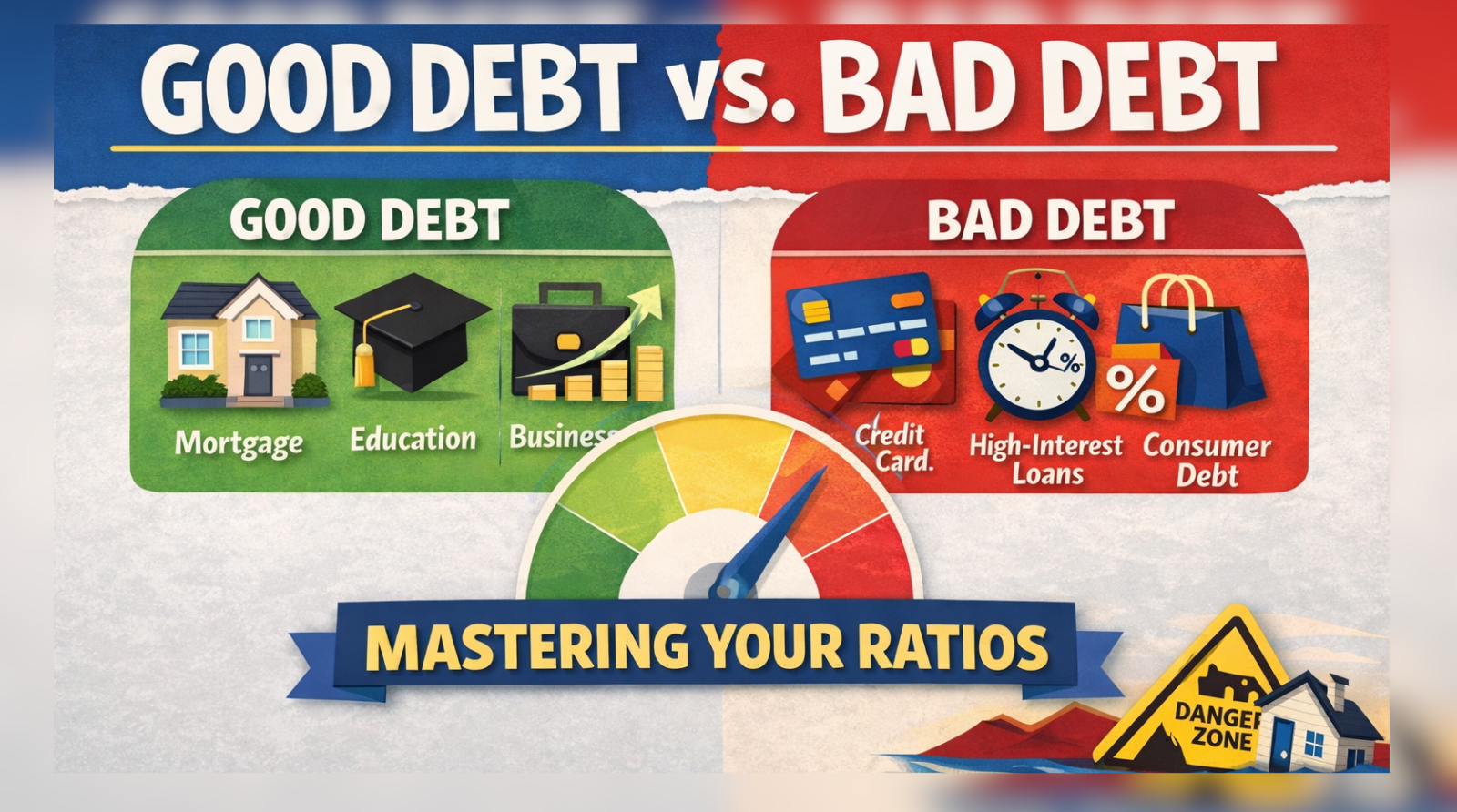

Good Debt vs. Bad Debt: Mastering the Ratios of Financial Health

Let’s be honest: the word “debt” usually feels like a four-letter word. We’ve been told since we were kids that owing money is a failure. But if you look at how the world’s wealthiest people operate, you’ll notice they aren’t debt-free—they are debt-literate.

The secret isn’t just avoiding “the red.” It’s understanding the nuance of good debt vs. bad debt and knowing exactly what is a good debt ratio for your specific stage of life.

1. The Vibe Check: Good Debt vs. Bad Debt

The quickest way to tell if you’re holding a tool or a trap? Look at where the money is going.

What is Good Debt?

Think of “good debt” as a business partner. It’s money you owe that helps you build a bigger future. It usually comes with low interest rates and high potential for a “thank you” in the form of appreciation.

- The Mortgage: It’s arguably the most common example of good debt. You’re leveraging the bank’s money to own an asset that historically goes up in value.

- Education: Taking out a loan for a high-ROI degree is an investment in yourself.

- Business Scaling: If you borrow at 7% to make a 20% profit margin, you’re winning.

The Reality of Bad Debt

On the flip side, bad debt vs. good debt is characterized by “the drain.” If the interest rate is in the double digits and the thing you bought is losing value (or was eaten for dinner last night), it’s bad debt.

- Credit Cards: The ultimate wealth-killer.

- Predatory Loans: If you’re stuck in high-interest cycles, looking into good debt consolidation loans is often the first step to breathing again.

2. The Lenders’ Secret: What’s a Good Debt to Income Ratio?

When you walk into a bank, they aren’t just looking at your smile or your salary. They are looking at your “DTI.” This is the percentage of your gross monthly pay that’s already spoken for by creditors.

What is a good debt to income ratio for mortgage approval?

If you’re house hunting, you need to know the 28/36 rule. Lenders generally want your housing costs under 28% and your total debt under 36%. If you’re pushing 43%, you might still get a loan, but the terms won’t be pretty.

Pro Tip: Keeping these numbers low early on is key. Check out these personal finance tips for young professionals to get ahead of the curve.

3. Beyond the Basics: The Pro Ratios

If you’re looking at your finances like a CFO, you need to look at what is a good debt to asset ratio and other corporate-style metrics.

- Debt to Equity (D/E): This is for the investors. Whats a good debt to equity ratio? Generally, staying between 1 and 1.5 is the sweet spot. It means you’re using leverage to grow, but you aren’t so buried that one bad month ruins you.

- Debt Service Coverage Ratio (DSCR): This is crucial for real estate investors. What is a good debt service coverage ratio? You want at least 1.25. This means for every dollar you owe, you’re making $1.25 in income. It’s your “sleep at night” buffer.

- Debt to Asset Ratio: Ideally, you want this under 0.4 (40%). If more than 60% of what you “own” is actually owned by the bank, you’re on thin ice. Understanding your investment risk tolerance can help you decide how much of this risk you’ve got the stomach for.

4. Turning the Tide

Numbers can be scary, but they are just data points. If you find your ratios are out of whack, don’t panic. Understanding how compound interest works against you in debt—but for you in savings—is the first step to flipping the script.

Your Target Cheat Sheet:

- DTI (Personal): Aim for < 36%.

- D/E (Business/Investing): Aim for 1.0.

- DSCR (Rental Property): Aim for > 1.25.

Final Thoughts

At the end of the day, debt is a choice. You can let it be a weight that holds you back, or a ladder that helps you reach the next level of your life. Keep your ratios tight, focus on “the good,” and always protect your downside. If you’re worried about the “what ifs” while building your empire, take a look at our what is life insurance guide to keep your family’s future secure.

Frequently Asked Questions

1. What is the absolute highest DTI a lender will accept?

While 36% is the gold standard, some lenders—especially for FHA loans—might go as high as 43% or even 50% in extreme cases. However, expect higher interest rates and more “hoops” to jump through if you’re at that level.

2. Is a 0% debt-to-income ratio always the best goal?

Not necessarily. While it sounds great, having zero debt often means you aren’t using credit, which can actually make your credit score stagnant. A small amount of well-managed “good debt” can actually prove to lenders that you are a reliable borrower.

3. Does my debt-to-income ratio include utilities or groceries?

Nope. DTI generally only tracks your minimum required debt payments (like credit cards, student loans, and car notes) and your housing costs. Everyday living expenses like food and Netflix don’t count toward this specific math.

4. Can I improve my debt-to-asset ratio without paying off debt?

Yes! Since it’s a ratio, you can improve it by increasing the “asset” side. If your investments grow in value or your home appreciates while your debt stays the same, your ratio improves automatically.

5. Why do investors care so much about the Debt to Equity (D/E) ratio?

Because it’s a measure of risk. A high D/E ratio means a company or individual is “highly leveraged.” If the market dips, they might not have enough of their own skin in the game to survive the crash.

6. What is the difference between front-end and back-end DTI?

Front-end DTI is just your housing costs (mortgage, tax, insurance) divided by income. Back-end DTI is everything—housing plus all other debts. Lenders look at both, but the back-end is the one that usually carries more weight.

7. Is a car loan considered good or bad debt?

It’s a gray area. Since cars lose value (depreciate), it’s technically bad debt. However, if a reliable car is what allows you to get to a high-paying job, it’s a “necessary evil” that acts like a tool. Just don’t overspend on the “luxury” side of it.

8. How often should I calculate my personal debt ratios?

Doing a “financial physical” once a quarter is a great habit. It helps you catch “lifestyle creep” before it turns into a mountain of debt that’s hard to climb over.

9. Does my spouse’s debt affect my debt-to-income ratio?

If you are applying for a loan together (like a joint mortgage), yes. The lender will combine your incomes and both of your debt obligations to find the joint DTI.

10. What is a “danger zone” for a Debt to Asset ratio?

If your ratio is above 0.6 (60%), you’re in the danger zone. This means you owe more than half of everything you own. At this stage, a single financial emergency could potentially lead to insolvency.