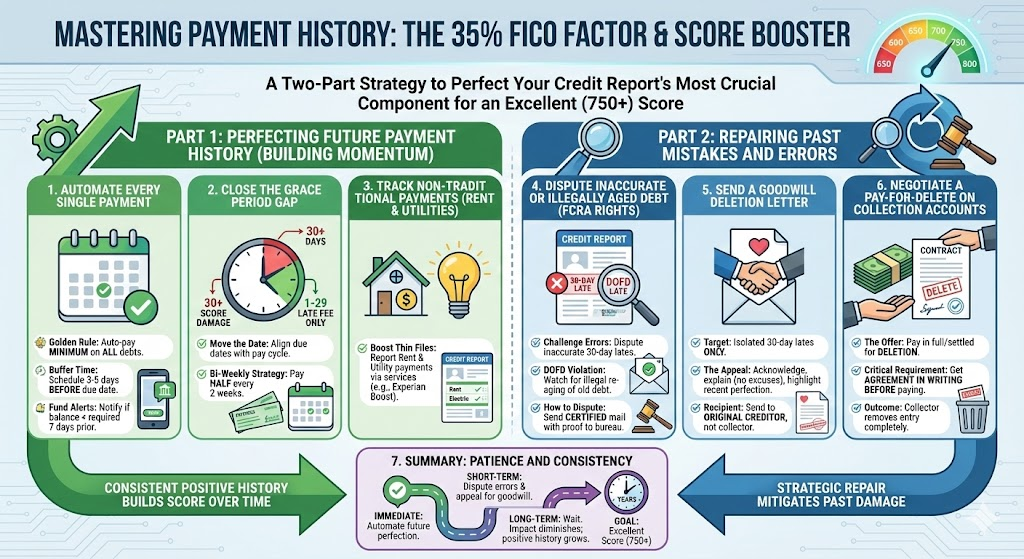

How to Fix and Improve Your Credit Payment History ?

Credit Payment history is the most important component of your FICO Score, making up a massive 35% of the total calculation. Because it acts as the primary indicator of your financial reliability, perfecting this section of your credit report is the fastest and most effective way to raise your score into the excellent range (750+).

Unfortunately, payment history is also the hardest part to change, as most negative marks stay on your report for up to seven years.

This guide provides a two-part strategy: Part 1 focuses on preventing future mistakes, and Part 2 focuses on repairing and disputing past errors.

Part 1: Perfecting Future Credit Payment History

The clock cannot be reversed, so the first step in fixing your payment history is ensuring the problem never gets worse. A future 7-year history of perfect payments is the only way to dilute the impact of an old mistake.

1. Automate Every Single Payment

The number one reason for a late payment is simply forgetting the due date or miscalculating the day a bill is processed. Remove human error entirely by setting up automatic drafts for all recurring obligations.

- The Golden Rule: Set up automatic payments for at least the minimum due amount on every debt (credit cards, installment loans, utilities, etc.).

- Buffer Time: Schedule the automatic payment to hit 3 to 5 days before the actual due date to avoid issues with bank processing times, weekends, or holidays.

- Fund the Account: Use banking alerts to notify you if the payment account balance drops below the required amount 7 days before the due date.

2. Close the Grace Period Gap

Remember that a payment is only reported as late if it is 30 or more days past the due date. If you consistently pay 5, 10, or 15 days late, you are incurring late fees but not damaging your score.

- Move the Date: Call your credit card issuer or lender and ask if they can change your due date to better align with your pay cycle (e.g., changing it from the 1st of the month to the 15th).

- The Bi-Weekly Strategy: If possible, pay half of your monthly payment every two weeks. This ensures you are always ahead of the due date and minimizes interest accumulation.

3. Track Non-Traditional Payments (Rent and Utilities)

Many major scoring models (like FICO 9 and VantageScore 3.0+) now include non-traditional accounts, like rent and utility payments, in their calculations if they are reported. A perfect history here can significantly boost a thin credit file.

- Ask Your Landlord: If you rent, ask your property manager if they report to credit bureaus (often via services like Experian Boost or RentReporters). If not, you may be able to subscribe to a service that reports your rent payments on your behalf.

- Utility Reporting: Some utility companies allow you to opt-in to have your history reported.

Part 2: Repairing Past Mistakes and Errors

While you cannot delete accurate late payments, you have strong consumer rights that allow you to challenge inaccuracies and appeal for leniency.

4. Dispute Inaccurate or Illegally Aged Debt (FCRA Rights)

The Fair Credit Reporting Act (FCRA) gives you the right to challenge any information on your report that you believe is inaccurate, incomplete, or unverifiable.

- The 30-Day Late Error: If you know you paid on time, or if a payment was only 15 days late but reported as 30 days late, dispute it immediately.

- The DOFD Violation: Check the Date of First Delinquency (DOFD). If an old debt has been illegally re-aged (i.e., the DOFD was changed to make the debt appear newer than it is), this is a federal violation.

- How to Dispute: Send a dispute letter via certified mail to the credit bureau reporting the error. Provide any documentation (canceled checks, bank statements) that proves the date is incorrect. The bureau must investigate and remove the item if the creditor cannot verify its accuracy within 30 days.

5. Send a Goodwill Deletion Letter

A goodwill letter is a formal, polite appeal to the original creditor to remove an accurate but minor late payment as an act of goodwill. This works best for isolated incidents.

- Target: Only target single 30-day late payments. Do not use this for 60-day or 90-day delinquencies, charge-offs, or collections.

- The Appeal:

- Acknowledge the mistake and take full responsibility.

- Explain the reason for the delinquency (e.g., job transition, temporary medical issue). Do not make excuses; state the facts.

- Highlight your perfect payment history since the incident (e.g., “I have made 36 consecutive on-time payments since the 30-day late in 2022”).

- Politely request the late payment to be removed from your credit file as a gesture of goodwill to reflect your true financial responsibility.

- Send to the Original Creditor: Do not send this to a debt collector or the credit bureau. It must go to the company that originally granted the credit.

6. Negotiate a Pay-for-Delete on Collection Accounts

If you have debt in collections, the collector is typically a third party. The most common way to resolve this is by negotiating a “Pay-for-Delete.”

- The Offer: You agree to pay the debt in full or settle for a reduced amount, only if the collector agrees in writing to completely remove the collection entry from your credit reports.

- Critical Requirement: Get the agreement in writing before you pay a single penny. If they refuse to provide a signed document promising deletion, do not pay, as the collection will simply update to “Paid” but remain on your report, still damaging your score.

7. Summary: Patience and Consistency

Improving your payment history is a marathon, not a sprint. The impact of a negative mark diminishes over time, and the impact of consecutive on-time payments grows over time.

- Immediate Action: Use automation to lock in future perfection.

- Short-Term Win: Dispute any inaccuracies or appeal for goodwill deletion.

- Long-Term Strategy: Wait. Every month that passes without a missed payment strengthens your position and brings you closer to the day the old negative mark finally falls off your report after 7 years.

Remember: Consistency in payment is the foundation of a high credit score, directly impacting 35% of your FICO calculation.