How Your Score Dictates Your Mortgage Reality in 2026 ?

Walking into a bank to secure a home loan feels like a high-stakes interview. You’ve saved the down payment, scouted the neighborhoods, and picked the perfect kitchen layout. But beneath the surface, a invisible three-digit number is doing all the heavy lifting. Your credit score isn’t just a grade; it’s a financial gatekeeper that dictates exactly how much of your hard-earned wealth will vanish into interest payments over the next thirty years.

When people ask, “how does credit score affect mortgage rates,” they often think in terms of small increments. In reality, the difference between a “good” and “excellent” score is often the cost of a luxury car in interest savings. Let’s pull back the curtain on what credit score for best mortgage rates is actually necessary to win the home-buying game.

The Bank’s Secret Playbook: Risk-Based Pricing

Lenders aren’t just giving you money; they are betting on you. Every time a loan officer pulls your file, they are calculating the statistical probability that you might stop paying. This is called risk-based pricing. The lower your score, the higher the “insurance” the bank charges in the form of interest to protect their investment.

If you are wondering what credit score gets the best mortgage rates, the target is shifting. While 720 used to be the golden ticket, today’s tightened economy means lenders are reserving their premier “platinum” pricing for those who cross the 760 threshold.

To understand the lender’s mindset deeper, explore our deep dive on How Lenders Evaluate Risk.

The Tiered Reality: What Credit Score for Best Mortgage Rates?

Lending isn’t a sliding scale; it’s a series of steps. Moving from a 679 to a 680 might seem like a single point, but it can jump you into an entirely different pricing bracket.

The Pricing Brackets

- 760 – 850: You are the “Perfect Borrower.” You get the lowest advertised rates and the least amount of paperwork hassle.

- 700 – 759: A solid position. You’ll qualify easily, but expect a slight “bump” in interest—perhaps 0.25% higher than the top tier.

- 660 – 699: This is the middle ground. You’ll likely face “Loan-Level Price Adjustments” (LLPAs), which are extra fees that make your loan more expensive.

- 620 – 659: The minimum for conventional lending. You’re in the door, but the high interest rates here can feel like a heavy weight.

If you’re just starting to build your profile, check out our Introduction to Credit Scores: A Comprehensive Guide.

How Does Credit Score Affect Mortgage Rates?

The impact of your credit score hits your wallet in three specific, painful ways:

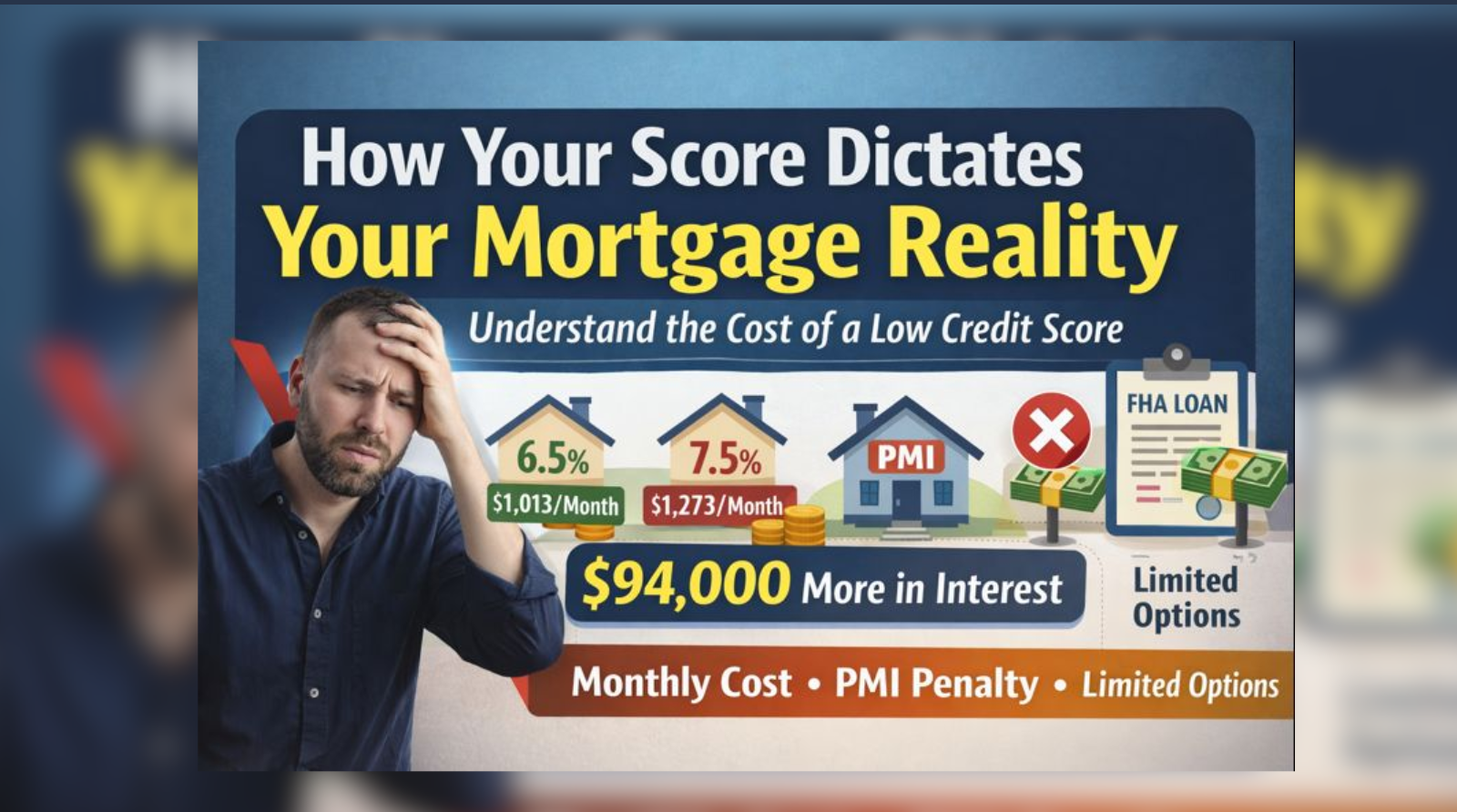

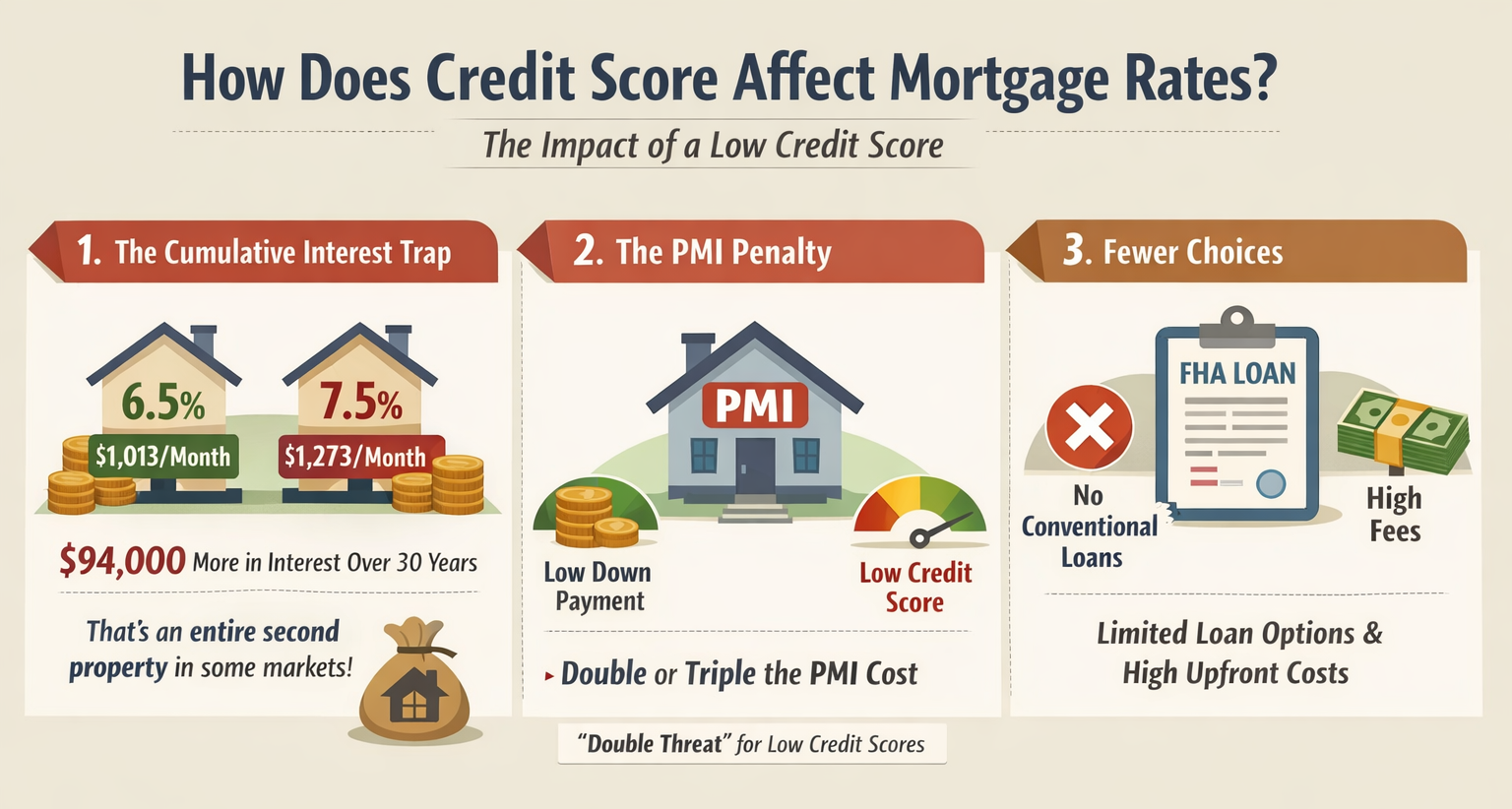

1. The Cumulative Interest Trap

On a $400,000 mortgage, the difference between a 6.5% rate and a 7.5% rate is roughly $260 a month. Over 30 years, that is nearly $94,000. You could buy an entire second property for that amount in some markets. This is why understanding Amortization: A Comprehensive Guide is so vital—it shows you how interest is front-loaded.

2. The PMI Penalty

If your down payment is under 20%, you’re stuck with Private Mortgage Insurance. Lenders see a low score and a low down payment as a “double threat.” Consequently, your PMI premiums can be double or triple what a high-score borrower pays.

3. Fewer Choices

A low score traps you in specific loan products. You might be forced into an FHA loan with high upfront fees because conventional options are off the table. This is often complicated by other factors, such as whether Does Student Loan Debt Affect Your Credit Score? in your specific case.

What Credit Score to Get Best Mortgage Rates?

If you are months away from buying, you have time to perform “financial surgery” on your score.

Kill the Utilization

Thirty percent of your FICO score is based on how much of your available credit you actually use. If your cards are maxed out, your score is suffocating. Bringing those balances down below 10% is like giving your score a shot of adrenaline. Learn more in our guide: Mastering Credit Card Utilization: A Comprehensive Guide.

The Error Hunt

Credit reports are notoriously messy. Inaccuracies regarding old debts or late payments can drag you down. If you have Found an Error on Your Credit Report, you must fight it immediately.

Leverage Your Rent

For years, rent was a “invisible” payment. No longer. By reporting your rent, you can add positive history to your file almost overnight. See How Reporting Rent Can Boost Your Credit Score for the step-by-step process.

FAQ: Your Mortgage and Credit Questions Answered

1. Is 720 a good enough credit score for the best mortgage rates?

It’s “good,” but it isn’t the best. Most lenders reserved their absolute lowest rates for scores of 760 and above. At 720, you’ll get a great loan, but you might pay slightly more than the “platinum” tier.

2. Can I get a mortgage with a 500 credit score?

It is extremely rare. While some government-backed programs technically allow it, almost all individual banks have “overlays” that require at least a 580 or 620 to actually approve the application.

3. Does a “Hard Inquiry” from a mortgage lender hurt my score?

Yes, but only slightly (usually around 5 points). The good news is that FICO realizes you need to shop around, so all mortgage-related inquiries within a 45-day window are bundled together as one single event. Read more on Everything About Hard Enquiries.

4. How does debt-to-income (DTI) relate to my credit score?

Think of credit score as your “reputation” and DTI as your “capacity.” You need a good reputation to get the rate, but you need the capacity (low debt) to actually get the loan amount you want. Check your Rent-to-Income Ratio to see how you look to a bank.

5. Why is my “Mortgage Score” different from the score on my banking app?

Your app likely uses VantageScore, which is a modern model. Mortgage lenders still use older versions of FICO (like FICO 2 or 4) because they are proven to predict long-term mortgage behavior. These models prioritize things like Length of Credit History differently.

6. Will a high down payment cancel out a bad credit score?

No. A big down payment makes it easier to get approved, but it rarely changes the interest rate. The rate is almost entirely tied to the score.

7. Should I close my old credit cards before applying for a mortgage?

Absolutely not. Closing an old account shortens your credit history and reduces your total available credit, both of which will likely tank your score right when you need it most.

8. How much will my mortgage rate drop if my score goes up 20 points?

If those 20 points push you from one tier to the next (e.g., from 675 to 695), you could see your rate drop by as much as 0.5%, which is a massive win.

9. Do medical bills on my credit report affect my mortgage rate?

Paid medical collections or those under $500 are typically ignored now. However, massive, unpaid medical debts still count against your score and can push your interest rate higher.

10. What is the fastest way to boost my score for a mortgage?

Pay down your revolving credit card balances. It is the only factor you can change in 30 days that has a massive, immediate impact on your points.

Final Thoughts: Ownership Starts with Credit

When you realize how does credit score affect mortgage rates, you stop looking at credit as a chore and start seeing it as an investment. Your score determines your lifestyle for the next three decades. By taking the time to polish your profile now, you aren’t just buying a house—you are buying your financial freedom. To see how broader market trends might affect your timing, keep an eye on the Federal Reserve’s Monetary Policy.