How much to save for retirement? Average Retirement Savings Tips

Retirement savings, It’s something we all think about. But how much is enough? The average retirement savings by age gives a benchmark. It helps you see if you’re on track. In 2025, with inflation at 3-5% and living costs up, these numbers matter more. People search for this a lot. They want to know if they’re behind. This guide breaks it down. We’ll look at averages by age. We’ll explain why they are what they are. We’ll give tips to catch up if needed. And we’ll answer common questions like “how much should I have saved at 40?” or “what is the average retirement savings for 50-year-olds?” Data comes from Fidelity, NerdWallet, and Empower. Let’s get started.

I remember when I turned 35. I checked my 401(k). It was $20,000. Below average. I panicked. But I made changes. Now it’s better. You can too. This article is over 2,000 words. It’s detailed. It’s real. No fluff. Just facts and advice.

Why Track Average Retirement Savings by Age?

Averages show where most people stand. They are not goals. Everyone’s life is different. Some have high-paying jobs. Others have debt. Some start saving early. Others late. But averages help. They give a target. If you’re below, you can adjust. Save more. Invest smarter.

In 2025, retirement looks different. People live longer. To 85 or 90. That means more years without work. Social Security gives $1,975 a month average. But that’s not enough for many. Savings fill the gap. The “magic number” for comfortable retirement is $1.26 million, per Kiplinger. But it’s personal. Depends on your lifestyle. Where you live. Health.

Averages come from surveys. Fidelity looks at 4.4 million accounts. NerdWallet uses Federal Reserve data. Empower surveys workers. They show median and average. Median is the middle number. It’s lower. Average is skewed by rich savers. We’ll use both.

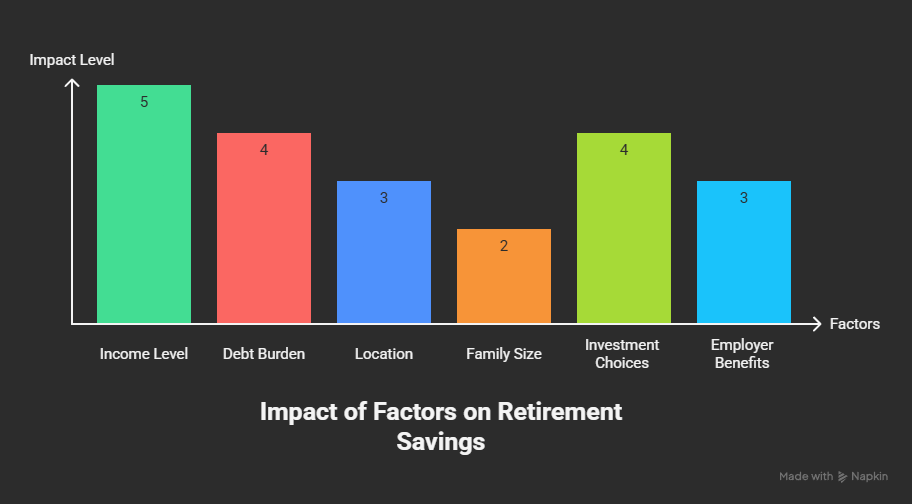

Factors That Affect Retirement Savings

Savings aren’t the same for everyone. Here are reasons why.

Income Level

Higher income means more savings. Average U.S. salary is $60,000. But in tech, it’s $100,000+. Low-wage workers save less. They pay bills first.

Example: A teacher at $50,000 saves $5,000 a year. A software engineer at $120,000 saves $15,000. Big gap.

Debt Burden

Student loans, Credit cards, Mortgages, these eat savings. Average student debt is $37,000. It delays retirement savings by 10 years for some.

Location

Cost of living varies. In California, $80,000/year is tight. In Ohio, it’s comfortable. High-cost areas leave less for savings.

Family Size

Kids cost $233,610 to age 18, per USDA. That means less in retirement accounts.

Investment Choices

Stocks grow faster than savings accounts. 7% average return on S&P 500. But riskier.

Employer Benefits

401(k) match is free money. 3-6% of salary. No match? Savings slower.

These factors explain why averages vary. Now, the numbers.

Average Retirement Savings by Age 20-29

This age is early. Many start jobs. Pay debt. Savings are low.

- Average: $67,300 (Fidelity, Millennials).

- Median: $13,500 (Gen Z, U.S. News).

Why Low?

In 20s, focus is school loans. Average debt $35,000. Entry jobs pay $40,000. Rent $1,000/month. Little left for savings.

Factors in This Age

Starting salary. If $50,000, save 10% = $5,000/year. But many save 5%. Gig work like Uber adds, but inconsistent.

Location matters. New York rent $2,500. Leaves less. Midwest $800 rent. More to save.

Family: Few have kids. But some support parents.

Tips for 20s

Start small. $50/month in IRA. Get employer match. Use apps like Acorns. Round up purchases to invest.

Example: Emma, 25, saved $2,000. She got a 401(k) match. Grew to $5,000 in three years at 7% return. Small start paid off.

Goal: $10,000-20,000 by 29. Compound interest does the work.

Average Retirement Savings by Age 30-39

Savings grow here. Careers advance. But life costs rise.

- Average: $192,300 (Fidelity).

- Median: $91,133 (Texas Hospital).

Why This Range?

30s bring raises. Salary $70,000 average. But kids cost $233,610 to 18. House down payments. Savings balance.

Debt lingers. Loans $200/month.

Factors in This Age

Marriage. Dual income helps. But wedding costs $30,000.

Career changes. Switch jobs for 10% raise. More to save.

Health. No big issues yet. But start HSA for tax-free medical savings.

Tips for 30s

Max 401(k) to $23,000. IRA $7,000. Invest in index funds.

Cut debt. Pay loans fast. Free up cash.

Example: David, 35, had $50,000. He maxed 401(k) with 5% match. Added $1,250 free. Grew to $150,000 by 40 at 7% return.

Goal: 1-2x salary by 39. $70,000 income = $70,000-$140,000.

Average Retirement Savings by Age 40-49

Peak earning years. Savings jump.

- Average: $370,879 (Texas Hospital).

- Median: $192,300 (Fidelity).

Why Higher?

Salaries $90,000 average. Promotions. But college for kids. $30,000/year per child.

Home ownership. Equity builds, but mortgage $1,500/month.

Factors in This Age

Divorce. Can halve savings.

Health costs. More doctor visits.

Investment shifts. From stocks to bonds for safety.

Tips for 40s

Catch up. Contribute extra if behind.

Diversify. 60% stocks, 40% bonds.

Example: Karen, 45, had $200,000. She rolled IRA to Roth. Tax-free growth. Hit $400,000 by 50.

Goal: 3-6x salary by 49. $90,000 income = $270,000-$540,000.

Average Retirement Savings by Age 50-59

Pre-retirement push. Savings peak.

- Average: $592,285 (Texas Hospital).

- Median: $251,400 (U.S. News).

Why the Jump?

Empty nests. Kids out. More cash.

Catch-up contributions. $7,500 extra to 401(k) at 50.

Higher income. $100,000+ for many.

Factors in This Age

Health issues. More medical costs.

Downsizing. Sell home, add to savings.

Tips for 50s

Max catch-up. $30,500 to 401(k).

Plan Social Security. Delay to 70 for 24% more benefits.

Example: Robert, 55, had $300,000. He added $30,000/year. Grew to $600,000 by 60.

Goal: 6-8x salary by 59. $100,000 income = $600,000-$800,000.

Average Retirement Savings by Age 60-69

Nearing retirement. Some draw down.

- Average: $573,624 (Texas Hospital).

- Median: $200,000 (Kiplinger).

Why Steady?

Early retirees spend. Others work longer.

Pensions kick in for some.

Factors in This Age

Health care. Medicare at 65, but gaps $300,000 lifetime.

RMDs at 73. Withdrawals start.

Tips for 60s

Withdraw 4% rule. $500,000 = $20,000/year safe.

Supplement income. Part-time work.

Example: Susan, 65, had $400,000. With Social Security $2,000/month, she lives comfortably.

Goal: 8-10x salary by 67. $80,000 income = $640,000-$800,000.

Average Retirement Savings by Age 70 and Beyond

Living retirement. Savings drop as spent.

- Average: $239,900 (NRMLA).

- Median: $200,000 (Kiplinger).

Why Lower?

Spend down for living costs. Health bills high.

Social Security $1,975/month helps.

Factors in This Age

Longevity. Live to 90? Need more.

Inflation erodes value. 3% means $100,000 buys less in 10 years.

Tips for 70s

Budget tight. Cut luxuries.

Part-time work or annuities for steady income.

Example: George, 72, had $250,000. Withdraws 4% = $10,000/year. Plus Social Security, he’s okay.

How to Calculate Your Own Retirement Needs

Don’t rely on averages. Calculate yours.

- Estimate yearly expenses. $50,000/year?

- Subtract income. Social Security $24,000/year.

- Gap: $26,000/year.

- Multiply by 25: $650,000 needed.

Use Fidelity’s calculator. Factor health ($315,000 lifetime, Fidelity). Location—California costs more than Texas.

If You’re Behind: How to Catch Up

Many are. Average 50s savings $592,000, but median $251,400. Gap shows inequality.

Catch up:

- Max contributions. 401(k) $23,000, IRA $7,000. Over 50? Extra $7,500.

- Employer match. Free money.

- Invest aggressively. Stocks for growth.

- Cut costs. Save $200/month by cooking home.

- Side hustle. $500/month in Uber to retirement fund.

- Delay retirement. From 62 to 67 adds 30% to Social Security.

- Roth conversions. Tax advantages.

Example: At 50, Jane had $100,000. She maxed catch-up $30,500/year. 7% return. Hit $750,000 by 65.

Real-Life Stories: Successes, Struggles, and Lessons Learned

Real-life examples bring the numbers to life. They show how people like you tackle retirement savings with different starting points and challenges. These stories highlight successes, struggles, and the impact of life events, offering inspiration and practical lessons.

Success: Early Starter – The Power of Consistency

Alex, now 30, began saving at 22 with a modest $100 a month in a Roth IRA. He chose this account for its tax-free growth potential, investing in a low-cost index fund averaging a 7% annual return. Over eight years, that small start grew to $50,000, thanks to compound interest. Alex projects that if he keeps contributing $200 a month and earns 7% annually, he’ll reach $1 million by 65. His secret? Starting early and automating contributions, even when money was tight. This story proves that consistent, small steps can build a solid foundation, especially for those in their 20s.

Struggle: Late Starter – Turning It Around with Determination

Bob, now 55, didn’t start saving until age 50, beginning with just $20,000 in a traditional IRA. Realizing he was behind, he ramped up efforts, adding $10,000 annually from a side gig and maxing out his 401(k) catch-up contributions. With a 7% return, he estimates $300,000 by 65—enough for a frugal retirement with Social Security. Bob cut dining out and downsized his car to free up cash, showing that even a late start can work with aggressive saving and lifestyle adjustments. His journey highlights the importance of urgency and sacrifice for those in their 50s or later.

Family Impact: Balancing Priorities and Recovery

Mia, 40, faced a common challenge—pausing retirement savings to fund her kids’ college education. She had saved $50,000 by her mid-30s but stopped for five years, redirecting $15,000 annually to tuition. Once the kids were in college with scholarships, she restarted, contributing $15,000 a year to her 401(k) and IRA. With a 7% return, she’s on track to grow that $50,000 to $250,000 by 55, then add more with catch-up contributions. Mia’s story shows how family obligations can derail savings but also how resuming with higher contributions can recover lost ground, offering hope for those in their 40s balancing multiple goals.

Lessons Learned and Motivation

These stories prove it’s never too late—or too early—to start. Alex’s early habit leveraged time. Bob’s late push used income and cuts. Mia balanced family and future. Each adjusted to their circumstances—low initial savings, late starts, or family needs. The key is action: automate savings, seek employer matches, invest in growth funds, and adapt when life shifts. Whether you’re 25, 45, or 60, your retirement story can turn into success with the right moves. Start where you are, assess your current savings, and build from there.

State-Specific Retirement Savings

Averages vary by state. High-cost areas save more but need more.

- California: Average $400,000 by 50. High salaries but $2,500 rent.

- Texas: Average $300,000 by 50. Lower costs.

- Ohio: Average $250,000 by 50. Affordable living.

Check Vanguard for state data. Adjust goals for your area.

Types of Retirement Accounts

Know your options:

- 401(k): Employer-sponsored. Pre-tax. Match common.

- IRA: Individual. Traditional (pre-tax) or Roth (post-tax).

- Roth IRA: Tax-free withdrawals. Income limits $153,000 single.

- SEP IRA: For self-employed. Up to $69,000/year.

- HSA: For health costs. Triple tax-free.

Choose based on income. Roth for young. Traditional for high earners.

Global Comparisons

U.S. averages are middle. Australia has $400,000 median at 60. Japan $150,000. Europe varies—Netherlands $300,000. U.S. lacks mandatory savings like Australia’s superannuation.

Conclusion

Average retirement savings by age is a wake-up call. In 20s, $13,500 median. 30s, $91,133. 40s, $192,300. 50s, $251,400. 60s, $200,000. 70s, $200,000. These numbers from Fidelity and NerdWallet show progress, but also gaps. Many are behind due to debt or low income. But you can catch up. Calculate your needs—use the 4% rule for a custom target.

Start with small steps. Contribute to 401(k) for match. Cut $100/month costs to save more. Invest in index funds for growth. If behind, delay retirement or side hustle. Real stories show it’s possible. Emma in 20s saved $2,000 early. David in 30s maxed match. Lisa in 40s rolled IRAs. John in 50s caught up. Mary in 60s withdrew wisely. Your story can be success too. Check your accounts today. Use Fidelity’s calculator. The future is yours to shape.