited from continuing collection.

If they continue to contact you without validation, it’s considered a violation of the FDCPA — and you may have grounds to file a complaint with the Consumer Financial Protection Bureau (CFPB) or even sue for damages.

7. What If the Debt Is Validated?

If the collector provides legitimate documentation proving the debt is yours, you have three main options:

Option 1: Pay in Full

If you can afford to, paying the full amount immediately closes the account and prevents further interest or legal action.

Option 2: Negotiate a Settlement

You can often settle for 40–60% of the total balance. Always get any settlement agreement in writing before paying.

Option 3: Dispute Inaccuracies

If the debt details are incorrect — wrong balance, dates, or account owner — you can dispute it with the collector and the credit bureaus.

8. What If the Collector Ignores Your Letter?

If a collector fails to respond or continues contacting you illegally:

- Keep records of every letter, email, or call.

- File a complaint with the CFPB (consumerfinance.gov/complaint) or your state attorney general.

- Consult a consumer law attorney — you may be entitled to up to $1,000 in damages under the FDCPA.

Collectors who violate your rights can be held accountable — but only if you document your case.

9. Debt Validation Letter vs. Debt Verification Letter

Many people confuse these two — but they’re not the same.

- A Debt Validation Letter is sent by you (the consumer) to request proof.

- A Debt Verification Letter is what the collector sends back in response.

You must initiate the process for validation to happen.

10. Free Debt Validation Letter PDF Download

To make things easy, you can create a Debt Validation Letter PDF using any word processor. Once done, export it to PDF and print it for certified mailing.

Or use free templates from:

Make sure to keep a digital copy and the mail receipt for your records.

11. Common Mistakes to Avoid

- Ignoring calls or letters — silence doesn’t make it disappear.

- Admitting ownership of the debt in your letter.

- Sending without certified mail proof.

- Failing to check your credit reports afterward.

- Missing the 30-day deadline.

Protect yourself by keeping communication written, factual, and traceable.

12. How Long Does the Debt Validation Process Take?

Typically, once your letter is received, the collector should respond within 30 days. Some respond sooner, others never do. During that time, they cannot legally pursue collection.

If 45 days pass with no response, consider the debt unvalidated and send a follow-up notice requesting removal from your credit report.

13. How to Check if a Debt Collector Is Legitimate

Before sending any money or information, confirm the collector is real.

Check:

- Their company name and license (via your state attorney general’s office)

- Their Better Business Bureau (BBB) profile

- Whether they are registered with the CFPB

Scammers often pose as debt collectors — so verify before engaging.

14. What If the Debt Is Too Old to Collect?

Most debts expire after a certain period (called the statute of limitations), usually 3–10 years depending on your state.

Once expired, collectors can still ask for payment, but they can’t sue you to collect it.

Important: If you acknowledge or make a partial payment, it may restart the clock on the debt. Always validate first before making any payment or admission.

15. Rebuilding After a Debt Collection

Once your debts are validated, resolved, or disputed, it’s time to rebuild.

- Check your credit report to ensure the account status is accurate.

- Dispute errors with Experian, Equifax, and TransUnion.

- Start paying bills on time to rebuild payment history.

- Use rent reporting services like AxcessRent to strengthen your credit profile without loans or credit cards.

Debt validation isn’t just about protecting yourself — it’s about taking control of your financial story.

Conclusion

A debt validation letter is one of the most powerful tools consumers have to protect their rights and avoid paying debts they don’t owe.

Whether you’re dealing with an old credit card bill, a surprise medical collection, or a third-party collector you’ve never heard of — always verify before paying.

The process is simple: write, send, wait for proof, and keep records. With the right approach, you can stop harassment, prevent credit damage, and move toward financial peace.