How to Create and Maintain a Budget: A Step-by-Step Guide

Introduction

At its core, budgeting is simply the process of creating a plan to spend your money. It is an itemized summary of your expected income and expenses over a specific period. Many people view a budget as a “financial diet” that restricts freedom, but the opposite is true: a budget is a tool that gives you permission to spend on the things that actually matter to you.

Having a budget is important because it ensures you will always have enough money for the things you need and the things that are important to you. The benefits are clear: it helps you find “hidden” money for your long-term goals and allows you to manage your daily finances effectively rather than living paycheck to paycheck.

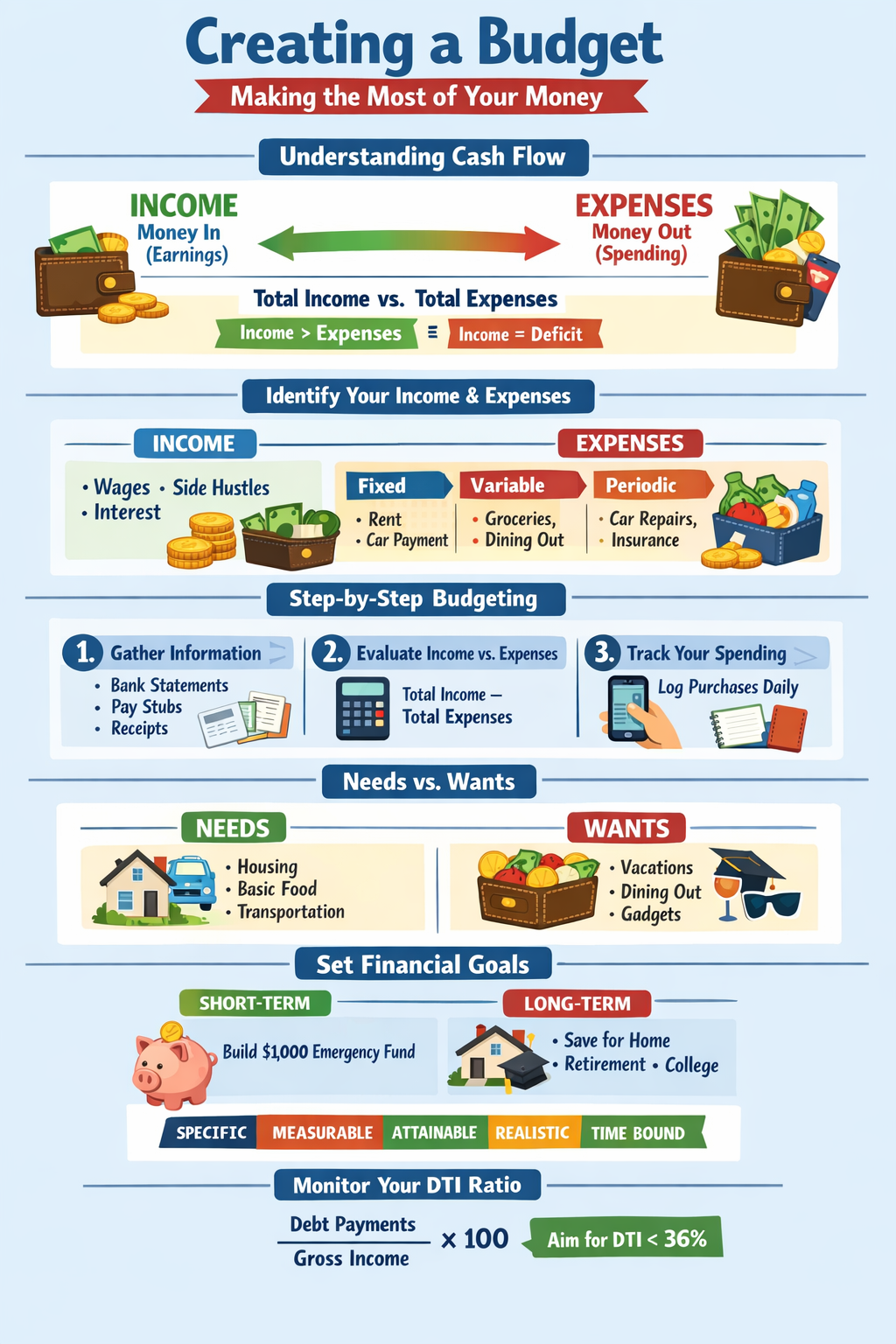

Creating a Budget – Making the Most of Your Money

Understanding Cash Flow

To master your money, you must understand your cash flow—the movement of money in and out of your pockets.

- Income: Money flowing in (earnings).

- Expenses: Money flowing out (spending). The ultimate goal of budgeting is to achieve a balance where your expenses never exceed your income.

Identify Your Income

Start by listing all money coming in. This includes employment wages, part-time “side hustles,” allowances, or interest from savings.

Critical Distinction: Net vs. Gross Income When budgeting, always use your Net Income (take-home pay). This is the amount left over after taxes, Social Security, and payroll deductions (like health insurance or 401k contributions) have been removed from your Gross Income (your total salary before deductions).

Identify Your Expenses

Not all spending is created equal. Categorize your outflows as follows:

- Fixed Expenses: These stay the same every month, such as your mortgage, rent, or car loan.

- Variable Expenses: These fluctuate based on your habits, such as groceries, dining out, or entertainment.

- Periodic/Occasional Expenses: These are the “budget busters”—things like car repairs, annual insurance premiums, or holiday gifts that don’t happen every month but must be planned for.

Step-by-Step Guide to Creating a Budget

- Step 1: Gather Information: Collect your bank statements, utility bills, pay stubs, and credit card receipts from the last 30–60 days.

- Record Everything: List every source of income and every single expense.

- Categorize: Break your spending into the fixed and variable categories mentioned above.

Evaluating Income and Expenses

Step 2: Evaluate Income vs. Expenses

Once the numbers are on paper, perform a simple calculation: Total Income – Total Expenses.

- If the result is negative: You are overspending. You must identify variable expenses to cut immediately.

- If the result is positive: You have a surplus! This money should be prioritized for savings, emergency funds, or debt repayment rather than “accidental” spending.

Review Your Budget Regularly

A budget is a living document. You should compare your actual spending against your budgeted amounts at least once a month. If you consistently overspend on groceries but underspend on entertainment, adjust your budget to reflect reality.

Step 3: Track Expenses

You cannot manage what you do not measure.

- Daily Tracking: Use a small notebook or a mobile app to record every transaction the moment it happens.

- Running Totals: Keep track of how much you have left in each category throughout the month. If your “dining out” budget is $200 and you’ve spent $150 by the second week, you know to slow down.

Determining Your Wants and Needs

Understanding Wants vs. Needs

This is the psychological heart of budgeting.

- Needs: Necessities for survival and basic functioning (housing, basic food, utilities, transportation to work).

- Wants: Non-essential items that enhance your life but aren’t required for survival (streaming services, designer clothing, luxury vacations).

Evaluating Values and Spending

Your budget should be a reflection of your personal values. If you value travel, your budget should reflect higher savings for vacations and perhaps lower spending on a car. Use the “48-hour rule” for wants: wait two days before buying a non-essential item to see if the desire fades.

Setting Financial Goals

Budgeting is easier when you are working toward something. Categorize your goals into:

- Short-term: Paying this month’s bills, building a $1,000 emergency fund.

- Long-term: Saving for a down payment, college tuition, or retirement.

Evaluating Priorities in Your Budget

Use the SMART criteria to ensure your budget supports your goals:

- Specific: “Save $50 a month” (not “save money”).

- Measurable: Use numbers to track progress.

- Attainable: Ensure your income can actually support the goal.

- Realistic: Be honest about what you can give up.

- Time-bound: Set a deadline for when you want the goal completed.

Measuring Success

Reaching Your Financial Goals

Stay motivated by celebrating small wins. When you pay off a credit card or hit your first $5,000 in savings, acknowledge the hard work. Use smaller “milestone” goals to build momentum.

Monitoring Debt-to-Income (DTI) Ratio

Monitoring your debt-to-income (DTI) ratio is an important part of maintaining a healthy budget and avoiding financial stress. The DTI ratio shows how much of your gross monthly income goes toward paying debts and is calculated by dividing your total monthly debt payments by your gross monthly income and multiplying by 100. Keeping this number in check helps ensure you are not overextended financially. As a general guideline, aiming for a DTI of 36% or less indicates good financial health and leaves room in your budget for savings, emergencies, and everyday expenses.

Suggested Monthly Spending Guidelines

If you aren’t sure where to start, use these general percentages as a baseline for your net income:

- Housing: $35

- Transportation: $20

- Debt Repayment: $15

- Other (Living Expenses): $20

- Savings & Investments: $10

Tools for Staying on Track

- Checking account register: Track your balance in real-time.

- Budget spreadsheets: Great for those who love data and customization.

- Personal finance software: Automates the tracking of your transactions.

Conclusion

Budgeting is the foundation of financial freedom. It isn’t about restriction; it’s about making better financial decisions and ensuring that your hard-earned money is working for you. By tracking your spending, distinguishing between wants and needs, and sticking to your SMART goals, you can take control of your future.

Start today. Pick up your bank statements, download a worksheet, and begin tracking your first month. Your future self will thank you.

Frequently Asked Questions About Budgeting

1. What is the most common mistake people make when starting a budget?

The most common mistake is being too restrictive or unrealistic. Many people create a “starvation budget” that cuts out all fun, which usually leads to “budget burnout” within a few weeks. A successful budget must include a category for entertainment or personal spending to be sustainable.

2. How do I handle “irregular” income if I am a freelancer or commission-based worker?

If your income fluctuates, base your budget on your lowest monthly income from the previous year. This ensures your essential needs are covered even in slow months. Any income earned above that baseline can be treated as a “bonus” and directed toward savings, debt repayment, or future goals.

3. Should I prioritize paying off debt or building an emergency fund first?

Financial experts generally recommend building a “starter” emergency fund (typically $\$1,000$ or one month of expenses) before aggressively paying down debt. This “buffer” prevents you from having to take on new debt when an unexpected expense, like a car repair, inevitably arises.

4. What is the “50/30/20 Rule” and how does it differ from the guidelines in the article?

The 50/30/20 rule is a popular alternative guideline:

- 50% for Needs (Housing, groceries, utilities).

- 30% for Wants (Dining out, hobbies).

- 20% for Financial Goals (Savings and debt repayment). It is a simplified version of the percentages in the article, designed for those who want a less granular approach.

5. How often should I update my budget?

You should track your daily spending constantly, but you only need to perform a formal budget review once a month. This allows you to look back at the previous month’s performance and adjust your categories for the upcoming month based on planned events (like birthdays or holidays).

6. What should I do if my expenses are higher than my income?

If your math results in a negative number, you have two choices: decrease expenses or increase income. Start by auditing your “Wants” and “Variable Expenses.” Canceling unused subscriptions or reducing dining out are the fastest ways to close the gap.

7. How do I budget for annual expenses like car registration or holiday gifts?

Take the total annual cost of the expense and divide it by 12. For example, if your car insurance is $600 per year, add a $50 “Sinking Fund” category to your monthly budget. By the time the bill arrives, you will have the full amount saved.

8. Is it better to use a budgeting app or a manual spreadsheet?

The best tool is the one you will actually use. Apps are convenient for automatic tracking and categorization, but manual spreadsheets or paper planners often create a stronger psychological connection to your spending, making you more mindful of where your money is going.