Guide to Debt Management Options: Mastering Your Finances

Debt is rarely just a numbers game; it is an emotional and psychological weight that can paralyze even the most disciplined individuals. In a world where “buy now, pay later” is the default setting of the economy, falling into a debt trap isn’t a sign of failure—it’s a systemic inevitability for many. However, staying in that trap is a choice.

This guide moves past the surface-level advice found in brochures. We are digging into the mechanics of debt management options, the predatory nature of certain “relief” industries, and the hard-coded laws that protect your bank account from total collapse.

The Reality of Financial Distress

Financial struggle isn’t a monolith. It manifests differently depending on your investment risk tolerance, your career stage, and your geographic location. Most people recognize they are in trouble only when the phone starts ringing at 8:00 AM with a collector on the other end.

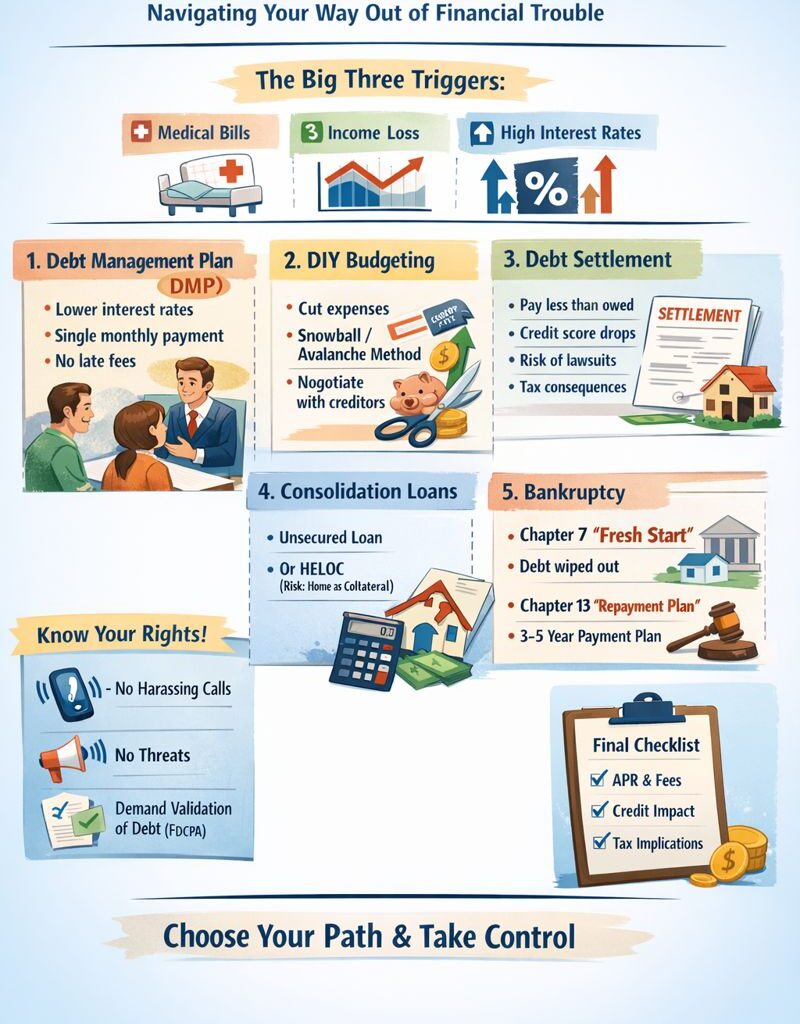

The triggers are often “The Big Three”:

- Medical Catastrophe: Even with high-tier insurance, a single week in the ICU can generate “ancillary” bills that bypass your deductible.

- Income Volatility: In the gig economy, a 20% drop in hours can lead to a 100% increase in credit card dependency.

- The Interest Rate Spiral: Carrying a balance at 29.99% APR means you aren’t just paying for your past purchases; you are paying a “tax” on your future earnings.

Before you can choose a path, you must understand where you stand. You can’t navigate a map if you don’t know your current coordinates.

Option 1: The Nonprofit Debt Management Plan (DMP)

If you are drowning in credit card debt but still have a steady income, a Debt Management Plan (DMP) is often the most logical middle ground. Unlike for-profit “consolidation” companies, nonprofit credit counseling agencies are governed by strict federal and state regulations.

How the “Bridge” Works

A DMP acts as a mediator. You stop paying the five or six different banks you owe and start making one payment to the agency. They, in turn, distribute that money to your creditors.

Why do creditors agree to this? Because they would rather receive 100% of the principal at a lower interest rate than 0% if you file for bankruptcy. Most major lenders have “pre-set” concessions for nonprofit agencies. These can include:

- Dropping interest rates from 30% to as low as 0% or 2%.

- Stopping late fees and over-limit charges.

- Re-aging: This is a crucial term. When an account is re-aged, the creditor brings it “current,” which stops the negative monthly reporting to bureaus like Equifax.

This is a powerful way to implement personal finance tips for young adults who might have overextended themselves early in their careers.

Option 2: The DIY Survivalist Strategy

You don’t always need a third party. If your debt-to-income ratio is still under 30%, you can often “muscle” your way out. This requires a shift in how you view capital.

The Budgetary Scalpel

A budget isn’t a restriction; it’s a mission statement for your money. You must separate “Survival Expenses” (Rent, Utilities, Food) from “Lifestyle Maintenance.”

- The Snowball Method: Paying off the smallest balance first for the psychological “win.”

- The Avalanche Method: Mathematically superior, focusing on the highest interest rate first.

For those curious about how these numbers scale over time, using a compound interest explained step-by-step guide can show you exactly how much your 24% APR credit card is actually costing you in lost retirement wealth.

Direct Negotiation

Believe it or not, you can call your credit card’s “Hardship Department.” If you have a clean history but are facing a temporary setback, they may offer a 6-month interest rate reduction. They won’t offer this to everyone, and they certainly won’t advertise it. You have to ask.

Option 3: Debt Settlement—The Dangerous Gamble

Debt settlement is the “bad boy” of the industry. It sounds enticing: “Pay back only 50% of what you owe!” But the fine print is written in blood.

Settlement companies usually tell you to stop paying your creditors. They want your accounts to go into “charge-off” status so the creditor feels enough pain to accept a settlement. During this period:

- Your Credit Score Dies: Expect a 100 to 200-point drop.

- You Will Be Sued: Creditors are not required to wait for a settlement. They can and will file lawsuits to garnish your wages.

- The IRS Wants Their Cut: The Internal Revenue Service (IRS) generally considers forgiven debt over $600 as taxable income. If you “save” $10,000, you might owe $2,500 in taxes the following April.

Compare this to the stability of a 401k know working limits strategy; whereas one builds wealth, the other is a desperate attempt to save a sinking ship.

Option 4: Consolidation Loans (Unsecured vs. Secured)

Consolidation is often misunderstood. It is the act of taking one new loan to pay off several old ones.

The Psychology Trap

The danger of consolidation is that it makes you feel like you’ve paid off your debt. In reality, you’ve just moved it. Many people clear their credit card balances with a consolidation loan, and then, because the cards have a $0 balance, they start spending again. Within 18 months, they have a consolidation loan plus maxed-out credit cards.

If you are considering a Home Equity Line of Credit (HELOC) to consolidate, proceed with extreme caution. You are turning unsecured debt (credit cards) into secured debt (your house). If you fail to pay a credit card, you get a bad score. If you fail to pay a HELOC, you lose your roof.

Option 5: The Legal Reset (Bankruptcy)

When the math simply doesn’t work—when your total debt exceeds 50% of your annual income—it is time to look at the U.S. Bankruptcy Code.

- Chapter 7: The “Fresh Start.” It wipes out most unsecured debts in 90 to 120 days. You must pass a “Means Test” to qualify.

- Chapter 13: The “Reorganization.” You pay back a portion of your debt over 3 to 5 years. This is the primary tool for stopping a home foreclosure.

Bankruptcy is a tool, not a tragedy. It exists in the U.S. Courts specifically to prevent a permanent “debtor’s prison” class from forming in the economy.

Protecting Yourself: The FDCPA

Regardless of which option you choose, you have rights under the Fair Debt Collection Practices Act (FDCPA).

- Collectors cannot call you at work if you tell them it’s prohibited.

- They cannot use profanity or threaten physical harm.

- They must provide a “Validation Notice” proving you actually owe the money.

If a collector violates these terms, you can actually sue them for damages. Knowing these rules is part of understanding personal finance for students and adults alike.

The Verdict: Which Path is Yours?

Choosing between these options requires an honest appraisal of your discipline and your assets.

- If you want to save your credit score: DMP or DIY.

- If you have a lump sum of cash but a ruined score: Settlement.

- If you have no assets and no hope of paying the principal: Chapter 7 Bankruptcy.

Before making a move, investigate your what is life insurance guide and other protections to ensure your family is covered while you restructure your liabilities. Debt is a season, not a destination. With the right architecture, you can build a bridge back to solvency.

Final Checklist Before You Sign Anything

- Check the APR: Is the new rate truly lower than the weighted average of your current debts?

- Verify the Fees: Does the company charge upfront? (If yes, walk away).

- Impact on Credit: Will this action stay on your report for 7 years (Bankruptcy) or show as “Paid in Full” (DMP)?

- Tax Implications: Have you set aside money for the potential 1099-C tax form?

By treating your debt management as a business transaction rather than a personal failure, you gain the tactical advantage needed to win.

Frequently Asked Questions

1. Will debt relief ruin my credit score forever?

No. While Chapter 7 bankruptcy stays on your report for 10 years and settlement can cause a significant temporary dip, these are “scars” that heal. Most people who go through a structured relief program see their scores begin to recover within 12 to 24 months as their debt-to-income ratio improves.

2. Can a debt collector take my house or car?

Only if the debt is “secured” by that asset (like a mortgage or auto loan). For unsecured debt like credit cards or medical bills, a collector must first sue you, win a judgment, and then seek a lien. It is a long process, but it is not impossible.

3. Is there a difference between debt consolidation and debt settlement?

Yes, a massive one. Consolidation involves taking a new loan to pay off old ones (ideally at a lower rate). Settlement involves stopping payments and negotiating to pay less than what you owe. One is a reorganizational tool; the other is a high-risk negotiation.

4. How do I know if a debt relief company is a scam?

The biggest red flag is any company asking for “upfront fees” before they have settled any debt or provided a service. Federal law prohibits for-profit settlement companies from collecting fees before they deliver results. If they promise to “make your debt disappear” overnight, walk away.

5. Can I handle debt relief on my own without a company?

Absolutely. You can call your creditors directly to ask for hardship programs or negotiate settlements yourself. The benefit of a company is often just their experience and “buffer” between you and the collectors, but there is no legal requirement to use one.

6. Does the government provide free debt relief?

The government does not pay off personal consumer debt. However, they regulate the industry and provide the legal framework for bankruptcy. They also fund certain HUD-approved counseling agencies that help with housing-related debt.

7. Should I use my 401k to pay off my credit cards?

Generally, this is a last resort. Your 401k is protected from creditors in a bankruptcy. If you pull the money out, you lose that protection, pay a 10% penalty (if under 59 ½), and owe income tax. You are essentially trading your future for a temporary fix. It’s better to understand 401k know working limits before touching those funds.

8. Can I still get a credit card after filing for bankruptcy or debt relief?

Yes. In fact, you will likely be flooded with offers for “secured” credit cards shortly after a bankruptcy discharge. Creditors know you can’t file for Chapter 7 again for several years, making you a “safe” bet for high-interest, low-limit cards used to rebuild credit.