Budget vs. Forecast: Understanding the Critical Differences

In the world of finance, the terms “budget” and “forecast” are often used interchangeably by laypeople. However, for a business owner, CFO, or serious investor, they represent two distinct tools with vastly different purposes.

While a budget acts as the blueprint for where you want to go, a forecast is a reality check on where you are actually heading. Understanding the interplay between these two is the difference between a business that survives and one that thrives.

What is a Budget?

A budget is a formal financial plan for a specific period (usually a fiscal year). It represents the organization’s goals, expectations, and authorized spending limits. It is a static document that serves as a benchmark for performance.

- Nature: Tactical and Strategic.

- Tone: “What do we intend to happen?”

- Focus: Goal-setting and control.

What is a Forecast?

A financial forecast is a projection of future financial outcomes based on historical data and current market trends. Unlike a budget, a forecast is dynamic. It is updated throughout the year to reflect new information, such as a sudden shift in consumer behavior or a change in supply costs.

- Nature: Predictive and Analytical.

- Tone: “What is actually likely to happen?”

- Focus: Realism and agility.

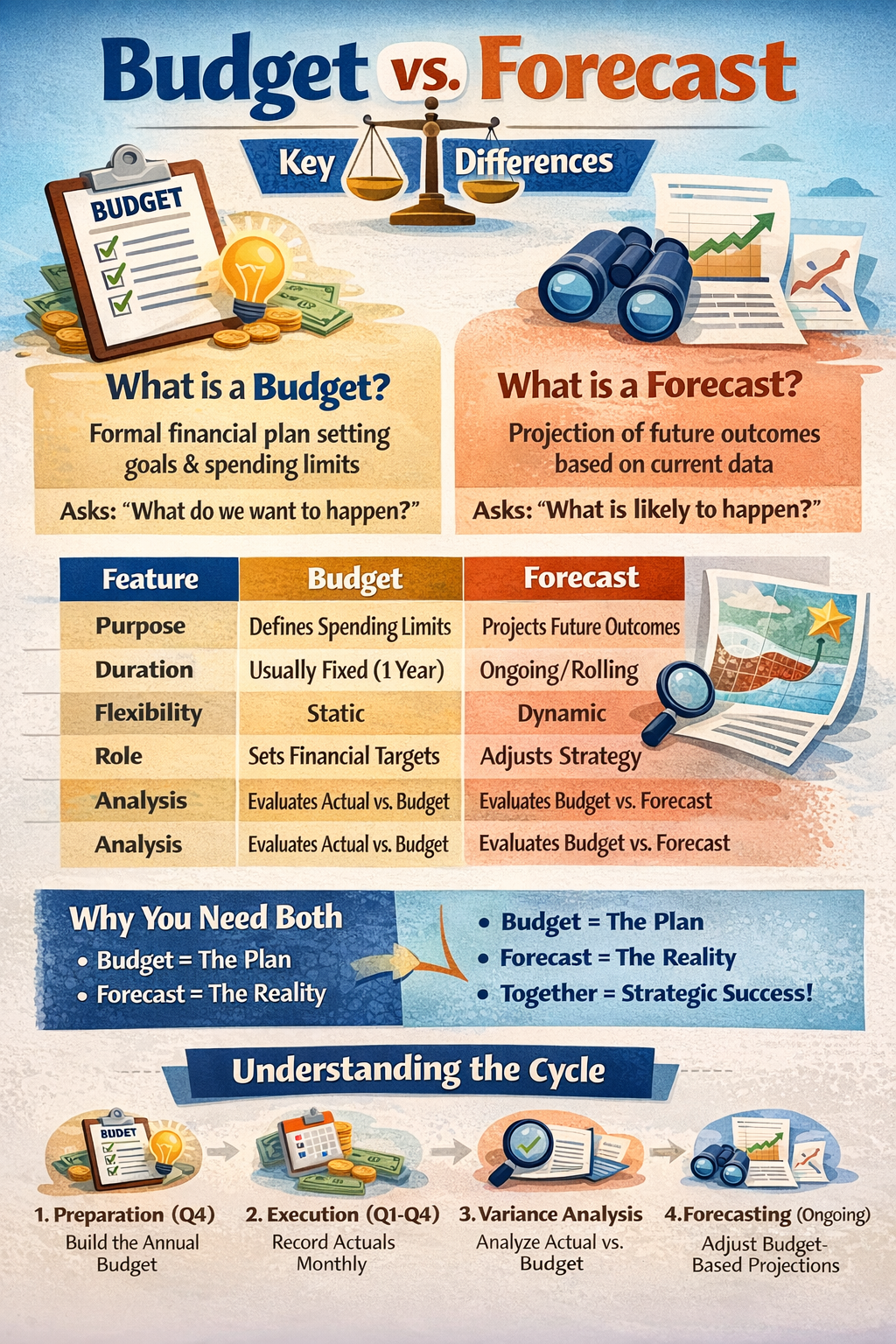

The Key Differences: Budget vs. Forecast

| Feature | Budget | Forecast |

|---|---|---|

| Purpose | Sets goals and defines spending limits. | Predicts future outcomes based on current data. |

| Duration | Usually fixed (1 year). | Ongoing/Rolling (Short-term or Long-term). |

| Flexibility | Static; usually changed only under extreme circumstances. | Dynamic; updated monthly or quarterly. |

| Management Role | Used to hold managers accountable (KPIs). | Used to adjust strategy and operations. |

| Variance Analysis | Compares Actuals vs. Budget. | Compares Budget vs. Forecast. |

| Incentives | Often tied to bonuses and compensation. | Rarely tied to compensation; focus is on accuracy. |

Why You Need Both: The Synergy of Planning

Using only a budget is like trying to sail across the ocean with a map but refusing to look at the weather. Using only a forecast is like watching the weather but having no destination.

The Budget as a “North Star”

The budget provides the organization with a unified goal. It ensures that the marketing department, the product team, and the operations crew are all working toward the same revenue targets and profit margins. It provides the discipline required to prevent overspending.

The Forecast as “Radar”

The forecast allows the company to pivot. If the budget was set in January with an expectation of 10% growth, but the June forecast shows a recession is looming, the forecast gives leadership the data they need to cut costs before the budget is officially blown.

The Process: How a Budget Becomes a Forecast

In a healthy financial cycle, the process follows a specific rhythm:

- Preparation (Q4): The budget is built for the upcoming year based on strategic goals.

- Execution (Q1-Q4): The business operates, and “Actuals” (real spending/revenue) are recorded.

- Variance Analysis: Every month, the finance team compares Actuals vs. Budget.

- Forecasting (Ongoing): Based on those variances, the team creates a “Rolling Forecast.” If the Actuals were lower than the Budget in Q1, the Forecast for Q2-Q4 is adjusted downward to reflect reality.

Implementation Strategies for Modern Businesses

The Top-Down vs. Bottom-Up Budget

- Top-Down: Leadership sets the targets, and departments find ways to meet them. This is fast but can lead to “unrealistic” goals.

- Bottom-Up: Every department submits their needs. This is more accurate but can lead to “budget padding.”

Rolling Forecasts

Modern finance is moving away from static annual forecasts toward Rolling Forecasts. Instead of forecasting until the end of the fiscal year, a rolling forecast always looks 12 months ahead. As one month ends, another is added to the tail end. This ensures the company is never caught off guard by the “year-end” cliff.

The Psychology of Financial Planning

There is a psychological tension between budgeting and forecasting.

Budgets are about Motivation. They are often aspirational. If you set a budget that is too easy to hit, the team becomes complacent. If it’s too hard, they become discouraged.

Forecasts are about Truth. A forecast that is “aspirational” is a failure. If a sales manager forecasts $1M in sales just to please the CEO, but only $500k is realistic, the company might over-hire or over-order inventory, leading to a cash flow crisis.

Common Pitfalls to Avoid

- Treating the Forecast as a Second Budget: Do not use the forecast to punish employees. If you do, they will stop providing honest predictions.

- Ignoring External Data: A budget is internal, but a forecast must be external. It should account for interest rates, competitor moves, and global events.

- Static Budgeting in a Volatile Market: In fast-moving industries (like Tech), a 12-month static budget is often obsolete by month three. These companies must prioritize the forecast over the budget.

Conclusion

In summary, the budget is your plan, while the forecast is your reality. The budget tells you what you should spend to reach your goals; the forecast tells you what you will have to spend based on how the world is changing.

Successful organizations use the budget to drive accountability and the forecast to drive adaptability. By mastering both, you create a financial framework that is both disciplined and resilient.

Frequently Asked Questions (FAQs)

Can a budget be changed once it is approved?

In most corporate settings, the “Original Budget” is never changed so that it can be used for year-end performance reviews. However, companies may create a “Revised Budget” if there is a massive structural change (like a merger or a global pandemic).

Which is more important for a startup?

For a startup, the forecast is usually more important. Since startups have little historical data, their initial budgets are often guesses. A weekly or monthly cash flow forecast is vital to ensure the startup does not run out of money (burn rate).

What is “Budget Variance”?

Budget variance is the difference between the budgeted amount and the actual amount spent or earned. A “Favorable Variance” means you spent less or earned more than planned. An “Unfavorable Variance” means you spent more or earned less.

Who is responsible for creating these documents?

The Budget is usually a collaborative effort between department heads and the Finance/Accounting team. The Forecast is typically handled by the Financial Planning and Analysis (FP&A) team, often using inputs from the Sales and Operations departments.

How does Zero-Based Budgeting (ZBB) affect forecasting?

ZBB makes the initial budget much more accurate because every expense is justified. This usually leads to fewer “shocks” in the forecast later in the year, as the “waste” was already removed during the budgeting phase.

Does a forecast include non-cash items?

While a budget often focuses on the Income Statement (Profit/Loss), a good forecast should focus heavily on the Cash Flow Statement. Knowing when cash actually enters and leaves the bank is more important for short-term survival than accounting profit.