How to remove derogatory items from credit report

Derogatory items can tank your credit score. They show up as late payments or collections. Lenders see them and charge higher rates. Or deny loans. But you have options. Not all negatives stay forever. Inaccurate ones must go. Even accurate ones can sometimes vanish with effort. This guide shows how. We cover spotting issues, disputing errors, and more. By the end, Step-by-step guide to remove derogatory items like late payments and collections from your credit report. Start with free reports from Equifax, Experian, and TransUnion. Act now for better credit.

What Are Derogatory Items on a Credit Report?

Derogatory items are negative marks. They signal risk to lenders. Bureaus add them from reports by banks or collectors. Your report lists them in the accounts or public records section.

These marks hurt more than positives. A single late payment drops your score 100 points. Collections can cut it further. Most stay 7 years. But rules vary by type.

Common Types of Derogatory Items

- Late payments: Missed due dates on cards or loans. They show as 30, 60, or 90 days late.

- Collections: Unpaid debts sent to agencies. Like old medical bills.

- Charge-offs: When lenders write off debt as loss. Often after 180 days late.

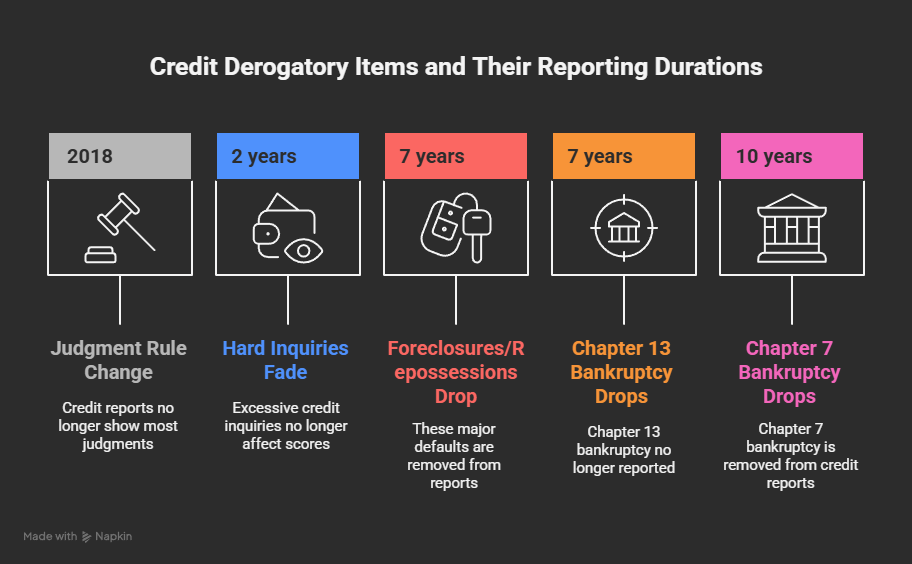

- Bankruptcies: Chapter 7 or 13 filings. Chapter 7 lasts 10 years. Chapter 13 lasts 7.

- Foreclosures or repossessions: Lost home or car from nonpayment. Stay 7 years.

- Judgments: Court orders for unpaid debt. Now rare on reports since 2018 rules.

- Hard inquiries: Too many in a row. But they fade in 2 years.

Each type has a clock. It starts from the first delinquency date. Not payment date.

| Derogatory Item | Typical Duration | Starts From |

|---|---|---|

| Late Payments | 7 years | First missed payment |

| Collections | 7 years | Original delinquency |

| Charge-Offs | 7 years | Delinquency date |

| Chapter 7 Bankruptcy | 10 years | Filing date |

| Chapter 13 Bankruptcy | 7 years | Filing date |

| Foreclosure | 7 years | Completion date |

This table helps track timelines. Use it to note dates on your report.

Why Bother Removing Derogatory Items?

Negatives drag scores down. FICO weights payment history at 35%. Amounts owed at 30%. Old marks still sting. A 7-year-old collection hurts less than a new one. But it blocks prime loans.

Removal opens doors. Lower rates on mortgages. Easier rentals. Better job chances in finance. One study shows clean reports save $1,000 yearly on interest.

Plus, fraud happens. Thieves add fake debts. Spot them early. Disputes fix that free.

In 2025, new rules help. Medical debts under $500 vanish. Others wait 1 year to report. But other negatives stick without action.

Your Legal Rights to Challenge Derogatory Items

- The Fair Credit Reporting Act (FCRA) protects you. It says bureaus must report accurate info. Inaccurate or old items? They remove them.

- You can dispute any item. Free. Bureaus investigate in 30 days. Can’t verify? It goes. Furnishers (like banks) must check too.

- Direct disputes to furnishers work. They report to all bureaus. FCRA requires notice of disputes on future reports.

- States add rights. Like California limits medical debt reports. Check your state’s AG site.

- No fee for disputes. Online, mail, or phone. Keep records. Results come by mail.

Step 1: Get Your Free Credit Reports to Spot Issues

- Start here. Pull reports from all three bureaus. Differences exist. One might miss a mark.

- Go to AnnualCreditReport.com. Free weekly in 2025. Enter name, SSN, address. Answer questions. Download PDFs.

- Direct sites: Equifax.com, Experian.com, TransUnion.com. Free monthly each.

- Review sections: Personal info, accounts, inquiries, public records. Highlight negatives.

- Take notes. Item, date, balance, status. Compare across reports.

Time: 30 minutes. Do it quarterly. Set reminders.

Step 2: Identify Which Items to Target

Not all marks qualify for removal. Accurate and current? They stay.

Look for:

- Errors: Wrong dates, amounts, accounts not yours.

- Outdated: Over 7 years old (10 for bankruptcies).

- Unverifiable: No proof from furnisher.

- Fraud: ID theft signs, like unknown addresses.

Examples: A collection from 2015 should drop in 2022. If still there, dispute.

- Paid collections: Mark as paid, but negative stays unless negotiated.

- Score impact: Use free tools like Credit Karma to see before/after estimates.

Step 3: Dispute Inaccurate Derogatory Items

Disputes work for errors. 1 in 5 reports has mistakes. Many lead to removals.

How to File a Credit Report Dispute

- Gather evidence: Statements, payment proofs, ID.

- Write a letter or use online form. Include name, address, account numbers, errors explained.

- Send to bureau(s) showing the item. And furnisher.

Online portals: Equifax disputes page. Experian dispute center. TransUnion online form.

Mail: Addresses on reports. Certified mail for proof.

Phone: Quick, but follow up in writing.

[Address Line 2]

[City, State ZIP]

[Address Line 1]

[Address Line 2]

[City, State ZIP]

Re: Dispute of Inaccurate Information

Account # [Number]

Dear Sir or Madam,

I dispute the following: [Describe item, e.g., “Collection from ABC Debt, $500, dated 01/01/2020”]. It’s inaccurate because [reason, e.g., “I paid it on 12/15/2019”].

Enclosed are copies of supporting documents for your review and verification. Please investigate this matter and remove the inaccurate information from my credit report.

Enclosed:

- [Proof 1 — e.g., payment receipt]

- [Proof 2 — e.g., bank statement showing payment]

- [Proof 3 — e.g., correspondence with creditor]

Sincerely,

[Your Name]

What Happens After You Submit a Dispute?

- Bureau sends to furnisher. They verify in 30 days. You get results. If deleted, updated report free.

- If denied, add a 100-word statement to your file. Lenders see it.

- Track multiple disputes. Space them. Re-dispute if new info appears.

- Success rate: Up to 40% for errors. Patience pays.

Using Goodwill Letters to Remove Accurate Late Payments

For true lates, try goodwill. Ask the creditor nicely. No legal right, but they might remove as courtesy.

Best for one-time slips. Like job loss. Long-time customers.

How to Write an Effective Goodwill Letter

Keep it short. One page. Explain situation. Show loyalty. Promise better habits.

[Address Line 2]

[City, State ZIP]

[Address Line 1]

[Address Line 2]

[City, State ZIP]

Re: Goodwill Request for Account [Number]

Dear [Customer Service],

I value our [X years] relationship. On [date], I missed a payment due to [brief reason, e.g., “unexpected medical costs”]. Since then, I have consistently made on-time payments and maintained good standing.

As a gesture of goodwill, I kindly request the removal of this late payment record from my credit report. This adjustment would greatly support my credit goals, including [goal, e.g., “purchasing a home”].

Thank you for your time and understanding. I appreciate your consideration and continued partnership.

Sincerely,

[Your Name]

Send certified. Follow up in 30 days. Success: 20-30% for polite requests.

Negotiating Pay-for-Delete for Collections

For old collections, offer payment for removal. Called pay-for-delete.

Legal gray area. Not banned, but bureaus frown on it. Creditors might agree if debt is small.

Steps for a Pay-for-Delete Agreement

- Verify debt: Call collector. Get validation letter.

- Offer partial or full payment for deletion.

- Get written agreement before paying. “We will request deletion from all bureaus.”

- Pay. Then dispute if not removed.

Sample letter:

[Address Line 2]

[City, State ZIP]

[Address Line 1]

[Address Line 2]

[City, State ZIP]

Re: Pay-for-Delete for Account [Number]

I am writing to offer a settlement on the above-referenced account. I propose a payment of $[amount] to settle the outstanding balance of $[original].

In exchange for this payment, I request that you agree to remove the related tradeline from all of my credit reports with the major credit bureaus.

Please confirm this agreement in writing on your official letterhead before I submit the payment.

Sincerely,

[Your Name]

Risk: They take money, don’t delete. Use for legit debts only. In 2025, still viable but rare.

Waiting for Derogatory Items to Age Off Naturally

- Some marks self-remove. No action needed.

- Most negatives: 7 years from delinquency. Track dates. Use apps like Mint.

- Bankruptcies: 10/7 years from filing.

- If past due, dispute as obsolete. Bureaus must drop.

Tip: Positive history dilutes old marks. Build now.

When to Hire Professional Help for Credit Repair

DIY fails? Consider services. They dispute in bulk. Track progress.

- Legit ones: Lexington Law, Credit Saint. Fees $50-150/month.

- Avoid scams. No guarantees. FTC warns of upfront fees.

- Pros: Time-saving. Higher success for complex cases.

- Cons: Costly. You can do most free.

- Check reviews. Use NACA directory.

- Case: John had 5 collections. Service disputed 3. Score up 150 points in 6 months.

Rebuilding Your Credit After Removing Derogatory Items

Removals help. But build habits.

- Pay on time. Automate bills.

- Keep utilization under 30%. Pay down debt.

- Add positives: Secured cards, credit-builder loans.

- Monitor monthly. Free apps.

Scores rise 50-100 points in a year.

Goal: 670+ for good rates.

Conclusion

Removing derogatory items from your credit report is not quick. It takes time and effort. But the payoff is big. A cleaner report means lower interest on loans. Easier approvals for homes or cars. Even better job options in some fields. Start with disputes for errors. They fix the easy wins. Then try goodwill letters for late payments. Or pay-for-delete deals on old collections. For the rest, just wait them out. They drop after 7 or 10 years. Use your FCRA rights every step. Check your reports at least quarterly. Pull them free from AnnualCreditReport.com.

Once items are gone, focus on building back. Pay all bills on time. That’s the top factor in your score. Keep credit card balances under 30% of your limit. Add new positive accounts, like a secured card. Track changes with free tools from Credit Karma or your bank. In 2025, scores can jump 50 to 100 points in six months if you stay steady. Don’t fall back into old habits. Set up auto-payments. Cut up extra cards if needed.

Here’s a quick checklist to wrap up:

- Pull all three reports today.

- Spot errors and dispute them online.

- Send a goodwill letter to one creditor this week.

- Negotiate with any active collector.

- Set calendar alerts for report checks.

- Start one new good habit, like timely payments.

Your credit history is a record of past choices. But it does not lock your future. You control the next pages. Take one step now. Pull your report. Dispute what you find. In a few months, you’ll see the difference. Better rates. Less stress. More options. If stuck, talk to a non-profit credit counselor. They help for free. Keep going. Financial freedom starts with small fixes.

Frequently Asked Questions

Can I remove accurate derogatory items?

You can’t force removal if the bureau verifies it’s correct. But try a goodwill letter to the creditor asking nicely. Or negotiate pay-for-delete with collectors. These work sometimes, about 20-30% of cases.

How long does a dispute take?

Bureaus have 30 days to investigate under FCRA. They contact the creditor for proof. You get a free updated report after. If no response, the item drops. Track it online or by mail.

Is pay-for-delete legal in 2025?

Yes, it’s legal to negotiate. No law bans it. But creditors aren’t required to agree, and bureaus may not honor deletions. Get everything in writing first. It’s a gray area, so use for old debts only.

What if my dispute is denied?

You can add a short statement to your report explaining your side—up to 100 words. Lenders see it. If the error was willful, sue under FCRA for damages. Consult a lawyer for that.

Do credit repair companies work?

Some help with disputes and tracking, especially complex cases. They charge $50-150 monthly. But you can do most free yourself via bureau sites. Start there to save money. Check reviews before hiring.