What Is Mortgage Recasting and How Does It Work?

What Is Mortgage Recasting?

Mortgage recasting is a method that allows you to reduce your monthly mortgage payment by making a large one-time payment toward your loan’s principal. Once that payment is applied, your lender recalculates the remaining balance over the original term of the loan, which lowers your monthly payment.

Unlike refinancing, a recast doesn’t change your interest rate or reset the term of your mortgage. Your rate stays exactly the same, and so does the loan length, but your payment becomes smaller because your remaining balance is reduced.

For instance, if you have a 30-year fixed mortgage and make a lump-sum payment of $50,000 toward the principal, your lender will adjust your payment schedule based on the lower balance. This means you’ll owe less interest over time and your monthly bill will drop.

In simple terms, if you come into extra money — perhaps through a work bonus, inheritance, or sale of another property — a mortgage recast can make your monthly payments more manageable without changing your existing loan terms.

How Does Mortgage Recasting Work?

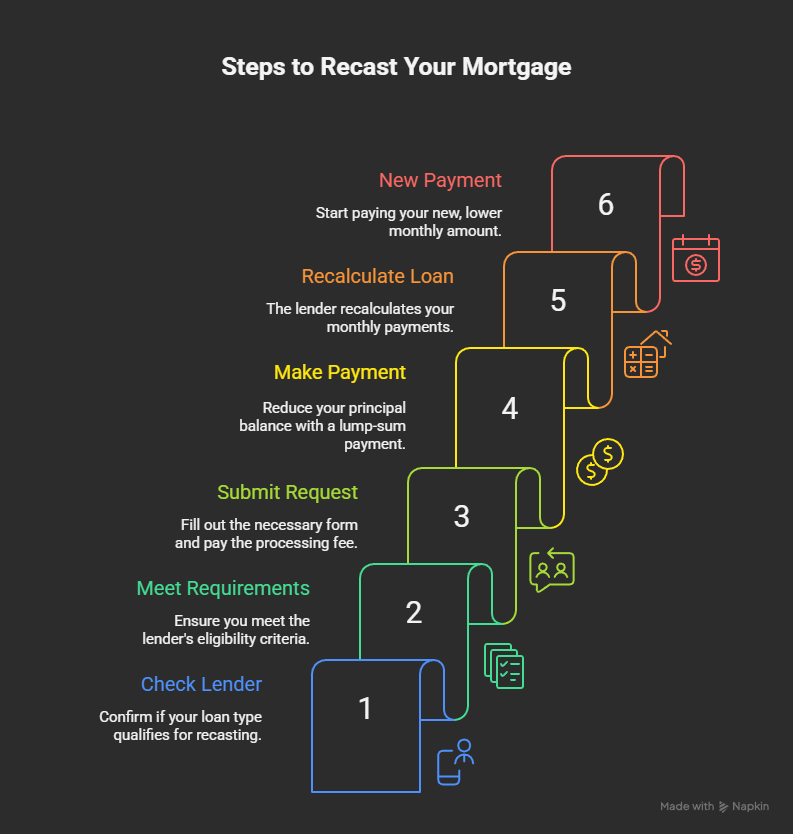

The process is straightforward and typically involves a few simple steps:

- Check with your lender: Not all lenders offer mortgage recasting, so the first step is confirming that your loan type qualifies. Most conventional loans are eligible, but government-backed loans like FHA or VA often are not.

- Meet eligibility requirements: Lenders generally require that you’ve made consistent, on-time payments and that you have a conventional loan. They may also set a minimum lump-sum payment — often between $5,000 and $10,000.

- Submit a recast request: Once you’re eligible, you’ll fill out a short form and pay a small processing fee.

- Make the lump-sum payment: The payment goes directly toward reducing your principal balance.

- Your loan is recalculated: The lender recalculates your monthly payments based on the new lower balance, keeping your same rate and remaining term.

- Start paying the new amount: Your new, lower monthly payment takes effect on your next billing cycle.

For example, if you owe $200,000 at 4.5% interest and pay $40,000 toward the balance, your payment will drop noticeably — saving you money on interest over time.

Who Should Consider Mortgage Recasting?

Mortgage recasting isn’t ideal for everyone, but it’s a strong choice in certain financial situations:

- You’ve recently received a lump sum from a bonus, inheritance, or property sale.

- You want to lower your monthly payment without changing your interest rate or extending your term.

- You already have a great rate and refinancing wouldn’t save you money.

- You’re preparing for a life change that might reduce your income, such as retirement or a career shift.

- You want to improve your debt-to-income ratio before applying for another loan.

If your goal is to keep your current mortgage terms while freeing up monthly cash flow, recasting is a practical option.

Advantages of Mortgage Recasting

- Lower monthly payments: Your monthly payment decreases because your remaining balance is smaller.

- Keep your existing interest rate: You’re not applying for a new loan, so you don’t risk losing your locked-in rate.

- Avoid heavy refinance costs: There’s no need for an appraisal, credit check, or closing costs.

- Save on total interest: A smaller balance means less interest paid over the life of the loan.

- Improve cash flow: Lower monthly payments can make budgeting easier and free up money for other goals.

Disadvantages to Consider

- Your cash becomes less accessible: Once you pay that lump sum, it’s tied up in your home equity and not available for emergencies or investments.

- No change to interest rate or term: If you want a shorter loan or lower rate, refinancing might be more effective.

- Not all loans qualify: Government-backed loans often can’t be recast.

- There’s still a small fee: Most lenders charge a modest administrative fee to process the recast.

If you simply pay a lump sum without officially recasting, your payment won’t change — you’ll just shorten your loan term instead.

Mortgage Recasting vs. Refinancing

While both reduce your monthly payment, they work differently:

| Feature | Recasting | Refinancing |

|---|---|---|

| Interest rate change | No | Yes |

| Loan term change | No | Yes |

| Monthly payment reduction | Yes | Yes |

| Paperwork & eligibility | Simple | Complex |

| Accessing equity | No | Yes |

| Best for | Lowering payment while keeping current rate | Lowering rate or changing term |

If your goal is simply to pay less each month, a recast works well. But if you want a new rate, shorter term, or cash-out equity, refinancing is the better path.

How to Decide if Recasting Is Right for You

To know if a recast fits your needs, consider these steps:

- Make sure your lender allows it and understand their requirements.

- Calculate how much you can comfortably pay toward principal without straining your finances.

- Compare your new projected monthly payment versus your current one.

- Consider alternative options like refinancing or just making extra payments.

- Keep your emergency fund intact — don’t drain your savings to recast.

- Think about opportunity cost — could your lump sum grow more if invested elsewhere?

If lowering your monthly payment fits your long-term goals and your lender supports recasting, it’s often a wise move.

Eligibility Requirements

Most lenders have similar requirements for mortgage recasting:

- Your loan must be a conventional type (not FHA, VA, or USDA).

- The loan should be current with no recent missed payments.

- You’ll need to make a minimum lump-sum payment (often $5,000–$10,000).

- The lender may require you to wait several months after closing before applying.

- A small service fee is usually charged to process the change.

Estimating Potential Savings

To estimate savings:

- Note your current loan balance, rate, and remaining term.

- Subtract your planned lump-sum payment from the balance.

- Recalculate the monthly payment using the same rate and term.

- The difference shows your monthly savings, which you can multiply by the number of months left on your loan to estimate long-term benefits.

For example, if your balance is $250,000 at 4.5% with 25 years left and you apply $50,000 toward the principal, your payment might drop by around $200 a month — totaling roughly $60,000 in reduced payments over the life of the loan.

When Mortgage Recasting May Not Be the Best Option

Recasting may not be ideal if:

- You want to change your interest rate or shorten your term.

- Current rates are much lower than your existing one.

- You have other high-interest debts that need attention first.

- You plan to move or sell the home soon.

- Your available lump sum is too small to make a noticeable difference.

In those cases, refinancing or simply making additional principal payments may yield better results.

Financial and Tax Considerations

Making a large payment reduces your loan balance and therefore the total amount of interest you pay, but it also means you’ll have slightly less mortgage interest to deduct if you itemize taxes.

On the bright side, a lower monthly payment can improve your cash flow, make budgeting easier, and potentially enhance your debt-to-income ratio — which could help with future loans or credit applications.

Real-Life Example

Imagine a homeowner named Sarah who owes $275,000 on her mortgage at a 4% fixed rate. She receives a $50,000 inheritance and decides to apply it toward her loan. Her lender approves the recast, recalculates her payments, and her monthly cost drops by about $200. Over time, she saves thousands in interest while keeping her same rate and loan term intact.

Common Questions About Mortgage Recasting

Can I recast my loan more than once?

Yes, many lenders allow multiple recasts, though each one may require a separate fee.

Does recasting affect my interest rate?

No. Your existing interest rate stays the same.

Can it shorten my loan term?

Not automatically, though you can pay more each month to finish sooner.

Are government loans eligible?

Usually not. FHA, VA, and USDA loans typically don’t allow recasting.

Will this impact my credit score?

There’s no hard credit inquiry, but the lower monthly payment can help your debt ratio.

Do I pay closing costs like with refinancing?

No, the fee is usually minimal — often just a few hundred dollars.

What if I sell soon after recasting?

If you sell too quickly, you might not recover the benefit of the lump-sum payment.

Can I recast with any lender?

No, your current lender must offer it; the option isn’t transferable.

Tips for Maximizing the Benefits

- Maintain a separate emergency fund before applying your lump sum.

- Wait until you meet all lender requirements before initiating the recast.

- Continue making extra principal payments after the recast if possible.

- Compare your potential savings against refinancing opportunities.

- Keep records of all communication and your new amortization schedule.

When You Should Avoid Mortgage Recasting

Avoid recasting if:

- You expect to move or refinance soon.

- You’re looking to access equity for other expenses.

- Your current interest rate is significantly higher than market rates.

- Your lump sum is too small to produce meaningful monthly savings.

Conclusion

Mortgage recasting is a smart, low-cost way to reduce monthly payments without altering your interest rate or loan term. It’s especially useful for homeowners who’ve received a lump sum and want immediate relief on monthly expenses.

However, it’s not a one-size-fits-all solution. Because your cash becomes locked into your home, it’s best for those who already have an emergency fund and long-term stability. Before deciding, speak with your lender, evaluate your options, and ensure the move supports your broader financial goals.