How Alternative Credit Data Helps You Build Credit in 2025

Building a strong credit profile is essential for financial stability, but for millions of Americans especially young adults, immigrants, or those with limited credit history traditional credit data like credit card payments or loans may not tell the full story. Enter alternative credit data, a gamec hanger in 2025 that leverages non-traditional sources like utility payments, phone bills, and rent to help you build credit and access better financial opportunities. This comprehensive guide explores how alternative data works, its impact on credit building, and why it’s trending, addressing key queries like “What is alternative credit data?” and “How can utilities, phone bills, and rent boost my credit score?”

With rising interest in alternative credit data, driven by new legislation like the Credit Access and Inclusion Act and platforms like AxcessRent, this article here is roadmap to understanding and using alternative data effectively. Whether you’re a first-time renter or someone with a thin credit file, this guide answers trending questions and provides actionable steps to improve your credit score.

What Is Alternative Credit Data?

Alternative credit data refers to non-traditional financial information used to assess creditworthiness beyond standard credit reports from bureaus like Experian, Equifax, and TransUnion. Traditional credit scoring relies heavily on loans, credit cards, and mortgages, but alternative data includes:

- Utility Payments: Electricity, gas, water, and internet bills.

- Phone Bills: Mobile and landline payment histories.

- Rent Payments: Monthly rent paid to landlords or property managers.

- Other Sources: Subscription services, bank account cash flow, or even social media activity.

This data paints a fuller picture of financial responsibility, especially for the estimated 80 million Americans who are “credit invisible” or have thin credit files, according to PYMNTS research. In 2025, alternative data is gaining traction as a tool to boost financial inclusion, particularly for underserved groups like young people, immigrants, or those in rural areas.

Why Alternative Data Matters in 2025

The traditional credit system often excludes people who pay bills on time but lack conventional credit products. For example, consistently paying $1,500 in rent or $100 in utilities monthly demonstrates financial reliability, yet these payments typically don’t appear on credit reports. New legislation, like the Credit Access and Inclusion Act introduced in April 2025, aims to change this by allowing credit bureaus to incorporate alternative data, such as rent and utility payments, to help millions build credit histories.

This shift is critical in a year when economic pressures—like resumed student loan payments and rising costs (average emergency expense: $1,400, per PYMNTS)—make credit access vital. Alternative data bridges the gap, offering a pathway to loans, credit cards, or better interest rates for those previously sidelined by traditional scoring.

Types of Alternative Credit Data for Better Credit Decisions

Alternative data encompasses a range of sources that lenders and credit bureaus use to evaluate creditworthiness. Here are six key types trending in 2025, inspired by resources like RiskSeal and Fyndoo:

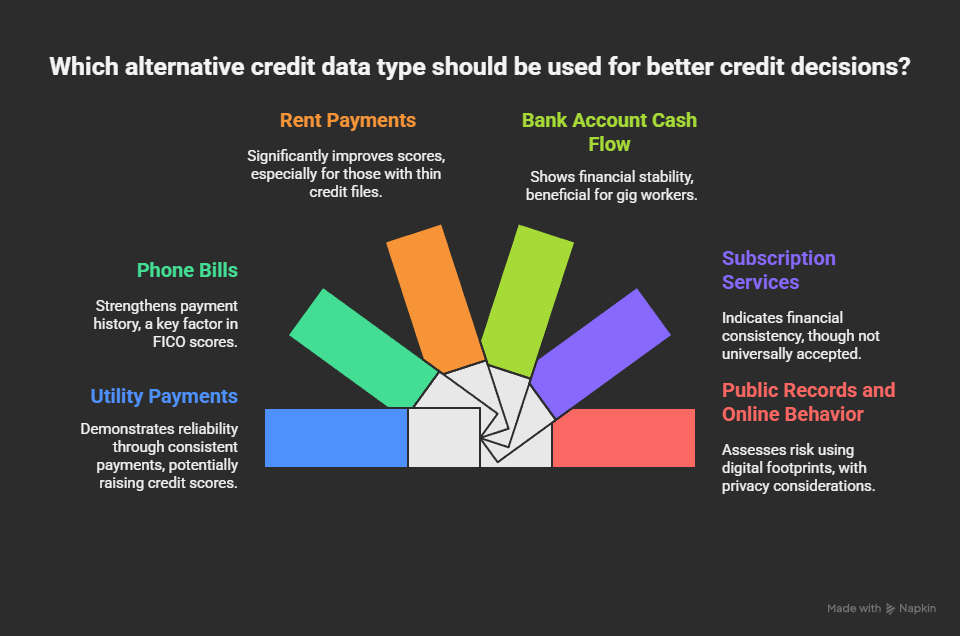

- Utility Payments:

- What It Includes: Electricity, gas, water, and internet bills.

- Impact: On-time payments demonstrate reliability. For example, consistent $200/month utility payments reported via Experian Boost can raise your credit score by 20–50 points in months.

- Example: A $150 electric bill paid on time each month shows financial discipline.

- Phone Bills:

- What It Includes: Mobile phone contracts or prepaid plans.

- Impact: Regular payments to providers like Verizon or T-Mobile can be reported to credit bureaus, boosting your payment history, a key factor in FICO scores (35% weight).

- Example: Paying a $70/month phone bill consistently strengthens your credit profile.

- Rent Payments:

- What It Includes: Monthly rent paid to landlords or property managers.

- Impact: Services like AxcessRent report rent payments to credit bureaus, significantly improving scores for those with thin files. A $1,200/month rent payment reported for a year can elevate your score substantially.

- Example: A first-time renter using AxcessRent to report $1,500/month payments builds a positive credit history.

- Bank Account Cash Flow:

- What It Includes: Income inflows, spending patterns, and savings from checking or savings accounts.

- Impact: Open banking data, supported by platforms like Fyndoo, shows lenders your financial stability, especially for gig workers or self-employed individuals.

- Example: Consistent $3,000/month inflows with low overdrafts signal reliability.

- Subscription Services:

- What It Includes: Payments for streaming services (e.g., Netflix), gym memberships, or software subscriptions.

- Impact: Regular payments indicate financial consistency, though not all bureaus accept this data yet.

- Example: A $15/month Netflix subscription paid on time adds to your positive payment history.

- Public Records and Online Behavior:

- What It Includes: Tax payment records, legal filings, or social media activity (used cautiously due to privacy concerns).

- Impact: Platforms like Scoreplex analyze digital footprints from 140+ sources to assess risk, helping lenders make informed decisions.

- Example: Consistent tax payments or professional LinkedIn activity can support creditworthiness.

These data types, highlighted in sources like RiskSeal’s 2025 Guide, enable lenders to make better loan decisions while helping consumers build credit without relying solely on traditional metrics.

How Alternative Data Boosts Credit Access

Alternative data addresses a critical issue: financial inclusion. Globally, 1.4 billion people are unbanked, and in the U.S., 5.6 million households lack bank accounts, per the World Economic Forum. Traditional credit scoring excludes these groups, but alternative data offers a solution:

- For the Unbanked: Utility and rent payments provide a credit-building pathway without requiring a bank account.

- For Young People: Millennials and Gen Z, who may not yet have credit cards or loans, can use rent or phone bill payments to establish credit.

- For Immigrants: Newcomers lacking U.S. credit history can leverage alternative data to access loans or rentals.

- For Rural Residents: Those in areas with limited banking access can use utility payments to build credit profiles.

The Credit Access and Inclusion Act (April 2025) supports this by mandating credit bureaus to include alternative data, potentially helping 40 million “credit invisible” Americans, as noted by Senator Tim Scott. This legislation, combined with tools like Experian Boost and AxcessRent, makes 2025 a pivotal year for credit building.

How to Use Utilities, Phone Bills, and Rent to Build Credit

Here’s a step-by-step guide to leveraging alternative data for credit building in 2025:

Step 1: Enroll in a Reporting Service

- Tools: Sign up for AxcessRent (for rent) or Experian Boost (for utilities and phone bills). These platforms report payments to major credit bureaus.

- Cost: AxcessRent and Experian Boost are often free or low-cost (e.g., $5–$10/month for premium features).

- Example: A renter paying $1,500/month uses AxcessRent to report to TransUnion, boosting their score over time.

Step 2: Pay Bills on Time

- Why It Matters: Payment history is 35% of your FICO score. Late payments hurt your score, so set up auto-pay for utilities, phone bills, and rent.

- Tip: Use reminders or budgeting apps like Mint to stay on track.

- Mistake to Avoid: Missing payments, as even one late payment can drop your score by 50+ points.

Step 3: Verify Data Reporting

- Check Your Report: Use AnnualCreditReport.com to confirm that your payments are reported correctly to Experian, Equifax, or TransUnion.

- Dispute Errors: If payments aren’t reflected, contact the reporting service or bureau to correct inaccuracies.

- Example: After three months of reported $200 utility payments, check your Experian report for updates.

Step 4: Maintain Consistent Payments

- Long-Term Impact: Consistent payments over 6–12 months can raise your score by 20–100 points, depending on your starting point.

- Example: Paying $100/month for internet and $1,200/month for rent consistently for a year can transform a thin credit file into a robust one.

Step 5: Monitor Your Credit Score

- Tools: Use Credit Karma or Experian for free score updates.

- Goal: Aim for a score of 670+ to qualify for better loans or rental applications.

- Tip: Track progress monthly to stay motivated and catch issues early.

Benefits of Alternative Data for Credit Building

Using alternative data like utilities, phone bills, and rent offers multiple benefits:

- Improves Credit Scores: Adds positive payment history, crucial for thin-file consumers.

- Increases Loan Approval Odds: Lenders see a fuller picture, improving access to credit cards, auto loans, or mortgages.

- Reduces Interest Rates: Higher scores lead to lower rates, saving thousands over a loan’s life.

- Enhances Financial Inclusion: Helps underserved groups like young adults, immigrants, or low-income individuals.

- Supports Rental Applications: A stronger credit profile impresses landlords, especially in competitive markets.

For example, a first-time renter with no credit history who reports $1,500/month rent payments via AxcessRent could raise their score from 550 to 650 in six months, improving their chances of securing a car loan at a 5% lower interest rate.

Challenges and Considerations

While alternative data is powerful, there are challenges to consider:

- Not All Bureaus Accept It: Some bureaus or lenders may not factor in alternative data yet, though adoption is growing in 2025.

- Privacy Concerns: Sharing bank or social media data raises privacy issues. Ensure services comply with regulations like GDPR or CCPA.

- Late Payments Hurt: If reported, missed payments can lower your score, so consistency is critical.

- Costs of Services: Some reporting tools charge fees, so compare options like AxcessRent (rent-focused) versus Experian Boost (utilities-focused).

Mistake to Avoid: Signing up for a reporting service without confirming it reports to all three major bureaus, as limited reporting may reduce impact.

Tools and Resources for Credit Building with Alternative Data

- AxcessRent: Reports rent payments to credit bureaus, ideal for renters building credit.

- Experian Boost: Free tool to report utility and phone bill payments.

- Credit Karma: Monitor your credit score and track alternative data impacts.

- AnnualCreditReport.com: Free credit reports to verify reported payments.

- Fyndoo: Platform for analyzing bank cash flow data for credit decisions.

- Scoreplex: Assesses digital footprints for lenders, including public records.

Conclusion

In 2025, alternative credit data—utilities, phone bills, and rent—is revolutionizing credit building, making it easier for first-time renters, young adults, and others with thin credit files to access loans, rentals, and better financial opportunities. By using tools like AxcessRent and Experian Boost, you can report consistent payments to boost your credit score by 20–100 points in months. New legislation like the Credit Access and Inclusion Act supports this trend, promoting financial inclusion for millions. Start by checking your credit at AnnualCreditReport.com, enrolling in a reporting service, and paying bills on time. For more credit-building tips, visit AxcessRent and take control of your financial future today.

FAQs

What Is Alternative Credit Data and What Is It Used For?

Alternative credit data includes non-traditional financial information like utility payments, phone bills, rent, and subscriptions used to assess creditworthiness. It helps lenders evaluate those with limited or no credit history, boosting financial inclusion for loans, rentals, or credit cards.

What Are Examples of Alternative Credit Data?

Examples include:

- Utility payments (electricity, gas, internet).

- Phone bill payments (mobile or landline).

- Rent payments to landlords or property managers.

- Bank account cash flow (income, spending patterns).

- Subscription services (Netflix, gym memberships).

- Public records or online behavior (tax payments, social media activity).

How Can Utilities, Phone Bills, and Rent Build Credit?

Services like AxcessRent and Experian Boost report these payments to credit bureaus, adding positive payment history to your credit file. Consistent payments of $100/month for utilities or $1,200/month for rent can raise your score by 20–50 points in months.

How Does Alternative Data Boost Credit Access?

It provides a fuller picture of financial responsibility, helping “credit invisible” individuals (e.g., young adults, immigrants) qualify for loans or rentals. Legislation like the Credit Access and Inclusion Act (2025) supports this by mandating bureau inclusion of alternative data.

What Are the Benefits of Using Alternative Data for Credit Building?

Benefits include improved credit scores, better loan approval odds, lower interest rates, enhanced financial inclusion, and stronger rental applications. For example, reporting $1,500/month rent can boost your score significantly.

Are There Risks to Using Alternative Data?

Risks include privacy concerns, potential fees for reporting services, and the impact of missed payments on your score. Always verify the service’s credibility and bureau reporting capabilities.