How Credit Scores Affect Your Mortgage Rate ? Qualify for the Best Rates in 2025

Introduction

Did you know that a 100-point difference in your credit score could save — or cost — you tens of thousands of dollars over the life of a mortgage?

Your credit score doesn’t just determine whether you get approved for a home loan; it also heavily influences the interest rate you’ll pay, the loan programs available to you, and even how much you’ll spend in monthly payments. A higher score means lower rates, more lender flexibility, and long-term financial savings.

And here’s something many buyers overlook: your rent payments can actually help you build or boost your credit score — if you use a rent reporting service. This can be a game-changer for first-time buyers who want to strengthen their credit profile before applying for a mortgage.

In this guide, we’ll break down how credit scores affect your mortgage rates, why even small improvements matter, and how rent reporting can help you take control of your financial future.

What Is a Credit Score and Why It Matters for Mortgages?

A credit score is a three-digit number (300–850) that represents your creditworthiness. Lenders rely on it to decide if you qualify for a mortgage and what interest rate you’ll receive.

The two most common scoring models are:

- FICO® Score – Used by 90% of top mortgage lenders.

- VantageScore® – A widely accepted alternative.

Your credit score directly impacts mortgage approval, interest rates, loan terms, and even the amount you can borrow:

- Approval Chances – Higher scores improve the likelihood of qualifying for a mortgage.

- Interest Rates – A strong score earns you lower rates, potentially saving you thousands over the life of the loan.

- Loan Options – Borrowers with higher scores gain access to more favorable mortgage programs.

- Monthly Payments – Lower interest rates reduce your monthly payments, making homeownership more affordable.

In short, the better your credit score, the more buying power you have and the less you’ll pay over time.

How Credit Scores Are Calculated ?

Your credit score isn’t just a random number — it’s calculated based on specific factors that reflect how you manage debt and credit over time. Lenders use these elements to predict how likely you are to repay what you borrow. Understanding what goes into your score helps you see where you’re strong and where you might improve.

- Payment History (35%) – Late payments hurt the most.

- Amounts Owed (30%) – Your credit utilization ratio.

- Length of Credit History (15%) – Older accounts strengthen your score.

- Credit Mix (10%) – Revolving (credit cards) + installment loans.

- New Credit (10%) – Recent inquiries and new accounts.

Credit Score Ranges (FICO® Model)

- Poor: 300–579

- Fair: 580–669

- Good: 670–739

- Very Good: 740–799

- Excellent: 800–850

Most lenders require a minimum 620 score for conventional mortgages, but higher scores unlock far better mortgage rates.

How Credit Scores Affect Mortgage Rates

When you apply for a mortgage, lenders don’t just look at your income or savings — your credit score plays a huge role. To them, it answers a critical question: “How risky is this borrower?”

- Lower credit scores signal higher risk, which usually means higher mortgage rates to protect the lender.

- Higher credit scores show you’re more reliable, so you’re rewarded with lower mortgage rates and better loan terms.

In short, a stronger credit score doesn’t just improve your chances of approval — it can save you tens of thousands of dollars in interest over the life of your mortgage.

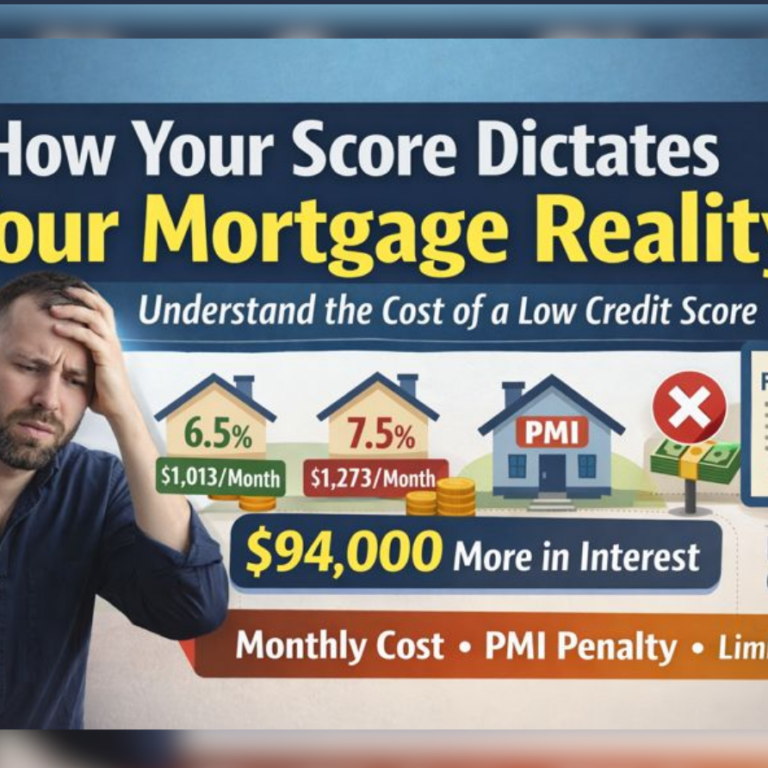

Real-World Example: Mortgage Rate Differences

For a $300,000 loan, 30-year fixed mortgage:

| Credit Score | Approx. Rate | Monthly Payment | Total Interest (30 Years) |

|---|---|---|---|

| 760–850 (Excellent) | 6.0% | $1,800 | $347,515 |

| 700–759 (Good) | 6.3% | $1,850 | $366,058 |

| 680–699 (Fair) | 6.7% | $1,935 | $396,628 |

| 620–679 (Poor) | 7.5% | $2,100 | $456,063 |

Let’s put the numbers into perspective. Imagine you’re taking out a $300,000 loan on a 30-year fixed mortgage. Your credit score directly affects the interest rate you qualify for — and the difference is massive.

- Excellent Credit (760–850): With a 6.0% rate, your monthly payment is about $1,800, and you’ll pay around $347,515 in total interest over 30 years.

- Good Credit (700–759): At 6.3%, your monthly payment increases slightly to $1,850, with $366,058 in total interest.

- Fair Credit (680–699): At 6.7%, payments climb to $1,935, and total interest jumps to $396,628.

- Poor Credit (620–679): With a 7.5% rate, monthly payments soar to $2,100, and interest over the loan’s lifetime skyrockets to $456,063.

That’s a $100,000+ difference in interest between having a score in the low 600s vs. the mid-700s — money that could have gone toward savings, investments, or even paying off your home faster.

Beyond Interest Rates

Your credit score also affects:

- Down payment requirements – Lower scores may mean larger down payments.

- PMI (Private Mortgage Insurance) – Higher scores = lower PMI costs.

- Loan program eligibility – Certain loans (like conventional) may be unavailable below a score threshold.

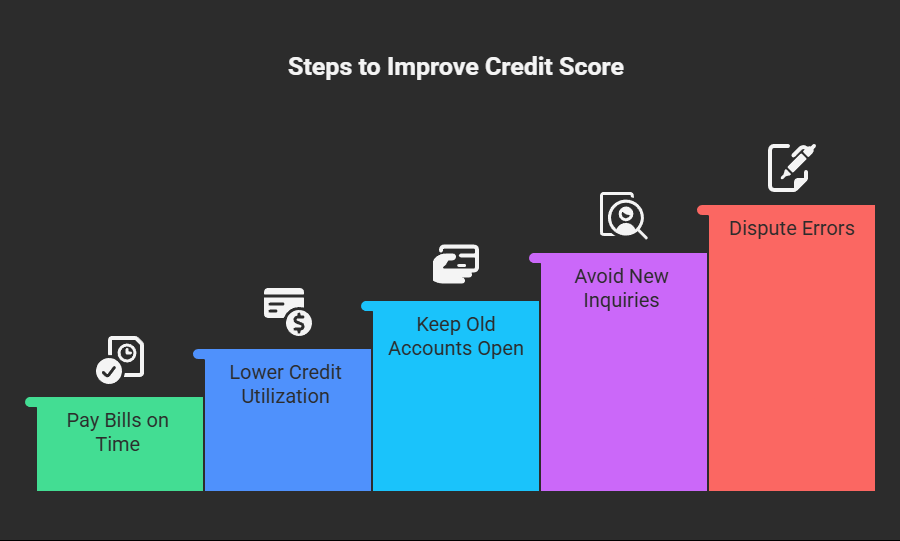

How to Improve Credit Scores Before Applying for a Mortgage

Even modest improvements in your credit score can make a big difference in the mortgage rate you qualify for—potentially saving you tens of thousands of dollars over the life of the loan. The good news? With the right habits and planning, you can boost your score before applying for a mortgage.

Key Strategies to Raise Your Score:

Pay Bills on Time – Your payment history makes up the largest portion of your credit score. Even one late payment can cause damage. Automate payments or set reminders to avoid missed due dates.

Lower Credit Utilization – This measures how much of your available credit you’re using. Keep balances below 30% of your limit—and under 10% if possible—to show lenders you can manage debt responsibly.

Keep Old Accounts Open – Closing old credit cards shortens your credit history, which can hurt your score. Even if you don’t use a card often, keeping it open helps build a longer, stronger profile.

Avoid New Inquiries – Every time you apply for new credit, a “hard inquiry” is added to your report. Too many inquiries in a short time can lower your score and signal risk to lenders. Avoid opening new accounts before mortgage shopping.

Dispute Errors – Mistakes on your credit report—like accounts that don’t belong to you or incorrect late payments—can unfairly drag your score down. Review your reports from Experian, Equifax, and TransUnion, and dispute inaccuracies.

Example: Raising your score from 660 to 700 may reduce your mortgage rate by 0.3% — saving $20,000+ over 30 years.

The Hidden Gem: Rent Reporting and Credit Building

Most people don’t realize that their rent payments can help them build credit. Traditionally, rent only shows up on your credit report if you miss a payment, which negatively impacts your score. But with rent reporting services, every on-time payment can positively contribute to your credit history—an often-overlooked strategy for first-time homebuyers or renters looking to strengthen their financial profile.

How Rent Reporting Works

- Sign Up with a Rent Reporting Service – Platforms like AxcessRent allow renters to report payments to credit bureaus.

- Verify Payments – Payments are confirmed via your landlord or bank statements to ensure accuracy.

- Payments Are Reported – Your rent history is added to one or more credit bureaus, such as Experian, Equifax, or TransUnion.

Key Benefits

- Builds Payment History – On-time payments are the most significant factor in your credit score.

- Helps Thin Credit Files – Ideal for young adults, immigrants, or anyone with limited credit history.

- Improves Credit Mix – Adds a consistent installment-like account, which strengthens your overall credit profile.

Real-Life Example

Jane, 28, starts with a 620 credit score. By using rent reporting consistently for 12 months, her score rises to 675.

Pro Tips for Future Homebuyers

- Start improving credit 12–24 months before applying.

- Use rent reporting if you’re a renter preparing for homeownership.

- Combine with other tools: secured cards, credit-builder loans.

- Work with a nonprofit credit counselor for a tailored plan.

Conclusion: Unlocking Homeownership Through Credit and Rent Reporting

Your credit score is one of the most powerful factors in determining your mortgage rate, monthly payment, and overall cost of homeownership. Even a modest improvement can save tens of thousands of dollars over the life of your loan. Understanding how your score is calculated—payment history, amounts owed, credit history length, credit mix, and new credit—is the first step toward taking control of your financial future.

Lenders use your credit score to assess risk. Higher scores mean lower interest rates, better loan terms, and more negotiating power. Real-world examples show that the difference between a 620 and a 760 score could cost over $100,000 in interest on a typical 30-year mortgage.

Fortunately, you don’t have to wait years to improve your score. Simple strategies like paying bills on time, lowering credit utilization, keeping old accounts open, and avoiding unnecessary inquiries can make a big difference.

And here’s the game-changer for renters: rent reporting. By reporting on-time rent payments through services like AxcessRent, you can build positive credit history, improve your credit mix, and boost thin credit files—often raising your score by 20–50 points in just a year. This can directly lower your mortgage rate and save thousands of dollars.

For first-time homebuyers, combining traditional credit-building strategies with rent reporting is one of the fastest ways to qualify for a better mortgage and secure your dream home. Start early, monitor your progress, and take advantage of all the tools available.

Key Takeaways:

- Your credit score directly affects your mortgage rate, loan approval, and total interest paid.

- Improving your score—even modestly—can save thousands over time.

- Rent reporting is a powerful, underutilized tool to boost credit history and lower mortgage costs.

- Consistency and strategic credit management put you in the best position to secure your ideal home.

Take control today, leverage your credit wisely, and when the time comes to apply for a mortgage, you’ll be ready to lock in the best rate possible and step confidently into homeownership.