Debt Settlement: Complete Guide, Costs & Risks

Debt is more than just a financial metric; it is a psychological weight that affects every facet of daily life. When your monthly obligations exceed your take-home pay, or when high interest rates make it impossible to touch the principal balance, you need a radical exit strategy. Debt settlement is that strategy—a high-stakes negotiation that allows you to pay back a fraction of what you owe.

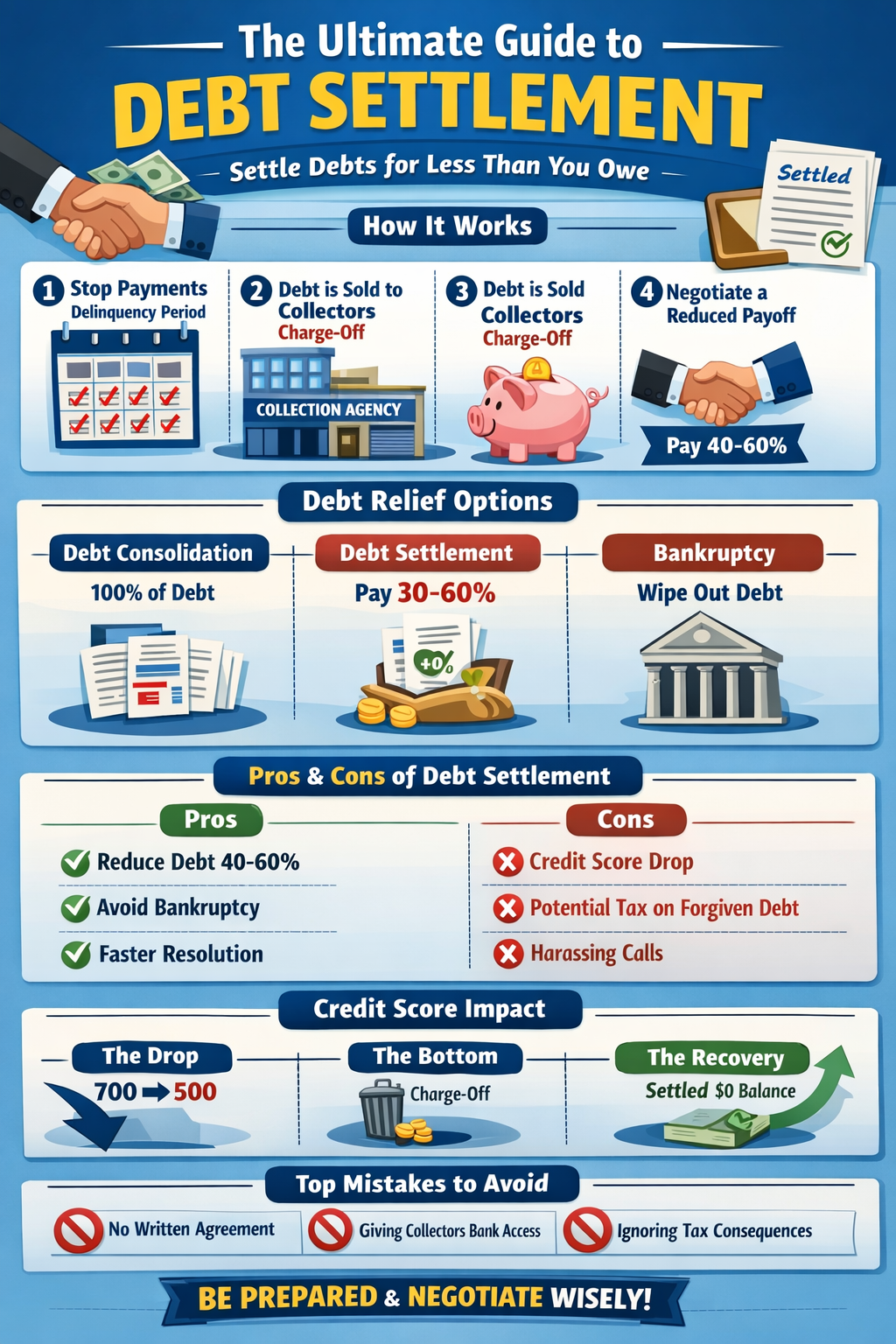

This guide provides a roadmap for navigating the complexities of debt settlement, from the first missed payment to the final credit repair steps.

What Is Debt Settlement?

Debt settlement is a formal agreement between a debtor and a creditor to satisfy a debt for a lump-sum payment that is less than the total balance owed. In this arrangement, the creditor agrees to “forgive” or “cancel” the remaining portion of the debt, marking the account as “Settled” or “Paid in Full for Less Than the Original Amount.”

How Debt Settlement Works in Real Life

In the real world, debt settlement is rarely a polite conversation held over a first-time phone call. It is a process born out of necessity. Creditors are in the business of making money through interest. They only agree to settle when they believe the alternative is getting zero dollars through a bankruptcy filing or a complete disappearance of the debtor.

Usually, this process involves a “delinquency period” where you intentionally stop paying the creditor to prove financial hardship. This creates the leverage needed for negotiation.

Debt Settlement vs. Debt Consolidation vs. Bankruptcy

Understanding the “Debt Relief Spectrum” is vital before choosing your path:

- Debt Consolidation: Best for those with good credit who want to simplify payments. You take a new loan to pay off old ones. You still owe 100% of the debt, plus interest.

- Debt Management Plans (DMP): Usually offered by non-profit credit counseling agencies. They lower your interest rates but you still pay 100% of the principal. Explore our guide to debt management options for more.

- Debt Settlement: You pay 30%–60% of the debt. It saves the most money but causes significant credit damage.

- Chapter 7 Bankruptcy: A legal liquidation. It wipes out most unsecured debt in 4–6 months but remains on your credit report for 10 years and involves federal court.

How Does Debt Settlement Work?

The mechanics of debt settlement are counter-intuitive. To fix your finances, you must first allow them to appear broken.

Step 1: The Delinquency Phase

Creditors will not negotiate with someone who is current on their payments. To them, if you are paying on time, the system is working. Most successful negotiations begin once an account is 90 to 180 days past due. During this time, your credit score will plummet, and you will receive aggressive collection calls.

Step 2: The Charge-Off and Collections

After approximately 6 months of non-payment, the original creditor (like Chase or Amex) will “charge off” the debt. This doesn’t mean the debt is gone; it means they have moved it from their “assets” to their “losses” for tax purposes. They then sell the debt to a third-party collection agency for pennies on the dollar. This is your primary window of opportunity. It is important to understand how an investor makes money off debt to understand why they settle.

Step 3: Accumulating the “Settlement Fund”

While you aren’t paying your creditors, you must be aggressively saving that money into a dedicated account. You cannot negotiate without a “carrot” to dangle. Most collectors won’t even look at an offer unless you have at least 25% of the balance ready to wire immediately.

Step 4: The Negotiation Dance

You contact the collector and present a hardship story. You offer a low percentage (20%). They counter with a high percentage (70%). You eventually meet in the middle, typically between 40% and 50%.

Timeline Expectations

- Months 1-6: Missed payments, late fees, and aggressive calls.

- Months 6-12: Debt is sold to collectors; initial low-ball offers are made.

- Months 12-36: Most settlements are finalized as the “Settlement Fund” grows large enough to cover the remaining accounts.

Is Debt Settlement a Good Idea?

Debt settlement is a “controlled burn.” It destroys the landscape of your credit to prevent the “wildfire” of total financial ruin.

When It Makes Sense

- You have a legitimate, documentable hardship (medical crisis, divorce, permanent job loss).

- You are “judgment proof” (you have no significant assets for a creditor to seize if they sue you).

- You have access to a lump sum (inheritance, 401k loan, or tax refund).

Who Should Avoid It

- People with “High-Value” Credit: If you have a 750 score and just want to save a few bucks, don’t do this. You will spend years trying to get back to that score.

- Active Military: Debt issues can affect security clearances.

- People planning to buy a home in 12 months: You should first ask am I ready to buy a house before damaging your credit.

Quick Pros vs. Cons Table

| Pros | Cons |

|---|---|

| Reduce total debt by 40-60% | Massive credit score drop (100+ points) |

| Faster than traditional repayment | Risk of being sued by creditors |

| Avoids the “public record” of bankruptcy | Forgiven debt is often taxable income |

| Stops the cycle of minimum payments | Daily harassment from collectors |

Is Debt Settlement Worth It?

To determine the “worth,” we must perform a cold, hard mathematical analysis.

The Savings Breakdown

Imagine you owe $20,000 on a credit card with a 24% APR.

- Minimum Payments: You pay roughly $500/month. It will take you over 20 years to pay it off, and you will pay over $30,000 in interest alone.

- Settlement: You stop paying for 8 months. You save $400/month. You offer $8,000 to settle. The creditor accepts.

- Result: You saved $12,000 in principal and thousands in future interest. Even after paying taxes on the forgiven debt (roughly $2,000) and a potential lawyer fee, you are ahead by over $10,000.

The Realistic Expectations

You must be prepared for the “dark period.” Between the time you stop paying and the time you settle, your phone will ring 10-20 times a day. You may receive “Summons and Complaint” notices. If you can handle the stress, the financial “worth” is undeniable.

How to Negotiate Debt Settlement on Your Own

You do not need a middleman. Many people fall into common investing mistakes when they pay high fees to companies for things they can do themselves.

Before You Negotiate

- Analyze Your Leverage: If you own a house with equity, you have low leverage (they can sue you and put a lien on the house). If you rent and have an empty bank account, you have high leverage.

- The “Hardship Letter”: Draft a concise explanation of why you can’t pay. Keep it focused on facts: “My hours were cut,” or “I have $50,000 in medical debt.”

How to Contact Creditors

Wait for them to call you, or call the “Loss Mitigation” department. Never talk to the first-level customer service agent; they don’t have the authority to settle. Ask for a manager or a “Settlement Officer.”

Sample Debt Settlement Script

The Opening: “I am calling to discuss account #XXXX. I am currently insolvent and am reviewing my options with a bankruptcy attorney. However, I have a small amount of cash from a family member and I’d like to see if we can resolve this today.”

The Offer: “I can offer a one-time payment of $1,200 to settle this $4,000 balance in full. This is all the cash I have available for this account.”

The Counter-Counter: “I understand you want 70%, but that is mathematically impossible for me. If we can’t get closer to 30%, I will have to move this account to the bottom of my priority list and focus on the creditors who are willing to work with me.”

How to Negotiate Credit Card Debt Settlement Yourself

Credit card debt companies use “internal scoring” to decide when to settle.

- The “Magic Number” Days: 120 days and 170 days are often when the biggest discounts are offered before the debt is moved to an outside agency.

- Active Accounts: You cannot settle an account and keep the card. The account will be closed immediately.

- The Written Agreement: This is the most important step. NEVER pay until you have a PDF or letter that says: “This payment of $X satisfies the debt in full and the creditor waives all further claims.”

How Much Does a Debt Settlement Lawyer Cost?

Lawyers bring a “shield” to the fight. When a lawyer represents you, collectors are legally barred from calling you directly (under the FDCPA).

Fee Structures

- Flat Fee: Often $500–$1,500 per account.

- Contingency: 15%–25% of the money saved. This is usually the best option as the lawyer only gets paid if they perform.

- Retainer: A monthly fee (e.g., $200/month) to keep them on call for legal defense if you get sued.

How Long After Debt Settlement Can I Buy a House?

Lawyers bring a “shield” to the fight. When an attorney represents you, collectors are legally barred from calling you directly under the Fair Debt Collection Practices Act (FDCPA).

- FHA and VA Loans: These are the most lenient. You can often qualify 12–24 months after the last settlement is paid, provided you have no new late payments.

- Conventional Loans: Usually require a 620 score. Most people hit this mark 24 months after settlement.

- The “DTI” Factor: Settlement helps your rent-to-income ratio by removing monthly obligations.

Debt Settlement Impact on Credit Score

Your score will take a “V-shaped” journey.

- The Drop: As you stop paying, your score will fall from the 600s/700s into the 400s or low 500s.

- The Bottom: This occurs when the debt is charged off.

- The Recovery: As soon as an account is marked “Settled,” your mastering credit card utilization improves because the balance goes to $0.

Common Debt Settlement Mistakes to Avoid

- The “Tax Trap”: If you settle a debt for $5,000 less than you owe, the IRS sees that $5,000 as income. You will get a 1099-C. Pro Tip: Look into IRS Form 982 (Insolvency). If your total liabilities exceeded your total assets, you might not owe taxes, as noted on the IRS official website.

- Verbal Agreements: Collectors are trained to lie. They will say “Pay $500 today and we’ll clear the rest.” If you don’t have that in writing, they will just take the $500 and keep hounding you for the rest.

- Giving Access to Your Bank Account: Never give a collector your primary checking account info. Pay via a cashier’s check or a prepaid debit card.

Debt Settlement vs. Bankruptcy (Detailed Comparison)

| Feature | Debt Settlement | Chapter 7 Bankruptcy |

|---|---|---|

| Cost | 40-60% of debt + potential fees | ~$1,500 – $2,500 in legal/filing fees |

| Credit Report | Stays for 7 years from delinquency | Stays for 10 years |

| Asset Risk | High (if sued) | Low (due to exemptions) |

| Privacy | Private negotiation | Public record |

For a deeper dive into the legal process, see our comprehensive guide to bankruptcy.

FAQs About Debt Settlement

Can I negotiate after being sued?

Yes! In fact, many settlements happen on the courthouse steps. A lawsuit is just a more aggressive form of collection. They would still rather take a guaranteed $3,000 from you than spend $2,000 on a lawyer to try and garnish wages that you might not even have.

Will debt settlement stop a wage garnishment?

Only if the settlement is reached before the garnishment order is finalized. Once a garnish is in place, the creditor has no incentive to settle because they are already getting your money.

Can I settle debt while employed?

Absolutely. However, don’t volunteer your salary information. If they know you make $100k a year, they will fight harder for 80% of the balance.

Final Verdict – Should You Choose Debt Settlement?

Debt settlement is for the “Financially Stranded.” It is for the person who is drowning and needs a life raft, even if that life raft is a bit leaky.

Choose Debt Settlement If:

- You have more than $10,000 in unsecured debt.

- You can’t pay it off in 3 years.

- You are willing to handle 12 months of stress for a lifetime of freedom.

The Decision Checklist:

- List every debt: Total it up.

- Calculate 40%: Do you have a way to get this amount in the next 12 months?

- Check your “Suit Risk”: Do you have wages that can be easily garnished? (If yes, hire a lawyer to handle the talks).

- Commit: Once you stop paying, you must follow through. Vacillating between paying and not paying is the worst thing you can do for your finances.

Conclusion Debt settlement isn’t a “get out of jail free” card—it’s a “work-release” program. It requires discipline, nerves of steel, and a focus on the long-term goal: a $0 balance and a fresh start.