How Much Is a Down Payment on a House? Pay Less and Qualify

Introduction

You’ve found your dream home, the perfect layout, great neighborhood, maybe even a backyard for your dog.

Now comes the big question: How much do you actually need to put down?

The answer isn’t one-size-fits-all.

While many people assume you need 20% down, the truth is — most buyers don’t pay that much. In fact, the average first-time homebuyer in 2025 puts down just 8%, according to the National Association of Realtors (NAR).

Your down payment depends on several factors:

- The type of mortgage you qualify for

- Your credit score

- Where you’re buying

- Whether you’re a first-time buyer

And here’s the good news: you can buy a home with as little as 3.5% — or even 0% down — if you qualify for the right loan.

In this complete, no-fluff guide, we’ll break down:

- What a down payment really is

- The myth of the 20% rule

- Average down payments across the U.S.

- Minimum requirements by loan type

- How your down payment affects your mortgage

- Smart ways to save

- And real-life examples of how real people bought homes in 2025

Let’s clear up the confusion — so you can plan with confidence.

What Is a Down Payment?

A down payment is the portion of a home’s purchase price that you pay upfront in cash when you close on the house.

For example, if a home costs $350,000 and you put down $35,000, that’s a 10% down payment. The remaining $315,000 is covered by your mortgage.

Why It Matters:

- Reduces your loan amount → lower monthly payments

- Lowers your loan-to-value (LTV) ratio → makes you a less risky borrower

- Can help you avoid private mortgage insurance (PMI) if you put down 20% or more

- Shows lenders you’re serious and have skin in the game

The down payment is due at closing, along with other closing costs (like appraisal fees, title insurance, and taxes).

And while it’s a big upfront cost, it’s also your first step toward building equity in your home.

The Myth of the 20% Down Payment

Let’s clear this up once and for all:

You do NOT need 20% down to buy a home.

Yes, 20% became the gold standard decades ago — mostly because it eliminates the need for PMI on conventional loans. But in today’s market, that number is out of reach for many.

Real Data from 2025:

- All homebuyers: Average down payment = 15%

- First-time buyers: Average down payment = 8%

- Repeat buyers: Average down payment = 17%

(Source: National Association of Realtors, Freddie Mac)

On a $400,000 home:

- 8% down = $32,000

- 15% down = $60,000

- 20% down = $80,000

With rising home prices and student debt, saving 20% can take years — especially in expensive markets.

The reality? Low-down-payment loans are not only available — they’re widely used. And they’re designed to help everyday people become homeowners.

Average Down Payment on a Home in 2025

The amount you need to put down varies by location, buyer type, and loan program.

National Averages (2024–2025):

| Buyer Type | Avg Down payment |

|---|---|

| First-time buyers | 8% |

| Repeat buyers | 17% |

| All buyers (combined) | 15% |

Regional Differences:

- West Coast (CA, WA): 10–18% — high prices mean even 5% requires big cash

- Northeast (NY, NJ): 12–16% — competitive markets favor stronger offers

- Midwest & South: 6–10% — more affordable homes = lower down payments

Trend Over Time:

Down payments have crept up slightly since 2022 due to higher home prices and tighter lending — but low-down-payment options are still widely available.

And remember: averages are just averages. Your personal down payment will depend on your finances, goals, and loan choice.

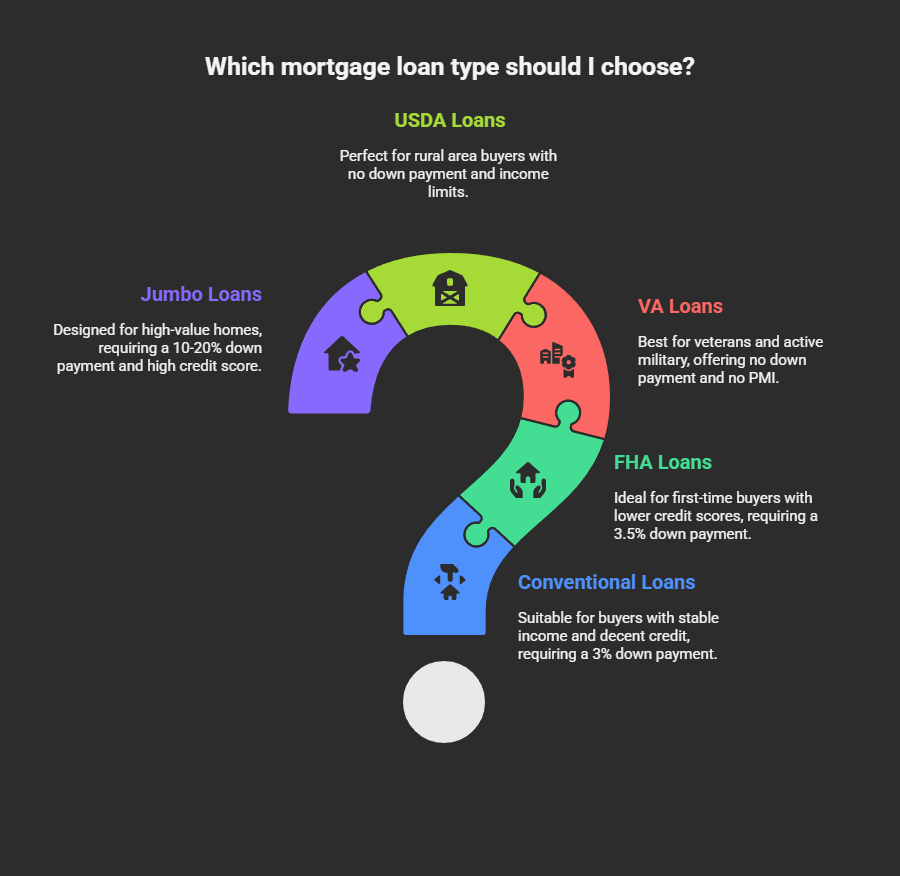

Minimum Down Payment by Loan Type

Not all mortgages are the same. Here’s a breakdown of the most common loan types and how much you need to put down.

1. Conventional Loans

Conventional loans are one of the most common mortgage options, popular with repeat buyers and those who have strong financial profiles. With as little as 3% down and a credit score of 620+, these loans are accessible to many buyers. However, if your down payment is less than 20%, you’ll need to pay private mortgage insurance (PMI). They’re best suited for buyers with steady income, decent credit, and plans to stay long-term.

- Minimum down payment: 3%

- Credit score needed: 620+

- PMI required? Yes, if down payment < 20%

- Best for: Buyers with stable income and decent credit

Popular with repeat buyers and those with good credit.

2. FHA Loans (Federal Housing Administration)

FHA loans are designed to help first-time buyers and those with lower credit scores achieve homeownership. With a minimum down payment of just 3.5% for credit scores 580+, they’re one of the easiest ways to qualify for a mortgage. Even if your credit is below 580, you may still qualify with 10% down. FHA loans require mortgage insurance, but their flexible requirements make them one of the most popular paths to buying a first home.

- Minimum down payment: 3.5% (with 580+ credit score)

- If credit < 580: 10% down required

- Mortgage Insurance: Required for life of loan if down < 10%

- Best for: First-time buyers, lower credit scores

One of the most popular options for new homeowners.

3. VA Loans (For Veterans & Active Military)

VA loans are a unique benefit for veterans, active-duty service members, and eligible spouses. They allow buyers to purchase a home with no down payment, no PMI, and flexible credit requirements. Most lenders look for a 620+ score, but there’s no official minimum. While there’s a funding fee, it can be rolled into the loan. With 100% financing and no mortgage insurance, VA loans are one of the most powerful homebuying tools available.

- Minimum down payment: 0%

- Credit score: No official minimum (most lenders want 620+)

- PMI required? No

- Funding fee: 1.4%–3.6% (can be rolled into loan)

- Eligibility: Veterans, active-duty, eligible spouses

A powerful benefit — 100% financing with no mortgage insurance.

4. USDA Loans (Rural Development)

USDA loans are perfect for buyers looking to purchase in smaller towns, rural areas, or eligible suburbs. They require no down payment, making them highly affordable for low- to moderate-income families. However, buyers must meet income limits and the property must be in a USDA-eligible location. With a small guarantee fee and annual fee, USDA loans offer a great way to achieve homeownership while keeping costs low—ideal for families wanting more space outside of cities.

- Minimum down payment: 0%

- Location: Must be in a USDA-eligible rural area

- Income limits: Yes (varies by county)

- Guarantee fee: 1% upfront + 0.35% annual fee

- Best for: Low- to moderate-income buyers in qualifying areas

Great for buyers in smaller towns or suburbs.

5. Jumbo Loans

Jumbo loans are designed for buyers purchasing high-value homes that exceed the conforming loan limit ($766,550 in 2025). These loans typically require a larger down payment—between 10% and 20%—and a strong credit score of 700 or higher. Lenders also expect borrowers to have several months of mortgage payments in reserve. Best for luxury or high-cost area homes, jumbo loans allow qualified buyers to secure financing when conventional loan limits aren’t enough.

- Minimum down payment: 10–20% (sometimes more)

- Loan limit: Above $766,550 (2025 conforming limit)

- Credit score: 700+

- Reserves required: 6–12 months of payments

- Best for: Expensive homes in high-cost areas

Used when the loan amount exceeds conventional limits.

Comparison Table: Down Payment Requirements at a Glance

| Loan type | Min. Down Payment | Credit Needed | PMI/MIP ? |

|---|---|---|---|

| Conventional | 3% | 620+ | Yes (<20%) |

| FHA | 3.5% | 580+ | Yes (MIP) |

| VA | 0% | Varies | No |

| USDA | 0% | Varies | No (but fees) |

| Jumbo | 10–20% | 700+ | Yes |

First-Time Home Buyer Down Payment Options

If this is your first home, you have more help than ever.

Special Programs & Options:

- FHA Loans: 3.5% down, flexible credit rules

- HomeReady® (Fannie Mae): 3% down, reduced mortgage insurance

- Home Possible® (Freddie Mac): Same as HomeReady — great for low-to-moderate income

- State & Local Assistance Programs (DAPs): Grants or second mortgages for down payment and closing costs

- Examples: CalHFA (California), HDA (Texas), NYHMFA (New York)

- Gift Funds: Most loans allow family to gift down payment money (with a letter)

- IRA Withdrawal: First-time buyers can take up to $10,000 penalty-free from a traditional IRA

“First-time buyer” means you haven’t owned a home in the past 3 years — so even if you’ve bought before, you may still qualify.

How Your Down Payment Affects Your Mortgage

Your down payment doesn’t just change how much you borrow — it impacts your entire loan.

Key Effects:

- Loan Amount: Lower down = higher loan = higher monthly payment

- Interest Rate: Larger down payments may qualify for better rates

- Private Mortgage Insurance (PMI):

- Required on conventional loans with <20% down

- Costs 0.5%–1% of loan annually

- Example: $300/month on a $300,000 loan

- Can be removed once you reach 20% equity

- Equity: A 20% down payment = 20% equity from day one

- Offer Strength: In competitive markets, a higher down payment makes your offer more attractive

Example: $300,000 Home

| Down Payment | Loan Amount | PMI ? | EST. monthly payments |

|---|---|---|---|

| 5% ($15k) | $285,000 | Yes | ~$1,950 + $150 PMI |

| 10% ($30k) | $270,000 | Yes | ~$1,850 + $130 PMI |

| 20% ($60k) | $240,000 | No | ~$1,650 |

Can You Buy a House with No Down Payment?

Yes — but only with specific loans.

0% Down Options:

- VA Loans: For veterans, active-duty, and eligible spouses

- USDA Loans: For buyers in rural areas with income limits

What You Still Need to Pay:

Even with $0 down, you’ll need cash for:

- Closing costs (2%–5% of home price)

- Appraisal and inspection fees

- Title insurance

- Prepaid taxes and insurance

On a $300,000 home, closing costs could be $6,000–$15,000.

But compared to a $60,000 down payment? That’s a huge advantage.

How to Save for a Down Payment

Saving thousands — or tens of thousands — feels overwhelming. But it’s doable with a plan.

Smart Saving Strategies:

- Set a Goal: Use a down payment calculator to know exactly how much you need.

- Open a High-Yield Savings Account: Earn 4%+ APY (e.g., Ally, Marcus, Capital One).

- Automate Transfers: Set up $100–$500/month to go straight to your home fund.

- Cut Expenses: Cancel unused subscriptions, cook at home, drive less.

- Increase Income: Side hustle, freelance work, sell old stuff.

- Use Windfalls: Tax refunds, bonuses, holiday gifts — put them straight into savings.

- Get Help:

- Gift funds from family (documented)

- Down payment assistance (grants or low-interest loans)

- IRA withdrawal (up to $10,000 penalty-free)

- House Hack: Buy a duplex, live in one unit, rent the other to cover your mortgage.

Example: Save $400/month at 4.5% interest → $20,000 in 4 years

Tips for Choosing the Right Down Payment Amount

There’s no “perfect” number — just what’s right for you.

Ask Yourself:

- Can I afford a larger down payment without draining my emergency fund?

- What loan types do I qualify for?

- Is the market competitive? (Higher down = stronger offer)

- Do I plan to stay long-term? (More down = more equity)

- Could that money earn more in investments? (Opportunity cost)

Smart Strategy:

Aim for at least 10% down if you can. Why?

- Reduces PMI duration

- Lowers monthly payment

- Makes you a more competitive buyer

- Still leaves you with cash reserves

Example: On a $350,000 home, 10% ($35k) avoids PMI faster than 5% ($17.5k) and saves thousands over time.

What Happens at Closing?

Your down payment is due on closing day.

How It Works:

- You’ll wire the funds to the title company or bring a cashier’s check

- It’s part of your total closing costs (which include fees, taxes, insurance)

- You’ll get a Closing Disclosure 3 days before closing — review it carefully

- The down payment is applied to the purchase price

- The rest of your cash covers closing fees

Pro Tip: Have your money cleared and ready at least 24 hours before closing to avoid delays.

Real-Life Examples: How People Bought Homes in 2025

Example 1 :

In 2025, many buyers found creative ways to achieve homeownership despite rising prices. Take Sarah, a first-time buyer in Ohio. With a $250,000 home, she used an FHA loan and made a 3.5% down payment of $8,750. To cover this, Sarah combined a $5,000 gift from her parents with $3,750 she saved. While she had to pay mortgage insurance (MIP), this didn’t stop her from moving into a home she truly loves. Similarly, James, a veteran in Texas, purchased a $300,000 home using a VA loan. With no down payment required, he only covered $6,000 in closing costs from savings and enjoyed the benefits of no PMI, a low rate, and full ownership.

Example 2 :

For repeat buyers, the journey looked a little different. The Nguyens, upgrading to a larger home in California, purchased an $800,000 property with a jumbo loan. They used $160,000 from the sale of their previous home to make a 20% down payment, which allowed them to avoid PMI and secure the best rate available. Their story highlights how equity can be a powerful tool when moving up in the housing market. Together, these examples show that there is no single path to buying a home in 2025—whether leveraging gifts, benefits, or equity, each buyer carved a unique path to ownership.

Conclusion: You Doesn’t Have to Be Perfect — Just be Smart

The idea that you must put 20% down to buy a home is outdated. In 2025, buyers have more flexible options — from VA and USDA loans with 0% down, to FHA loans starting at 3.5%, and other state or conventional programs that make owning a home more accessible. In fact, the average down payment for first-time buyers is only 8%.

The key is not perfection, but planning wisely. Your down payment impacts your mortgage rate, monthly payment, and equity, but what matters most is consistency and starting where you are. Saving is a journey — take small steps, build momentum, and move closer to your dream. With the right approach, you’re already one step closer to holding the keys.