What Is a Consumer Statement on Your Credit Report? Better Financial Understanding

Introduction

Your credit report tells the story of your financial life — how you borrow, repay, and manage debt. But sometimes, numbers don’t tell the full story. Maybe you missed a payment because you lost your job, went through a health crisis, or faced identity theft. In those moments, a consumer statement can be your voice.

A consumer statement is a short explanation that you add to your credit report. It doesn’t change your credit score, but it helps others understand the circumstances behind certain items. Think of it as a note of context — a small paragraph that says, “Here’s what really happened.”

In this complete guide, we’ll cover what a consumer statement is, why it matters, when to use one, how to write it effectively, and how lenders interpret it in 2025. You’ll also find examples, a step-by-step process, FAQs, and professional tips for tenants, borrowers, and anyone working to rebuild credit.

What Is a Consumer Statement?

A consumer statement is a brief personal note that you can attach to your credit report. It allows you to explain information that appears in your file, especially if it’s negative or disputed.

For instance, if a late payment was caused by a temporary job loss, you can add a short message saying, “Payment delay due to unexpected job loss in March 2023. Account brought current in July 2023.”

Every major credit bureau — Experian, Equifax, and TransUnion — allows you to submit such a statement, either online or by mail.

While it doesn’t erase negative marks, it gives lenders context when they review your credit. This can make a difference in situations where human underwriters (like mortgage or rental applications) look beyond the score.

Why Add a Consumer Statement to Your Credit Report?

Adding a consumer statement isn’t always necessary — but in certain cases, it can be very helpful.

Here are the most common reasons why people add one:

1. To Explain a Temporary Financial Hardship

Maybe you faced a sudden layoff, illness, or family emergency that caused short-term financial strain. A statement shows that your late payment wasn’t due to negligence but an exceptional situation that’s now resolved.

This is especially useful for lenders who review reports manually, like mortgage officers or landlords.

2. To Clarify Identity Theft or Fraud

If your credit report shows accounts or charges that aren’t yours, and you’ve already disputed them, a consumer statement helps reinforce your position. You can note that the item was a result of identity theft and is under investigation or resolved.

3. To Show Responsibility and Transparency

Sometimes, just the act of explaining yourself can show lenders that you take credit seriously. A short, factual statement can demonstrate maturity, responsibility, and awareness — qualities that lenders appreciate.

4. To Provide Context for Closed or Settled Accounts

If you settled a debt, closed a credit card, or went through a temporary collection process, a statement can show that you took proactive steps to correct the issue. It tells lenders you’ve learned and recovered.

5. To Support Manual Underwriting

Some financial institutions still perform manual reviews, especially for large loans or rental agreements. In these cases, a consumer statement can add valuable human context that automated scoring systems can’t capture.

When You Should Avoid Adding a Consumer Statement

While a consumer statement can help, it’s not always the right move. Here are situations where adding one might backfire:

1. When You Have a Clean Credit History

If your credit report is positive and accurate, there’s no reason to add extra information. Doing so may draw unnecessary attention or raise questions.

2. When You Haven’t Disputed an Error Yet

If there’s an incorrect item on your report, don’t skip the dispute process. Always file a dispute with the credit bureau first. Only add a consumer statement if the dispute doesn’t fully resolve the issue or if you want to add context.

3. When the Issue Is Old or Resolved

If the event occurred years ago and your credit has long recovered, a statement could remind lenders of past problems rather than focusing on your progress.

4. When It Sounds Emotional or Defensive

A poorly written statement that sounds emotional, angry, or defensive can do more harm than good. Keep your tone factual, polite, and professional.

Legal Basis for Consumer Statements

Under the Fair Credit Reporting Act (FCRA), every U.S. consumer has the right to explain information on their credit report. This protection ensures you can add a statement of explanation for disputed or contextual items.

However, the law also states that your statement does not override the factual data. Negative marks remain visible — but your explanation is added alongside them.

Think of it as adding a “footnote” to your credit history. It won’t erase a late payment, but it tells future lenders why it happened.

How to Write an Effective Consumer Statement

Writing a consumer statement is an art. It needs to be short, factual, and clearly written. Most credit bureaus limit statements to about 100 words (or 475 characters).

Here’s how to make yours effective:

1. Be Clear and Direct

Avoid long sentences or emotional language. Write like you’re explaining facts to a stranger.

Example: “Late payment in June 2023 due to temporary job loss. Account has been paid in full and all subsequent payments are current.”

2. Take Responsibility, Don’t Shift Blame

It’s okay to explain the reason, but never sound like you’re making excuses.

Example: Instead of saying “The bank made an error,” say “There was a delay in payment processing that has since been resolved.”

3. Include Relevant Dates

If you reference a specific event, mention when it occurred. This shows accuracy and professionalism.

4. End on a Positive Note

Mention what you’ve done since the issue occurred. Example: “I’ve maintained on-time payments for 18 months since this event.”

5. Keep It Professional

Avoid emotional wording or unnecessary detail. Treat it like a short business letter, not a personal story.

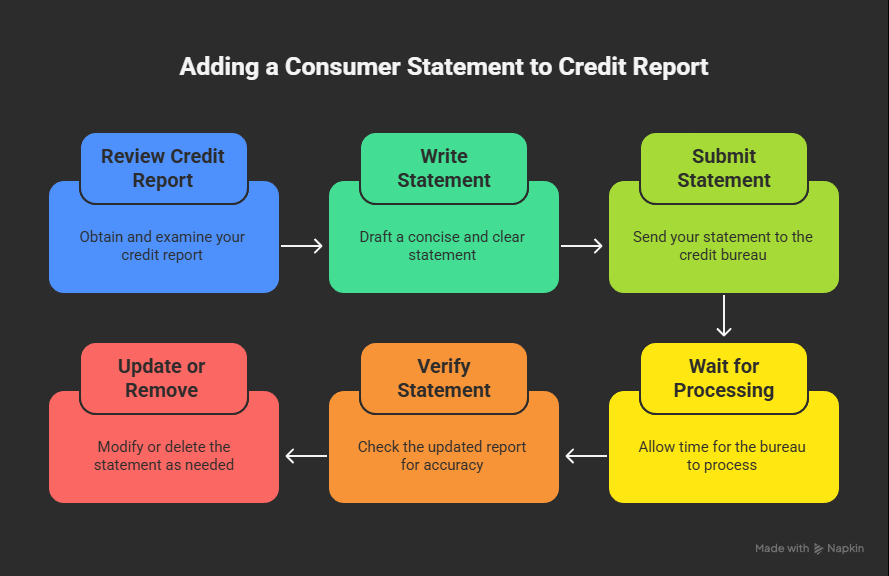

Step-by-Step: How to Add a Consumer Statement

Follow these simple steps to add your statement to your credit report:

- Review Your Credit Report

Get a free copy from AnnualCreditReport.com or directly from each bureau. Identify which account or event you want to explain. - Write Your Statement

Keep it short and clear — under 100 words. Double-check spelling and tone. - Submit Your Statement

Each credit bureau allows you to submit online or by mail. You’ll need your full name, address, report number (if available), and your statement text. - Wait for Processing

The bureau will confirm receipt and notify you once your statement is added. This usually takes 30–60 days. - Verify It Appears Correctly

Once updated, pull your report again to ensure the statement appears exactly as you wrote it. - Update or Remove It Later

You can request removal anytime — especially once the issue becomes irrelevant.

How Lenders Interpret Consumer Statements in 2025

Credit scoring systems (like FICO or VantageScore) ignore consumer statements because they focus on numerical data. However, human underwriters do read them.

1. In Mortgage Applications

Mortgage lenders often review credit reports manually. A short, honest consumer statement can help them understand a temporary hardship and view you more favorably.

2. In Car Loans or Personal Loans

For most automated loan decisions, the statement won’t make a difference. But in borderline cases, it can provide enough reassurance to push approval forward.

3. In Rental Applications

Landlords and property managers often read consumer statements carefully. Explaining one or two past late payments due to valid reasons can help you secure a lease.

4. In Employment Screenings

If a job requires credit checks, a professional statement can show accountability and transparency — key traits employers value.

Pros and Cons of Adding a Consumer Statement

Pros

- Gives you a voice in your credit profile.

- Adds valuable context for lenders.

- Free to add or remove.

- Useful during major applications (mortgage, rental, business loans).

Cons

- Doesn’t improve your credit score.

- May highlight negative events unnecessarily.

- If poorly written, it can appear unprofessional.

- Some lenders ignore it completely.

Examples of Good Consumer Statements

Here are a few templates you can adapt:

Example 1:

“Late payment in April 2023 due to temporary job loss during company downsizing. Account brought current in June 2023 and remains in good standing.”

Example 2:

“Account listed in dispute. Charges resulted from identity theft reported to the police in July 2022. Issue resolved and account closed.”

Example 3:

“Medical emergency in early 2021 led to temporary missed payments. Since recovery, all accounts have been paid on time for 24 consecutive months.”

Best Practices for Maintaining a Healthy Credit Report

- Pay on Time, Every Time

Payment history is the single biggest factor in your score. - Keep Credit Utilization Low

Try to use less than 30% of your available credit. - Monitor Your Reports Regularly

Review for errors or unauthorized accounts. - Limit New Credit Inquiries

Too many new accounts can temporarily lower your score. - Use Tools Like Rent Reporting

Reporting your rent through services like AxcessRent can help build positive history over time. - Update or Remove Old Statements

Once your situation improves, consider deleting your consumer statement to keep your report clean.

Conclusion

A consumer statement is your opportunity to add humanity to your credit report. It’s your voice in a system that’s often dominated by numbers and algorithms. While it doesn’t directly boost your credit score, it can influence how lenders and decision-makers perceive your profile.

Used wisely, a consumer statement demonstrates transparency, responsibility, and growth. It says, “I faced a challenge — and I overcame it.”

If you’ve ever had a temporary setback, adding a clear, professional statement can help ensure that your story is told accurately — and that your financial journey reflects not just your mistakes, but your recovery and resilience.

Frequently Asked Questions

1. Does a consumer statement affect my credit score?

No. It doesn’t change your score — it only adds an explanatory note to your file.

2. How long does it stay on my credit report?

Typically, a general statement remains for about two years or until you remove it.

3. Can I edit or remove my statement later?

Yes. You can update or delete it anytime by contacting the credit bureau.

4. Should I add one for every issue?

Only when it adds genuine value. Don’t clutter your report with unnecessary notes.

5. Can lenders ignore my statement?

Yes — some automated systems skip it. But human reviewers, like mortgage underwriters or landlords, often read them carefully.