FICO Score vs Credit Score: Understanding the Difference

If you have ever applied for a mortgage, taken out a car loan, or even rented an apartment, you have likely been told that your decision hinges on your credit score. Yet, when you check your credit through your bank or a monitoring service, you are often presented with a number labeled FICO Score. This introduces a fundamental question: Are they the same thing?

The simple answer is that the relationship between a FICO Score and a generic credit score is similar to the relationship between Kleenex and facial tissue. A FICO Score is simply one specific, proprietary brand of credit score.

Understanding this distinction is crucial because it explains why the number you see when you check your credit might be different from the number a lender sees, impacting the interest rate you are offered on major purchases.

The Credit Score Ecosystem: A Generic Definition

To understand FICO, we must first define the generic term: Credit Score.

A credit score is a three-digit number, usually ranging from 300 to 850, that acts as a snapshot of your credit risk at a specific moment in time. Its sole purpose is to help lenders quickly determine the probability of you defaulting on a debt obligation in the next 24 months.

Credit scores are calculated by applying complex mathematical formulas (known as scoring models) to the data contained in your credit report. This data is held by the three major U.S. consumer credit reporting agencies (CRAs):

Since each of these three bureaus collects data independently from various creditors, your credit report—and therefore your credit score—will be slightly different at each bureau. The score itself is merely the output of the scoring model processing that unique report data.

The Dominant Brand: What is the FICO Score?

FICO stands for Fair Isaac Corporation, the company that pioneered credit scoring technology in the late 1950s. FICO scores were first widely used in the 1980s and have since become the industry standard.

The reason FICO holds such prominence is simple: it is estimated that 90% of all major lending decisions in the United States—including nearly all mortgages, car loans, and credit card approvals—are based on a version of the FICO Score.

The Five Key FICO Factors

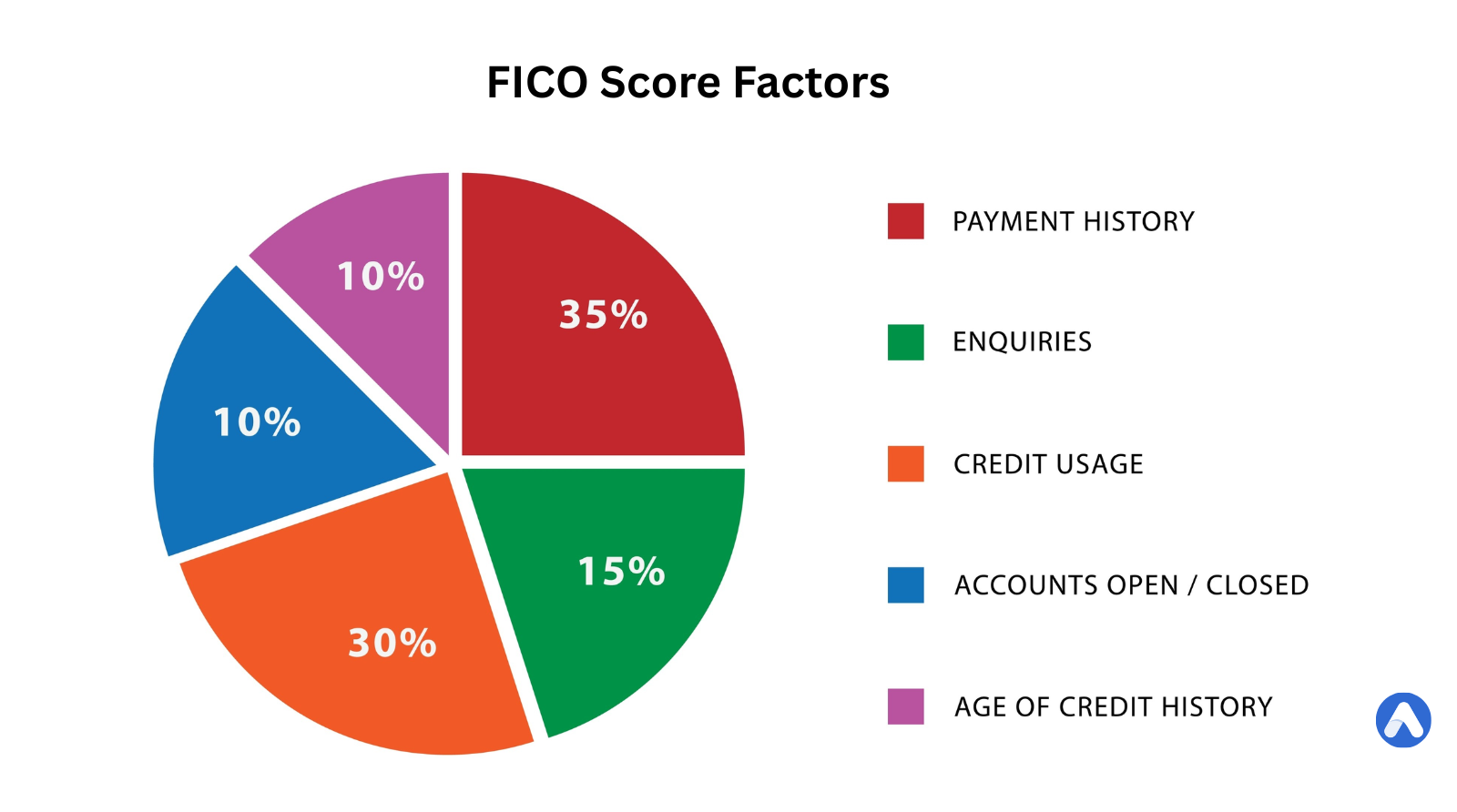

The FICO scoring model, regardless of which specific version is used, is built upon five core categories. These categories are weighted to reflect their importance in predicting future credit risk.

| FICO Factor | Weight (%) | Description |

|---|---|---|

| Payment History | 35% | Have you paid your past debts on time? The most critical factor. |

| Amounts Owed (Utilization) | 30% | How much of your available credit limit are you using? Keeping this ratio below 30% is crucial, but under 10% is optimal. |

| Length of Credit History | 15% | How long have you been managing credit? This includes the age of your oldest account and the average age of all your accounts. |

| New Credit | 10% | How many new accounts have you opened recently? Too many hard inquiries or new accounts signal high risk. |

| Credit Mix | 10% | Do you have a healthy mix of revolving debt (credit cards) and installment debt (mortgages, car loans)? |

The FICO Version Problem

To make matters more confusing, FICO is not a single number. It is an evolving series of models, often specialized by industry:

- FICO Score 8: Currently the most commonly used, general-purpose score.

- FICO Score 9: A slightly newer model that gives less negative weight to paid collection accounts.

- FICO Score 10 T: The newest version, which incorporates trended data (how balances change over 24+ months) for more predictive accuracy.

- FICO Industry-Specific Scores: These include FICO Auto Scores (used for car loans) and FICO Bankcard Scores (used for credit card approvals), which adjust the weighting to emphasize factors relevant to that specific type of lending.

The Contender: VantageScore

VantageScore is the second most common scoring model, developed in 2006 as a joint venture between the three major credit bureaus (Equifax, Experian, and TransUnion). The goal was to create a strong competitor to the long-standing FICO model, providing a single, consistent scoring approach across all three bureaus.

VantageScore is often the score you receive when you check your credit through free monitoring apps or many personal finance websites. It also ranges from 300 to 850.

Key Differences in VantageScore Factors

While the components are similar, VantageScore uses slightly different factor names and weightings than FICO, making it more flexible for consumers with shorter credit histories.

| VantageScore Factor | Weight (Relative) | FICO Equivalent |

|---|---|---|

| Payment History | Extremely Influential | Payment History (35%) |

| Age and Type of Credit | Highly Influential | Length of History / Credit Mix (25%) |

| Credit Utilization | Highly Influential | Amounts Owed (30%) |

| Total Balances/Debt | Moderately Influential | (Included in Utilization) |

| Recent Credit Behavior | Less Influential | New Credit (10%) |

Key VantageScore Advantage: It is easier for thin-file consumers (those with little history) to get a score. FICO often requires an account to be at least six months old and activity within the last six months, whereas VantageScore can often score a consumer with less history.

Why Do You See Different Credit Scores?

The main source of confusion for consumers is checking their “credit score” and seeing a completely different number than what their lender reports. This happens for three primary reasons:

1. Different Scoring Models

If you check your credit on a free app, you might see a VantageScore 4.0. When you apply for a mortgage, the lender pulls a FICO Score 8. Since these are two separate mathematical formulas with different weightings, they will produce two different numbers, even if they use the exact same credit report data.

2. Different Credit Bureaus

As mentioned, the three credit bureaus (Equifax, Experian, and TransUnion) do not talk to each other. Your credit card company might report your payment to Experian on the 5th of the month and to TransUnion on the 10th. This difference in reporting schedules, combined with the slightly varied information in your file, ensures that you almost always have three distinct FICO scores and three distinct VantageScores.

3. Industry-Specific Scores

Lenders often use specialized versions of the FICO score. For example, a credit card company might use a FICO Bankcard Score 2, which puts higher emphasis on credit card utilization. This number might be significantly different from the FICO Score 8 your bank shows you in your online portal.

Frequently Asked Questions (FAQ)

Which score is the most important?

The FICO Score 8 is generally the most important and most widely used score for general lending decisions, including auto loans and credit cards. However, if you are applying for a mortgage, lenders typically pull three FICO scores (one from each bureau) using older models like FICO 2, 4, or 5.

What is a “good” FICO score?

While the exact definition varies by lender, credit scores generally fall into these tiers:

- Exceptional: 800+

- Very Good: 740 – 799

- Good: 670 – 739

- Fair: 580 – 669

- Poor: Below 580

A score of 740 or higher is typically needed to secure the absolute best interest rates.

How often should I check my credit score?

You should check your credit scores (FICO or VantageScore) monthly to monitor for changes, especially utilization, and to catch any signs of identity theft quickly. You are entitled to a free copy of your credit report from each of the three bureaus once every 12 months via AnnualCreditReport.com.

Do “soft inquiries” affect my FICO score?

No. A soft inquiry (like checking your own score, or a credit card company pre-approving you) does not affect your FICO score. Only “hard inquiries,” which occur when you formally apply for new credit, can slightly lower your score for a few months.

Summary: Focus on the Fundamentals

Ultimately, whether your score is FICO or VantageScore, the actions required to improve it are the same. A higher score in one model almost always translates to a higher score in the other.

The most effective strategy to improve your credit is to focus on the top two weighted factors:

- Pay on time, every time (35% FICO / Extremely Influential VantageScore): Never miss a payment date.

- Keep credit utilization low (30% FICO / Highly Influential VantageScore): Try to use less than 10% of your available credit limits.

By concentrating on these core behaviors, the specific brand or version of the score the lender uses will be high enough to qualify you for the best interest rates available.