How to Create Your Dream Life Through Budgeting ?

Most people view the word “budget” as a financial straightjacket—a restrictive list of “no’s” that prevents them from enjoying life. But what if a budget wasn’t about limitation? What if, instead, it was the blueprint for your dream life?

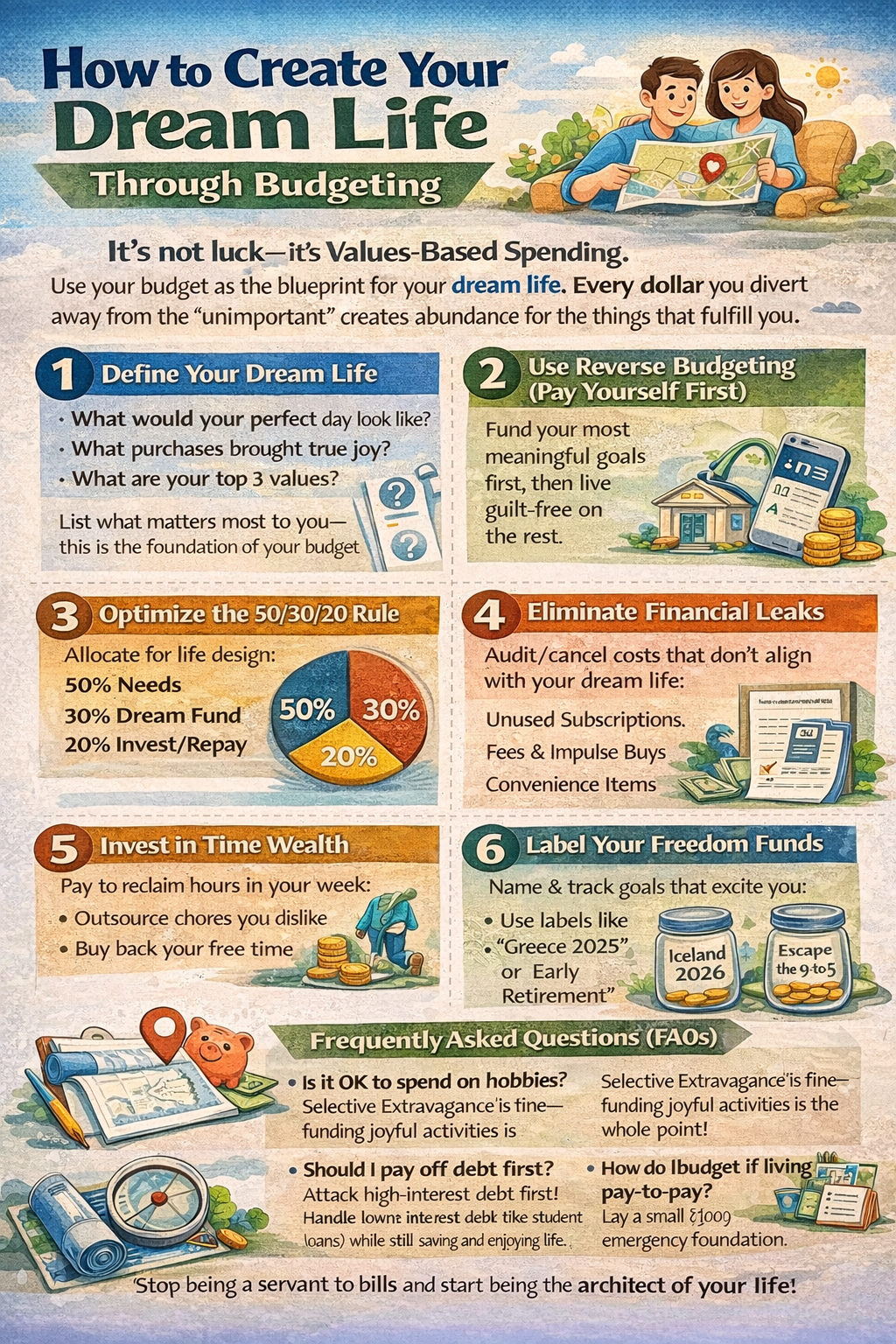

To create your dream life isn’t about winning the lottery; it’s about intentionality. It is the process of diverting every dollar away from things that don’t matter so you have an abundance of resources for the things that do. This is the essence of Values-Based Spending.

In this guide, we will explore how to stop “accidental spending” and start engineering a lifestyle that brings you genuine fulfillment.

1. The Philosophy of the “Dream Life” Budget

The traditional approach to budgeting focuses on math. The “Dream Life” approach focuses on psychology and values.

Most budgets fail because they are built on deprivation. You cut out the $6 latte, the streaming service you enjoy, and the dinners with friends. By day 15, you feel miserable, “splurge” to feel better, and abandon the budget entirely.

Values-Based Spending flips the script. Instead of asking “What can I cut?” you ask “What do I want to fund?” When you identify that travel, creative hobbies, or early retirement are your “Big Rocks,” cutting back on mindless Amazon purchases or expensive data plans doesn’t feel like a sacrifice—it feels like a strategic trade-off.

2. Step One: The Dream Life Audit

Before you touch a spreadsheet, you need to define what your dream life actually looks like. Many of us spend money trying to keep up with a version of success defined by social media or our neighbors.

Ask yourself these three questions:

- If I had no debt and a fully funded emergency fund, what would my Tuesday look like?

- Which purchases in the last six months gave me lasting joy, and which ones felt like a “sugar high” that faded instantly?

- What are my top three values? (e.g., Adventure, Security, Generosity, Learning, Health).

Write these down. Your budget should be a physical manifestation of these answers.

3. The Reverse Budgeting Method

For those who hate tracking every penny, Reverse Budgeting (also known as “Pay Yourself First”) is the most effective way to build your dream life.

How it works:

- Calculate your “Dream Goals” monthly cost: If you want a $6,000 vacation every year, your monthly cost is $500.

- Automate your savings: The moment your paycheck hits, that $500 (plus your retirement and emergency fund contributions) is moved to a separate account.

- Spend the rest guilt-free: As long as your “Dream Life” is funded and your bills are paid, the remaining balance in your checking account is yours to spend. You don’t need to track the $4 muffin because the “Big Rocks” are already taken care of.

4. Mastering the 50/30/20 Rule (with a Dream Life Twist)

The 50/30/20 rule is a classic framework, but we can optimize it for life design:

- 50% Needs: Housing, utilities, groceries, and insurance. If this exceeds 50%, you are “house poor” or “car poor,” and it is likely the primary anchor holding your dream life back.

- 30% Wants (The Dream Fund): This isn’t just “spending money.” This is where you fund your values. If you value health, this is your high-end gym membership. If you value learning, this is your book budget or Masterclass subscription.

- 20% Financial Foundation: Debt repayment and long-term investing. This is the “Security” pillar that ensures your dream life lasts forever, not just for a weekend.

5. Eliminating “Financial Leaks”

To fund the dream, you must plug the leaks. Financial leaks are recurring expenses that do not align with your core values.

- Ghost Subscriptions: Use an app or check your bank statement for services you haven’t used in 90 days.

- The Convenience Tax: Delivery fees, last-minute gas station snacks, and “convenience” grocery items can easily add up to $300+ a month. That’s a round-trip flight to a new city every single month.

- Social Spending: Are you going to expensive dinners because you enjoy them, or because you’re afraid to say “that’s not in my budget” to your friends?

6. Investing in “Time Wealth”

The ultimate dream life usually involves more time, not just more things. Once your basic budget is stable, start looking at “buying back your time.”

- If spending 4 hours on Saturday cleaning your house makes you miserable, and hiring a cleaner costs $100, can you find $100 of “leakage” to cut so you can enjoy your weekend?

- This is the transition from a “Money-First” mindset to a “Time-First” mindset.

7. The Psychology of “Deep Savings”

Saving for the sake of saving is boring. Saving for a “Freedom Fund” is exhilarating. Give your accounts names that excite you. Instead of “Savings Account,” call it “Project: Escape the 9-to-5” or “Iceland 2026.” Psychologically, it is much harder to “raid” an account when you have to look at the name of the dream you are stealing from.

Frequently Asked Questions (FAQs)

How do I budget for a dream life if I’m living paycheck to paycheck?

When you’re at break-even, your first “Dream Goal” must be Security. Your dream life cannot exist under the constant stress of a financial emergency. Focus 100% on a small $1,000 emergency fund first. Once that’s done, look for one “leak” (even if it’s just $20 a month) and start a “Dream Seed” fund. Small wins build the momentum needed for big changes.

Is it okay to spend a lot on one category if I cut others?

Yes! This is called Selective Extravagance. Famous personal finance experts call this “spending extravagantly on the things you love and cutting costs mercilessly on the things you don’t.” If you are a “foodie,” it’s okay to spend $800 a month on high-quality dining if you’re driving a 10-year-old car and living in a modest apartment.

How often should I review my budget?

Perform a “Values Check-In” once a month. Don’t just look at the numbers; look at the transactions. Ask: “Does this list of expenses look like the life I want to lead?” If you spent $400 on takeout but your value is “Health,” your budget is telling you that you’re off track.

Should I pay off debt before funding my dream life?

It’s a balance. High-interest debt (Credit cards) is a fire that will consume your dream life. Attack that first. However, if you have low-interest debt (like a student loan or mortgage), don’t wait until it’s zero to start living. Use the 20% portion of the 50/30/20 rule to handle debt while keeping the 30% “Wants” to stay motivated.

How do I get my partner on board with this vision?

Don’t start with numbers; start with the “Tuesday Morning” question. Ask your partner what their ideal day looks like. When you find common ground in your visions, the budget becomes a shared mission rather than a source of conflict. You aren’t “limiting” each other; you are “co-authoring” a future.

What is the biggest mistake people make in life-design budgeting?

The “Lifestyle Creep.” When people get a raise, they immediately upgrade their car or apartment. This keeps the “Dream Life” forever out of reach. When you get a raise, maintain your current lifestyle for six months and put the entirety of the increase toward your “Dream Fund.”

Conclusion: Your Money is a Tool, Not a Boss

A budget is not a set of rules; it is a set of choices. Every time you tap your card, you are voting for the life you want to live. By identifying your values, plugging your financial leaks, and automating your path to freedom, you stop being a servant to your bills and start being the architect of your existence.

Start today. Identify one value, find $50 of “leakage,” and move it toward your dream. Your future self will thank you.