FAFSA Mistakes to Avoid: Stop Losing Free College Money

The Free Application for Federal Student Aid (FAFSA) is the single most important document in a student’s journey toward an affordable college education. Every year, billions of dollars in federal grants, work-study funds, and low-interest loans are distributed based on the data provided in this form. However, billions more are left on the table because of simple, avoidable errors.

Filling out the FAFSA can feel like navigating a minefield of financial jargon and bureaucratic red tape. One wrong number or a misunderstood question can result in a significantly higher Student Aid Index (SAI), potentially costing a family thousands of dollars in “free money.” To ensure you maximize your aid package, avoid these critical FAFSA mistakes.

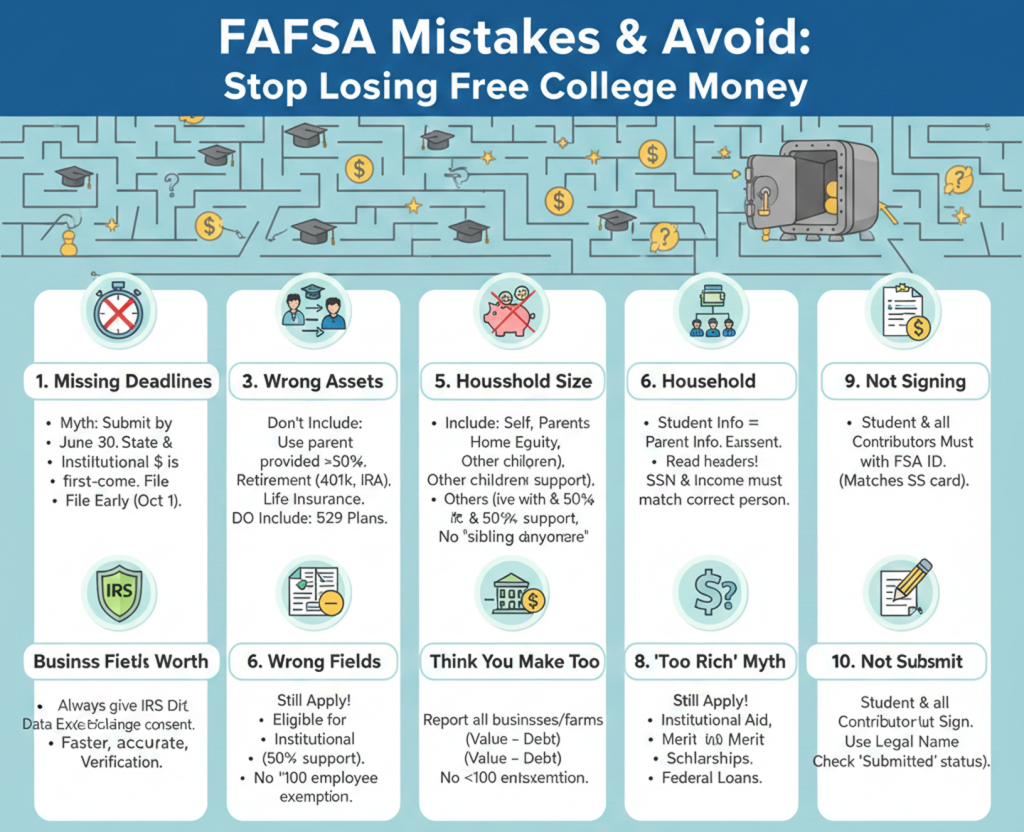

1. Missing Deadlines: The “First-Come, First-Served” Trap

One of the most tragic mistakes families make is assuming that as long as they submit before the final federal deadline (usually June 30 of the following year), they are safe. This is a myth.

While the federal deadline is generous, state and institutional deadlines are much earlier—often as early as February or March. Many states have a “first-come, first-served” policy for their grant programs. Once that pot of money is empty, it’s gone. If you wait until May to file, you might still get federal Pell Grants, but you could completely miss out on thousands of dollars in state-specific scholarships.

The Fix: Aim to submit the FAFSA as soon as it opens (traditionally October 1, though sometimes delayed for system updates). Check the specific deadlines for every college on your list and your state’s higher education agency.

2. Misidentifying the “Contributor” (Parental Confusion)

With the recent “FAFSA Simplification,” the term “Contributor” has become central. A common mistake in households where parents are divorced or separated is providing the financial information of the wrong parent.

Previously, the rule was to use the parent with whom the student lived most. The new rule requires the parent who provided the most financial support over the last 12 months to be the contributor. If both parents provided equal support, the parent with the higher income or assets is typically the one whose information is required.

The Fix: Carefully review the financial support levels before starting. If your “primary” parent has remarried, your stepparent’s income and assets must also be included. Failing to include a stepparent is considered a fraudulent filing and will be caught during the verification process.

3. Reporting the Wrong Assets (And Over-Reporting)

This is where families lose the most money. The FAFSA asks for the net worth of investments, but many people include things they shouldn’t, which artificially inflates their wealth and lowers their aid.

- Mistake: Including your primary residence. You should never report the equity in the home you live in. The FAFSA only cares about “investment properties” (vacation homes or rentals).

- Mistake: Including retirement accounts. Do not report the value of your 401(k), 403(b), IRA, or pension plans. These are protected assets.

- Mistake: Including life insurance values. The cash value of a life insurance policy is not considered an asset for FAFSA purposes.

Conversely, families often forget to report 529 College Savings Plans. If the plan is owned by the parent for the student (or any other children in the household), it must be reported as a parental asset.

4. Failing to Use the Direct Data Exchange (DDX)

In the past, users manually entered tax data, leading to countless typos. The new FAFSA uses the IRS Direct Data Exchange (DDX) to pull tax information automatically.

Many applicants hesitate to grant consent for this exchange, fearing privacy issues or wanting to “tweak” the numbers. This is a mistake. Refusing to provide consent makes the student ineligible for federal student aid entirely. Furthermore, manual entry significantly increases the likelihood that your application will be flagged for “Verification,” a tedious process where you must prove every number on your form with physical documentation.

The Fix: Always provide consent for the DDX. It is faster, more accurate, and drastically reduces your chances of being audited by the financial aid office.

5. Miscounting Household Size

The Student Aid Index (SAI) calculation is heavily influenced by how many people live in your household. A common mistake is only including immediate family or failing to include children who are away at college but still supported by the parents.

You should include:

- Yourself (the student).

- The parents (including a stepparent).

- The parents’ other children, even if they don’t live at home, provided the parents provide more than half of their financial support.

- Other people (like grandparents) who currently live with the parents and receive more than half of their support from them.

Note: A major change in the new FAFSA is that having multiple siblings in college no longer provides a “discount” or automatic reduction in SAI. However, schools may still consider this during a Professional Judgment appeal, so keep track of those tuition bills.

6. Inputting Information into the Wrong Fields

It sounds simple, but switching the “Student” and “Parent” sections is one of the most frequent errors. If a parent accidentally enters their own social security number in the student’s field, or enters their income in the student’s income section, the form will either be rejected or will show the student as having massive earnings, disqualifying them from need-based aid.

The Fix: Read the header of every page. If it says “Student Financials,” it is asking about the student’s bank account and job, not the parents’.

7. Reporting “Net Worth” of a Small Business or Family Farm

Under the old FAFSA rules, small family businesses with fewer than 100 employees were exempt from being reported as assets. This exemption is gone. Now, the net worth of all businesses and for-profit farms must be reported. Families often make the mistake of reporting the total value of the business rather than the net worth (Value minus Debt). If you have a business worth $500,000 but owe $400,000 on equipment and property, your asset is $100,000, not $500,000.

8. Not Submitting Because You Think You “Make Too Much Money”

This is perhaps the biggest mistake of all. Many families assume that because they have a six-figure income, they won’t qualify for anything. While they might not qualify for a federal Pell Grant, they might still qualify for:

- Institutional Aid: Many expensive private colleges have large endowments and give need-based aid to families making $150k or even $200k.

- Merit Aid: Some schools require a FAFSA on file to award merit-based scholarships, regardless of financial need.

- Federal Student Loans: To access the $5,500+ in federal direct loans (which have better protections than private loans), a FAFSA is mandatory.

9. Leaving Fields Blank

The FAFSA system can be sensitive. Leaving a field blank instead of entering a “0” can sometimes cause the system to treat the application as incomplete. If a question does not apply to you and it is a numeric field, enter “0”.

Additionally, ensure you are using your legal name as it appears on your Social Security card. If you use a nickname (e.g., “Alex” instead of “Alexander”), the Social Security Administration match will fail, and your application will be stalled for weeks.

10. Forgetting to Sign and Submit

It sounds ridiculous, but thousands of students finish the entire form and then simply close the browser window without clicking the final “Submit” button or completing the “Sign” section with their FSA ID.

Both the student and the contributor (parent) must sign the form with their respective FSA IDs. If one party signs but the other doesn’t, the FAFSA remains in “In-Process” or “Draft” status and is never sent to the colleges.

The Fix: Check your email for a confirmation message with a Data Release Number (DRN). If you don’t have that email, your FAFSA has not been submitted.

Conclusion: The Path to Maximum Aid

Avoiding these mistakes requires patience and attention to detail. The FAFSA is not a document to be rushed through on a Sunday night at 11:00 PM. Treat it as a high-stakes financial transaction.

By filing early, using the IRS data tool, correctly identifying your assets, and ensuring all contributors provide their signatures, you protect yourself from the clerical errors that lead to lost funding. Remember, the financial aid office at your target college is there to help. If your financial situation has changed significantly since your last tax return (due to job loss, medical bills, or death), file the FAFSA as-is first, then contact the school for a “Professional Judgment” review. Don’t leave your “free money” to chance—double-check every line.

Frequently Asked Questions (FAQs)

Q: I have two siblings in college. Does the FAFSA still give us a “sibling discount”?

A: No. Under the new FAFSA rules, the “number in college” is no longer part of the federal formula for the Student Aid Index (SAI). However, colleges still ask this question on the form. While the federal government won’t give you extra aid for it, individual colleges may use their own funds to help families with multiple tuitions. Always ask the financial aid office if they offer an institutional sibling allowance.

Q: What if my parents refuse to provide their information?

A: If your parents refuse to help, you can still submit the FAFSA, but you will likely only be eligible for unsubsidized federal loans. You will need to indicate on the form that you have “unusual circumstances” or that you are unable to provide parental data. This usually triggers a request for a “Dependency Override” from your college’s financial aid office, which requires significant documentation of your estrangement or situation.

Q: My parents are divorced. Which parent do I invite as a “Contributor”?

A: You must invite the parent who provided the most financial support to you during the last 12 months. If that parent is remarried, your stepparent is also considered a contributor and their information will be required as part of that parent’s section.

Q: Does my parent see my information, and do I see theirs?

A: No. The FAFSA is designed for privacy. When you “invite” a contributor via their email and FSA ID, they log in to their own portal. They cannot see your specific financial answers (like your bank balance), and you cannot see theirs. The system merges the data in the background for the government.

Q: I’m a student and I have a part-time job. Will my earnings hurt my financial aid?

A: There is a “Student Income Protection Allowance” (usually around $10,000+ depending on the year). If you earn less than this amount, your income generally has zero impact on your SAI. Even if you earn more, it is usually assessed at a lower rate than parental income. Don’t be afraid to work!

Q: What happens if I make a mistake after I’ve already submitted?

A: Once your FAFSA is “Processed” (usually 1-3 days after submission), you can log back in and click “Make Corrections.” You can add more schools, fix typos, or update your address. However, you generally cannot change your “Financial Assets” as of the day you originally signed the form—those are intended to be a “snapshot” in time.

Q: Do I have to pay a fee to file the FAFSA?

A: Absolutely not. The “F” in FAFSA stands for Free. If you are on a website that asks for a credit card number to submit your FAFSA, you are on a scam site. Always use studentaid.gov.