10 ways to Improve your Credit Score Quickly

Improve your Credit Score feels like a challenge, but it matters more than most people realize. Your credit score works like a grade that follows you everywhere. It decides whether a bank trusts you with a loan, if a landlord approves your apartment application, or if you qualify for a credit card with rewards. A high score makes life smoother, while a low score blocks opportunities and raises costs.

The good news? A low score does not have to stay low forever. You can take smart steps right now that move your score up faster than you think. This is not about waiting ten years or paying a costly credit repair company. It is about real actions you control today. Let’s dive into them step by step.

What a Credit Score Really Means

A credit score shows how responsible you look with money. Lenders use it as a shortcut to decide if you pay back what you borrow. It ranges from 300 to 850, and every point matters.

- Excellent (750–850): You look like the dream customer. Banks fight to give you loans with the lowest interest rates.

- Good (700–749): You qualify for most loans, though rates may not be the absolute lowest.

- Fair (640–699): You can still get approved, but lenders may charge higher interest or limit your options.

- Poor (300–639): Many lenders reject applications, and those who approve usually attach tough terms.

If you sit in the fair or poor range, raising your score even by 50 points changes everything. A car loan that costs you $400 per month today may drop to $340 with a better score. That is real money back in your pocket.

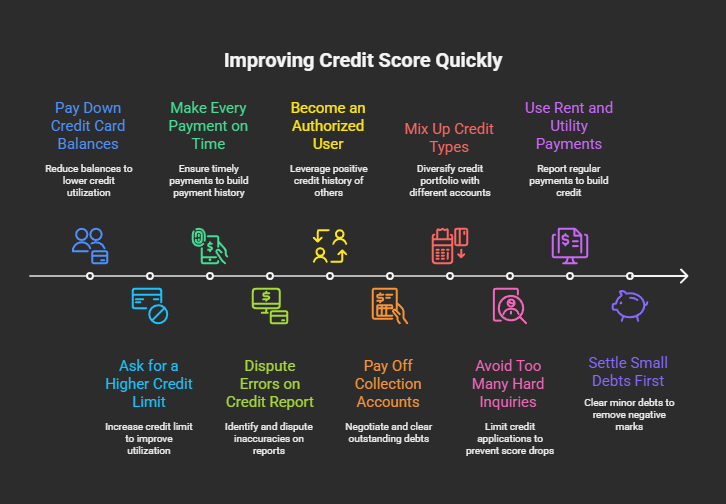

1. Pay Down Credit Card Balances Right Away

The quickest way to improve your credit score is by lowering balances on credit cards. Credit utilization—the percentage of available credit you use—makes up about 30% of your score.

Imagine you have a credit card with a $5,000 limit and a $4,000 balance. That means you use 80% of your credit line. To a lender, that looks risky. You may pay bills, but you sit close to maxed out. Now picture paying that balance down to $1,000. Suddenly, your utilization drops to 20%. This one action alone often boosts scores within a month.

Many people think you must clear the balance completely. Not true. Even reducing it by a few thousand changes your utilization and helps your score. If you have several cards, target the ones closest to their limit first.

Golden rule: Keep utilization under 30% if possible, and under 10% if you want the best results.

2. Ask for a Higher Credit Limit

Not everyone can pay large balances overnight. Here is another quick move: ask for a credit limit increase. If your limit jumps from $5,000 to $8,000 while your balance stays at $4,000, your utilization falls from 80% to 50% instantly. No payment required.

Most banks approve limit increases if you have a steady job, decent history, or a track record of paying on time. You can request it through your bank’s app or by calling customer service. The process takes a few minutes.

But remember: a higher limit only helps if you do not use it as permission to spend more. Use the new space to look less risky, not to rack up more debt.

3. Make Every Payment on Time

Payment history carries the heaviest weight in your score—35%. Even one missed payment leaves a mark that lasts years. The flip side: a streak of on-time payments pushes your score up month after month.

Set yourself up for success. Link bills to automatic payments. Use reminders on your phone. Some people pay the same day the bill arrives instead of waiting until the due date. That habit removes the chance of forgetting.

Think of it like this: each on-time payment is a brick in a wall of trust. The more bricks you stack, the stronger the wall looks to lenders.

4. Dispute Errors on Your Credit Report

One overlooked way to improve credit quickly is checking for mistakes. Studies show about 20% of reports contain errors that drag down scores unfairly. You may have an old account listed as unpaid even though you cleared it, or a late payment reported twice.

Go to AnnualCreditReport and grab free reports from Experian, Equifax, and TransUnion. Review every account line by line. Circle anything that feels off. Then file a dispute online with the bureau. By law, they must investigate within 30 days. If they confirm the error, they remove it. That single fix may add dozens of points to your score overnight.

5. Become an Authorized User

If you have a trusted family member or close friend with excellent credit, ask them to add you as an authorized user on their card. This does not mean you use the card. It means their positive history—years of on-time payments and low balances—appears on your report as well.

The result feels like an instant head start. If they have a card open for 10 years, your credit history suddenly looks longer and stronger. Just confirm that the issuer reports authorized users to all three bureaus, since not every card does.

6. Pay Off Collection Accounts

Collection accounts weigh your score down heavily. If you owe money to a collection agency, negotiate. Some agencies agree to remove the account completely if you pay—this is called “pay for delete.” Others at least update the account to “paid,” which looks far better than “unpaid.”

Even a small collection, like $200 from a forgotten phone bill, hurts more than people realize. Clearing it clears the path for your score to climb.

7. Mix Up Your Credit Types

Credit scores improve when you show variety. If you only have one type of account, like credit cards, your score does not reflect your ability to handle different forms of debt.

A healthy mix includes:

- Revolving credit like credit cards

- Installment loans like auto loans or student loans

- Long-term debt like mortgages

If you cannot qualify for a new loan, consider a secured credit card. You put down a deposit, and the bank reports your usage just like a normal card. Over time, this adds depth to your file.

8. Avoid Too Many Hard Inquiries

Each time you apply for credit, lenders run a hard inquiry on your report. A few inquiries spread out does not matter. But many in a short time makes you look desperate. Each one can shave a few points off your score.

Instead, use pre-qualification tools. Many banks and credit card companies let you check if you qualify with only a soft inquiry. Soft checks do not hurt your score. Use those first before sending full applications.

9. Use Rent and Utility Payments to Your Advantage

Most people pay rent, internet, and phone bills every month, but those payments do not usually help credit scores. That changes with services like Experian Boost or rent reporting programs.

Imagine paying $1,200 rent each month for two years. Without reporting, that history sits invisible. With reporting, it adds a record of consistent, on-time payments. For many people, this alone raises scores within a few months.

Landlords often sign up for rent reporting like axcessrent, or you can use a third-party service. It is one of the easiest ways to turn an expense into a credit-building tool.

10. Settle Small Debts First

Sometimes people chase big debts and ignore small ones. But a $150 medical bill sent to collections hurts just as much as a $2,000 one. Clearing small accounts quickly removes multiple negative marks in less time.

It feels motivating too. Each cleared debt shows progress and gives you a boost to keep going. Think of it as cleaning small stains before tackling the big ones.

How Long Does It Take to See Results?

You may ask, “How quickly can I improve my credit score?” The timeline depends on where you start and which actions you take.

- Within 30 days: Pay down balances, raise limits, or dispute errors. These actions show up quickly.

- Within 3 months: On-time payments stack up, and being added as an authorized user makes a visible difference.

- Within 6–12 months: Consistent effort brings bigger gains. A fair score can rise into the good range.

The key is patience. Credit scores do not change overnight, but steady action creates visible progress faster than most expect.

Mistakes to Avoid When Improving Score

- Closing old accounts: This shortens your credit history and hurts your score. Keep old accounts open even if you rarely use them.

- Maxing out one card: Better to spread balances across cards than to max one out.

- Ignoring small bills: Even small unpaid debts cause damage.

- Opening too many new accounts: Lenders may see it as risky behavior.

Avoid these traps, and every positive step you take will have more power.

Real-Life Example of Fast Improvement

Take Sarah, a 29-year-old with a credit score of 620. She felt stuck, rejected for loans, and paying high interest. She decided to take three steps.

First, she paid $3,000 toward her $5,000 balance. Next, she asked her bank to raise her card limit from $5,000 to $7,500. Finally, she disputed a false late payment on her report.

Within 45 days, her score rose to 690. The difference? A car loan that would have cost $420 per month now cost $300. That is $120 saved every month, just by making a few smart moves.

Final Thoughts

Improving your credit score quickly is not some hidden trick or a secret hack that only experts know. It comes down to a series of smart, targeted steps that anyone can take. Paying down high balances, fixing errors on your report, and adding positive accounts are not complicated, but they do require focus and consistency. Even something as simple as setting reminders to pay bills on time builds a foundation that credit bureaus notice.

The best part is that progress shows up faster than most people expect. Many believe you need years to repair your credit, but in reality, a few months of the right moves can unlock real change. A small increase of 30 to 50 points might not sound huge, yet it can transform your financial options. That difference can decide whether you get approved for a mortgage, whether you qualify for a lower car loan payment, or whether you finally receive a credit card with rewards instead of one with high fees.

Think of your credit score as a financial passport. The higher it climbs, the more doors open for you. Landlords feel more comfortable renting to you, employers may view you as more responsible, and lenders offer you better terms. All of that reduces stress and saves money over time.

So, if your score feels stuck right now, remember it is not permanent. Every payment, every balance you lower, and every error you correct works like a building block. Step by step, those small wins stack into a bigger picture of trust. You do not need perfection, just steady progress.

Start with one action today—pay a little more toward your balance, pull your credit report and scan it for mistakes, or call your bank about raising a limit. These moves may feel small, but they add up quickly. A stronger score is not years away. It is closer than you think, and the journey to excellent credit can start right now.