How Does Medical Collection Debt Affect Your Credit Score?

Medical debt feels different from other types of debt. Nobody plans to get sick or end up in the hospital, yet a single trip to the emergency room can leave you with thousands of dollars in bills. According to the Peterson Center on Healthcare and the Kaiser Family Foundation (KFF), more than 3 million people in the United States owe over $10,000 in medical debt. Millions more carry balances of a few hundred dollars.

This raises an important question: how does medical debt affect your credit score? The answer depends on the size of the debt, the status of the account, and how fast you respond. Let’s break it down in detail.

Do medical bills affect your credit score?

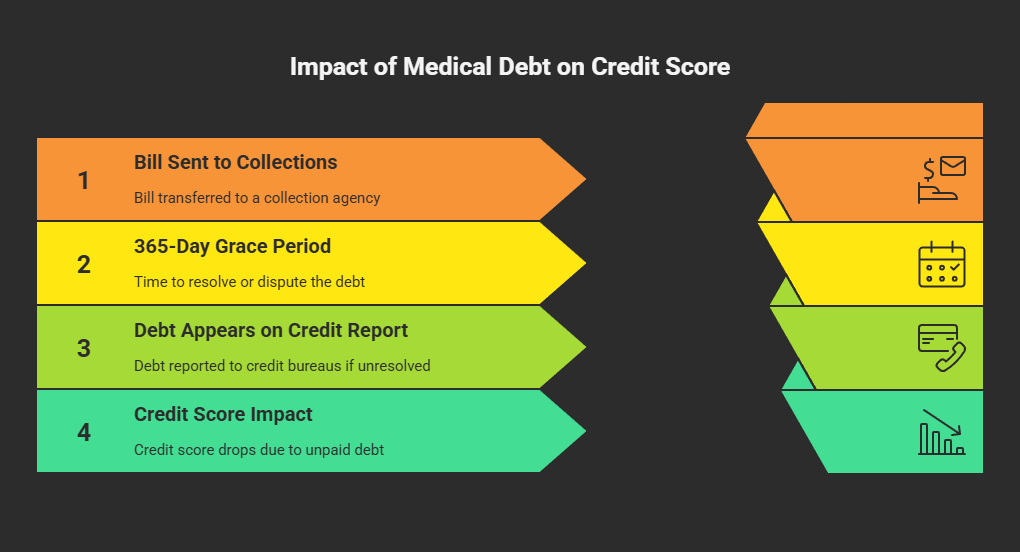

Medical bills do not affect your credit report as long as they stay unpaid directly with the hospital or clinic. Health care providers do not send account information to credit bureaus. Instead, the bill needs to go to a collection agency before it shows up on your credit report.

That process takes time. Providers usually wait 60, 90, or even 120 days before they sell an unpaid balance to a collection company. The exact timing depends on the hospital’s or clinic’s policy.

Even after a debt goes to collections, the credit bureaus—Experian, Equifax, and TransUnion—do not report it right away. They allow a 365-day grace period. This window gives you time to settle disputes with your insurance, correct billing errors, or work out a payment plan. If you clear the debt within that year, it never appears on your report.

Another major change came in March 2023. The three bureaus announced that they would no longer include medical collections under $500 on consumer credit reports. That means if the original balance is less than $500, it does not hurt your score even if it goes unpaid.

Paid medical collections also no longer appear. So if you or your insurance pay off the account, it disappears completely.

How Medical Debt Can Lower a Credit Score

Unpaid medical debt above $500 creates real problems. Once the account shows up on your credit report, it acts like any other collection account. That means:

- Your score can drop significantly, especially if you have a thin credit history.

- A collection account signals to lenders that you failed to meet an obligation.

- Even a single unpaid medical account can make it harder to qualify for loans or credit cards.

A collection account stays on your report for seven years from the date of delinquency. The good news: once the balance is paid, the bureaus now remove the account, which can immediately boost your score.

Can Medical Bills Be Removed From a Credit Report?

Yes. If you find a medical collection on your report that does not belong to you or that shows incorrect information, you can dispute it. Mistakes are common because medical billing systems often miscode procedures or fail to process insurance payments correctly. Identity theft also creates fraudulent accounts under your name.

To file a dispute, contact each bureau where the collection appears. You can do this online or by mail. Provide evidence such as:

- Statements from your insurance company

- Records from the provider

- Copies of checks or credit card statements that prove payment

If the dispute resolves in your favor, the collection gets updated or removed. Disputes cost nothing, but they require patience. You must follow up with the collection agency, the provider, and the bureaus.

Does Paying Off Medical Collections Improve Credit?

Yes, and in a big way. In the past, paid collections used to stay on your report for seven years. That changed in July 2022, when the three bureaus updated their policies. Now, once you pay off a medical collection, the account disappears.

For example, if you had a $2,000 hospital bill that went to collections and later you paid it or insurance covered it, the entire account gets deleted. This update can raise your score quickly, sometimes by dozens of points.

So if you have medical collections above $500, it is always better to pay them off or negotiate a settlement. Even a partial payment arrangement can lead to removal if the provider reports the account as settled in full.

What to Do if You Cannot Pay Medical Bills

Large medical bills overwhelm many households. If you face a balance you cannot cover, you still have options:

1. Negotiate a Lower Balance

Hospitals and clinics often accept a reduced payment if you can pay a lump sum. Some offer 20%–50% discounts for upfront payments. Others create hardship programs for low-income patients.

2. Request a Payment Plan

Many providers set up installment plans. They break the total into monthly payments with little or no interest. This option allows you to avoid collections without draining your savings.

3. Hire a Medical Billing Advocate

Advocates specialize in medical billing systems and insurance rules. They contact providers and insurers on your behalf, often uncovering errors or overcharges. Although they charge fees, the savings often exceed the cost.

4. Apply for Financial Assistance

Nonprofits, religious organizations, and government programs provide aid for medical bills. Medicaid covers costs for low-income families, while hospitals sometimes offer charity care programs. Always ask the provider about available assistance.

5. Use Credit With Caution

A personal loan or credit card may cover an urgent bill, but this option carries risk. Interest charges increase the cost. Avoid loans secured by your home or car because default could lead to losing the asset. If you use a card, look for a 0% APR introductory offer and plan to clear the balance before the rate increases.

How to Keep Your Credit Score Healthy After Medical Debt

Even if a collection appears on your report, you can still rebuild your score. Focus on the following steps:

- Pay all bills on time, including utilities and credit cards.

- Keep credit card balances low relative to your limits.

- Limit new credit applications unless necessary.

- Monitor your reports for errors or fraudulent activity.

- Use free credit monitoring tools to track your progress.

You can pull one free report each year from each bureau through AnnualCreditReport.com. Check for any incorrect medical collections, verify that paid accounts are removed, and watch your progress as you rebuild.

Conclusions

Medical debt does not act like typical debt. Health providers rarely report accounts directly, and the credit bureaus give you a full year before a collection appears. Collections under $500 no longer show up, and once you pay off a larger balance, it disappears completely.

Still, unpaid balances above $500 can drop your score by dozens of points and linger for seven years if left unresolved. Quick action matters most: review bills immediately, fight errors, work with your provider, and set up a plan before the account goes to collections.

Your health comes first, but your financial health also matters. With the right steps, you can protect your credit, lower stress, and keep doors open for future loans or housing opportunities.