How to Pay Off Credit Card Debt: Step-by-Step Guide That Actually Works

Credit card debt feels heavy. High interest rates, late fees, and minimum payments trap millions of people in a cycle that looks impossible to escape. If you struggle with multiple balances or feel like your payments never make progress, you are not alone. According to consumer finance reports, credit card debt is one of the fastest-growing types of debt in the U.S., and most households pay thousands of dollars in interest every year.

The good news? You can break free. Once you understand how to pay off credit card debt step by step, the path becomes clear. Whether your priority is saving the most money, paying off balances quickly, or staying motivated with small wins, there is a method designed for you.

This guide breaks down proven strategies like the avalanche method, the snowball method, balance transfers, debt consolidation, and lifestyle adjustments that speed up repayment. Each section explains why the method works, who it fits best, and how to apply it with real examples.

By the end, you will know exactly how to choose a strategy that matches your financial situation and start eliminating debt with confidence.

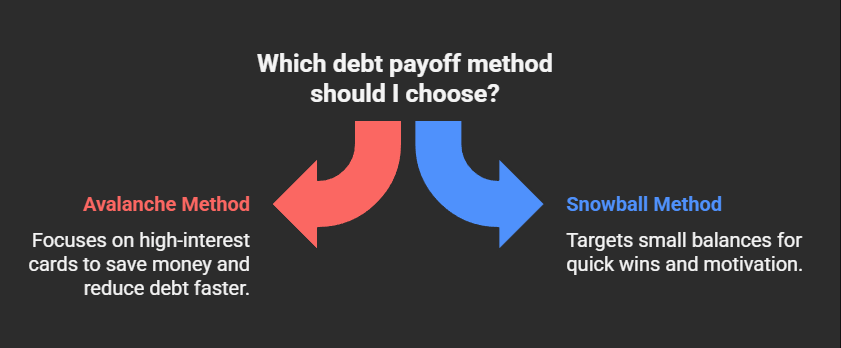

1. Choose a Payoff Method That Matches Your Style

You control how to attack the balance. Two of the most popular strategies are the avalanche method and the snowball method.

High-Rate (Avalanche) Method

This strategy focuses on the credit card with the highest interest rate first. You continue making minimum payments on all cards to stay current, but you direct every extra dollar toward the balance with the steepest APR.

Why it works:

- You save the most money on interest over time.

- Your debt shrinks faster because less of your payment gets eaten up by interest charges.

- It is a logical, math-driven approach for long-term savings.

Example:

You have three credit cards:

- Card A: $2,000 at 24% APR

- Card B: $1,000 at 19% APR

- Card C: $500 at 15% APR

With the avalanche method, you focus on Card A first because it carries the highest rate. You pay the minimums on Cards B and C, while directing all extra money toward Card A.

Once Card A is eliminated, you roll that freed-up payment amount onto Card B. Finally, after Card B is gone, you tackle Card C.

By sticking to this method, you minimize total interest paid and shorten the repayment timeline, even though progress may feel slower at the start compared to other methods.

Snowball Method

The snowball method targets the smallest credit card balance first. You pay the minimum required amount on all cards but direct any extra cash toward the card with the lowest balance.

Why it works:

- Small victories keep motivation high.

- Eliminating a balance quickly creates momentum and confidence.

- The sense of progress reduces stress and encourages discipline.

Example:

Using the same cards above:

- Card C: $500 at 15% APR

- Card B: $1,000 at 19% APR

- Card A: $2,000 at 24% APR

With the snowball method, you pay off Card C ($500) first, then move on to Card B ($1,000), and finally clear Card A ($2,000). This approach costs more in interest compared to the avalanche method, but the consistent wins fuel determination and help you stay committed until the last card is paid off.

2. How Debt Consolidation Works

Debt consolidation combines multiple balances into one payment. This can happen with a personal loan or a balance transfer card. The goal is to secure a lower interest rate and simplify your repayment.

Benefits:

- One payment instead of juggling several.

- Lower interest saves money long term.

- A fixed payoff timeline creates structure and accountability.

Example:

You owe $5,000 across three cards at 22% APR. You qualify for a personal loan at 11% APR. That cut in half saves thousands over the loan’s life and makes repayment more predictable.

3. Free Up Money to Pay Off Debt Faster

Paying off credit card debt requires extra cash flow. Even small changes free up dollars for debt payoff.

Ideas to free up money:

- Cancel unused subscriptions.

- Cook at home instead of eating out.

- Sell items you no longer use.

- Use tax refunds or work bonuses for lump-sum payments.

- Track expenses daily to catch wasteful spending.

Example:

An extra $100 per month on a $5,000 balance at 20% APR cuts the timeline by more than a year and saves over $1,000 in interest.

4. Transfer the Balance to a New Card

Many banks offer 0% APR for balance transfers. You move an existing balance to the new card and pay no interest during the promotional period.

Key details:

- Most cards charge a 3–5% transfer fee.

- Promotional periods last 12–21 months.

- You must pay the balance in full before the promo ends, or the rate jumps.

Example:

You transfer $4,000 to a 0% APR card for 18 months. To clear it in time, you must pay at least $223 per month.

5. Negotiate a Lower Interest Rate

Credit card companies want to keep customers. If you have a history of on-time payments and a fair credit score, they may agree to lower your APR.

Example script:

“Hello, I have been a loyal customer for years. I pay on time, but my balance feels overwhelming because of the high rate. Can you lower my APR so I can stay on track?”

Even a 3% reduction in APR saves hundreds of dollars over time.

6. What to Do If You Cannot Pay Credit Card Bills

Falling behind feels stressful, but you still have options.

Steps to take:

- Call your lender and request hardship assistance.

- Ask for reduced minimum payments or a temporary pause.

- Explore nonprofit credit counseling services.

- Focus on essentials first: rent, food, and utilities.

Never ignore the problem. Missed payments damage your credit and lead to collection calls.

7. Final Thoughts: Build Momentum and Stay Consistent

Paying off credit card debt takes patience, discipline, and commitment — but with the right approach, real results follow.

The avalanche method helps you save the most money on interest, while the snowball method creates quick wins that build motivation. Debt consolidation provides structure and simplifies payments, and negotiation can lower your overall costs. Adding extra payments along the way accelerates your journey to financial freedom.

Every payment you make is progress. Every small win is proof that you can stay in control. Over time, these steps not only eliminate debt but also reduce stress and increase confidence in your financial future.

The ultimate goal is more than just paying off credit card debt — it’s about building long-term habits that keep you debt-free for life. Stay consistent, stay focused, and remember: freedom from debt is not just possible, it’s within your reach.

FAQs About Paying Off Credit Cards

How do I avoid getting into credit card debt again?

Use cards only for purchases you can pay in full every month. Track your spending and build an emergency fund for surprises.

Should I close credit cards after paying them off?

Not always. Closing reduces your available credit, which increases utilization ratio and may hurt your score. Keep accounts open unless they carry high annual fees.

Can I use other credit cards to pay off debt?

No. You cannot directly pay one card with another. Balance transfers or personal loans are the safe alternatives.

What should I do if I cannot pay my credit card bill?

Call your lender right away. Many offer hardship programs or temporary adjustments. Ignoring bills makes things worse.

Are credit counselors worth it?

Yes, if you use a trusted nonprofit. Credit counselors negotiate lower interest and set up debt management plans that help you stay accountable.

How much debt is too much?

Debt becomes excessive when you cannot pay more than the minimum or when your utilization rises above 30%. Lenders see you as risky at that level.