Smart Asset Allocation: 10 Easy Ways to Protect Your Money

Introduction: Why Asset Allocation Matters More Than Stock Picking

Did you know that according to a landmark Vanguard study, over 90% of portfolio performance is determined by asset allocation rather than individual stock selection? This surprising fact underscores why understanding asset allocation is the single most important investing skill you can master.

{kind=link}

Key Questions We’ll Answer:

- What exactly is asset allocation and why does it dominate investment returns?

- How do different asset classes (stocks, bonds, alternatives) behave in various market conditions?

- What are the proven asset allocation strategies used by top investors?

- How should your asset mix change as you age and approach retirement?

- What are the most common asset allocation mistakes to avoid?

We’ll provide actionable advice, real-world examples, and specific portfolio models you can implement immediately. Let’s begin with the fundamentals.

What is Asset Allocation?

Definition and Core Principles

Asset allocation refers to the strategic distribution of investment dollars across different asset categories – primarily stocks (equities), bonds (fixed income), cash, and alternative investments. The goal is to balance risk and reward according to your:

Critical Insight: Asset allocation is not about picking “winning” investments, but about constructing a portfolio that can weather different market environments while progressing toward your objectives.

Asset Allocation vs. Diversification: Key Differences

While related, these concepts serve distinct purposes:

| Factor | Asset Allocation | Diversification |

|---|---|---|

| Focus | Allocation between asset classes | Spread within an asset class |

| Example | 60% stocks, 30% bonds, 10% alternatives | Holding 50+ stocks across sectors |

| Primary Benefit | Controls overall portfolio risk | Reduces specific security risk |

| Adjustment Frequency | Periodic rebalancing | Ongoing security selection |

Real-World Example:

During the 2008 financial crisis: The 2008 financial crisis highlighted the importance of proper asset allocation in protecting wealth during market downturns. Investors who held a portfolio with 100% stocks experienced devastating losses of over 50%, making recovery slow and painful. The extreme volatility and sharp decline in equity markets left many struggling to regain financial stability.

In contrast, a well-balanced portfolio with a 60/40 allocation between stocks and bonds saw a more manageable decline of around 30%. Bonds provided stability and helped cushion losses, allowing investors to recover more quickly. This example underscores the value of diversification and risk management in building a resilient investment strategy.

The Role in Wealth Building: Academic Evidence

Multiple studies confirm asset allocation’s supremacy:

- Brinson, Hood & Bee bower Study (1986): Found 93.6% of portfolio variation explained by asset allocation

- Vanguard Research (2019): Showed proper allocation reduced volatility by 25-50% versus concentrated portfolios

- Dalbir Studies: Consistently show most investors underperform due to poor allocation decisions

Actionable Tip: Before picking investments, spend time determining your ideal asset mix – this decision will have far greater impact than any individual stock or fund choice.

Understanding Asset Classes: Characteristics and Roles

Equities (Stocks): The Growth Engine

Historical Performance: 9-10% average annual return since 1926 (S&P 500)

Current Market Insight (2024): Small-cap value stocks have historically outperformed during rising rate environments, making them potentially attractive now.

Fixed Income (Bonds): The Stabilizer

Key Characteristics:

- Lower volatility than stocks

- Regular interest payments

- Inverse relationship with interest rates

Major Bond Types:

| Type | Average Yield | Risk Level | Best For |

|---|---|---|---|

| U.S. Treasuries | 3-5% | Lowest | Safety seekers |

| Corporate Bonds | 4-7% | Moderate | Income investors |

| Municipal Bonds | 3-6% (tax-free) | Low | High-tax investors |

| High-Yield (Junk) Bonds | 7-10% | High | Yield seekers |

2024 Interest Rate Consideration: With rates rising, short-duration bonds currently offer better protection than long-term bonds.

Cash and Cash Equivalents: Liquidity Providers

The Importance of Cash and Cash Equivalents in Asset Allocation

Cash and cash equivalents play a pivotal role in any well-rounded investment portfolio, serving as the bedrock of liquidity and stability. These assets include high-yield savings accounts (offering 4-5% APY), money market funds, certificates of deposit (CDs), and Treasury bills. While they may not deliver the explosive growth potential of stocks or real estate, their primary function is to provide safety, accessibility, and peace of mind. For example, high-yield savings accounts are ideal for parking funds that need to remain liquid while earning modest returns. Money market funds, on the other hand, offer slightly higher yields with minimal risk, making them a favorite among conservative investors. CDs and Treasury bills, though less flexible due to lock-in periods, provide guaranteed returns backed by the government or financial institutions, ensuring capital preservation. These options collectively ensure that investors have access to liquid assets when needed, without exposing their portfolios to unnecessary risks.

The Strategic Role of Cash in Financial Planning

While cash and cash equivalents may offer minimal growth compared to other asset classes, their strategic role cannot be overstated. First and foremost, they serve as a reliable source of emergency funds, acting as a financial safety net for life’s uncertainties. Whether it’s an unexpected medical bill, urgent home repairs, or a sudden job loss, having liquid assets ensures you’re prepared for unforeseen expenses without disrupting your long-term investments. Beyond emergencies, cash also functions as “dry powder” for investors looking to capitalize on market opportunities. During periods of economic downturns or market volatility, having readily available funds allows you to purchase undervalued assets at discounted prices. This approach aligns seamlessly with tactical asset allocation , where short-term adjustments are made based on market conditions. By maintaining liquidity, you position yourself to take advantage of moments when stocks, bonds, or real estate are priced attractively, enhancing your portfolio’s potential over time.

Balancing Cash with Growth-Oriented Assets

Incorporating cash and cash equivalents into your portfolio requires balancing liquidity and growth. While these assets provide stability, over-allocating to cash can hinder long-term wealth due to low returns and inflation’s impact. A common guideline is to hold enough cash to cover three to six months of living expenses, depending on personal needs. Excess cash should be strategically invested in higher-return assets like equities or real estate to maximize potential. This balance is especially critical in retirement asset allocation , where retirees often use cash equivalents to create a buffer against market volatility while still pursuing growth through equities. Younger investors, with longer horizons, can use cash as a temporary holding place during uncertainty, reallocating to growth assets as conditions improve. Ultimately, understanding how cash fits into your broader strategic asset allocation plan is key—it’s not just about having cash but using it wisely to support your financial goals.

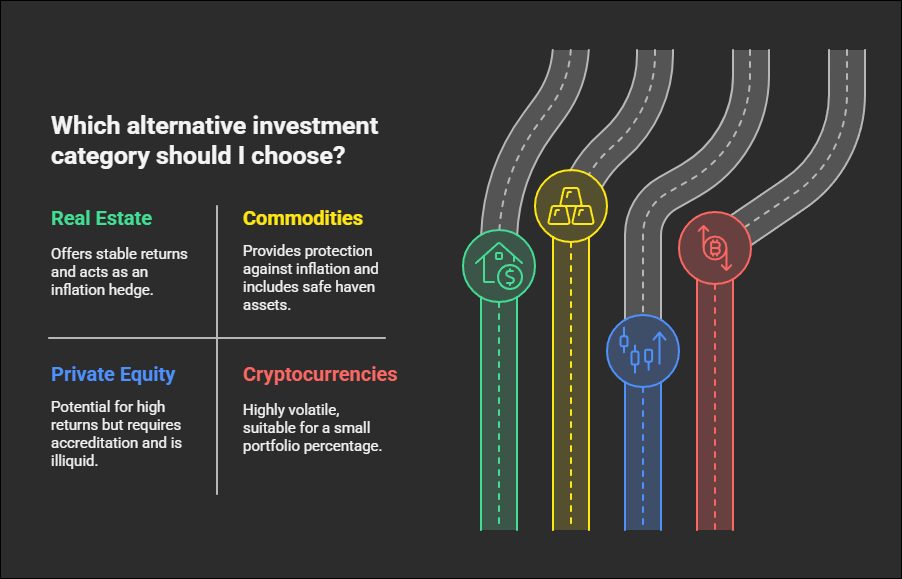

Alternative Investments: Portfolio Diversifiers

Growing Importance: Allocations to alternatives have increased from 5% to 15-20% in modern portfolios.

Expert Tip: Alternatives generally work best when they behave differently than traditional stocks and bonds – focus on low-correlation assets.

Determining Your Optimal Asset Allocation

The Risk Tolerance Assessment

Questionnaire Example:

If your portfolio dropped 20% in a month, how would you react? A conservative investor might panic and sell everything to avoid further losses, while a moderate investor would likely hold steady and wait for the market to recover. On the other hand, an aggressive investor sees this as an opportunity and buys more at lower prices, taking advantage of the downturn. Your risk tolerance plays a crucial role in determining the right investment strategy for you.

Another key factor is your investment time horizon. If you need your money in less than three years, a conservative approach with low-risk assets is best to protect your capital. A moderate investor with a three-to-ten-year horizon can afford some market fluctuations while still aiming for growth. Those with a long-term horizon of ten or more years can take on more risk, as they have ample time to recover from market downturns and capitalize on long-term growth.

Your primary investment goal also shapes your asset allocation strategy. If capital preservation is your priority, a conservative portfolio with bonds and cash equivalents may be ideal. Investors seeking a balance between growth and income may opt for a moderate approach with a mix of stocks and bonds. Meanwhile, those aiming for maximum growth should focus on stocks and other high-return investments, accepting higher volatility for the potential of greater long-term gains.

Scoring: Mostly a’s = Conservative; b’s = Moderate; c’s = Aggressive

Time Horizon Considerations

General Guidelines:

| Years Until Goal | Suggested Stock Allocation |

|---|---|

| 0-3 years | 0-30% |

| 3-7 years | 30-60% |

| 7-15 years | 60-80% |

| 15+ years | 80-100% |

Exception: For retirement income, many advisors recommend maintaining 30-50% in stocks even during retirement to combat inflation.

Goal-Based Allocation Models

Common Financial Goals and Typical Allocations:

For an Emergency Fund (1-2 years of expenses), it’s best to keep 100% in cash or cash equivalents for easy access. For a Home Down Payment with a 5-year horizon, a balanced approach includes 50% in short-term bonds, 40% in CDs or money market accounts, and 10% in stocks for limited growth potential. A Retirement Portfolio with a 30+ year horizon should focus on long-term growth with 80-90% in stocks, 10-20% in bonds, and 5-10% in alternative investments. Finally, for Legacy Wealth intended for multi-generational growth, a diversified mix of 60-70% in stocks, 20% in alternatives, 10% in bonds, and 5% in cash ensures stability while preserving capital for future generations.

Strategic Asset Allocation: The Core Approach

Definition and Mechanics

Strategic asset allocation involves setting target percentages for each asset class and periodically rebalancing back to these targets. This disciplined approach:

- Forces you to “buy low, sell high” through rebalancing

- Maintains consistent risk exposure

- Removes emotion from investment decisions

Sample Strategic Allocations

Choosing the right investment allocation depends on your risk tolerance and financial goals. A Conservative Portfolio (30/60/10) focuses on stability with 30% in stocks, 60% in bonds, and 10% in cash, making it ideal for risk-averse investors. A Moderate Portfolio (60/35/5) balances growth and security with 60% in stocks, 35% in bonds, and 5% in alternatives, perfect for long-term investors seeking steady returns. An Aggressive Portfolio (80/15/5) prioritizes high growth with 80% in stocks, 15% in bonds, and 5% in alternatives, suited for those with a long investment horizon and a higher risk appetite. Find the best strategic asset allocation to match your financial future!

Implementation Tips

- Use Index Funds/ETFs: Low-cost way to gain asset class exposure

- Automate Rebalancing: Many brokerages offer automatic rebalancing

- Tax Considerations: Place bonds in tax-advantaged accounts when possible

Age-Based Asset Allocation: The Lifecycle Approach

The Decade-by-Decade Guide

In your 20s and 30s (Wealth Accumulation Phase), the focus is on growth by leveraging a long time horizon. A portfolio with 90% stocks, 7% bonds, and 3% alternatives allows young investors to maximize returns while tolerating market fluctuations.

By your 40s (Peak Earnings Phase), it’s time to start de-risking while maintaining growth. Allocating 75% to stocks, 20% to bonds, and 5% to alternatives helps balance risk and reward as income peaks and financial responsibilities increase.

As you enter your 50s (Pre-Retirement Phase), capital preservation becomes a priority. A more conservative approach with 60% stocks, 30% bonds, and 10% alternatives/cash helps protect accumulated wealth while still allowing for moderate growth.

During your 60s and beyond (Retirement Phase), the focus shifts to income generation and inflation protection. A balanced portfolio with 40-50% stocks, 40-50% bonds, and 10% cash ensures stability while providing income through dividends and fixed-income investments.

The Glide Path Concept

Target date funds automatically adjust allocations using a “glide path” – gradually becoming more conservative as the target date approaches.

Example Glide Path (Retirement at 65):

| Age | Stocks | Bonds | Cash |

|---|---|---|---|

| 25 | 90% | 10% | 0% |

| 40 | 80% | 18% | 2% |

| 50 | 65% | 30% | 5% |

| 60 | 50% | 45% | 5% |

| 65 | 40% | 55% | 5% |

When planning for retirement, one of the most effective strategies is using a glide path , which outlines how your asset allocation should evolve as you age. This approach helps balance risk and reward, ensuring your portfolio remains aligned with your financial goals at every stage of life. Below, we’ll break down a sample glide path designed for someone aiming to retire at age 65, highlighting key principles and benefits.

Advanced Asset Allocation Strategies

Tactical Asset Allocation

Involves making short-term adjustments (typically 5-15% of portfolio) based on market conditions.

Current Tactical Opportunity (2024): Overweighting value stocks and short-duration bonds given rising rate environment.

Dynamic Asset Allocation

More active approach that responds to economic indicators like:

- Inflation rates

- Yield curve shape

- GDP growth

- Unemployment figures

Example: Reducing equity exposure when the yield curve inverts (historical recession signal).

Core-Satellite Approach

Combines passive and active strategies:

- Core (70-80%): Low-cost index funds

- Satellite (20-30%): Active bets (individual stocks, sector ETFs)

Benefits: Maintains market exposure while allowing for outperformance opportunities.

Portfolio Rebalancing: The Key to Maintaining Allocation

Why Rebalancing Matters

- Maintains target risk level

- Forces disciplined buying low/selling high

- Prevents portfolio drift

Case Study: A 60/40 portfolio left unbalanced from 2009-2019 would have become 80/20 due to stock market growth, exposing the investor to much higher risk.

Rebalancing Methods

Calendar-Based Rebalancing is a simple and structured approach where investors adjust their portfolios at fixed intervals, such as quarterly or annually (with annual rebalancing being the most common). This method ensures consistency in maintaining asset allocation and prevents portfolios from drifting too far from the target.

Threshold-Based Rebalancing focuses on asset class deviations, triggering adjustments when an asset class shifts ±5% from its target allocation. For example, if a portfolio has a 60% stock target, rebalancing occurs when stocks reach 65% or drop to 55%. This approach helps manage risk effectively and keeps investments aligned with long-term goals.

Cash Flow Rebalancing is a tax-efficient strategy that involves using new contributions to buy underweight assets rather than selling overperforming ones. By strategically directing new investments, investors can maintain balance without triggering capital gains taxes, making this an ideal method for tax-conscious portfolio management.

Tax-Efficient Rebalancing

- Rebalance in tax-advantaged accounts (401(k), IRA) first

- For taxable accounts:Tax-Loss Harvesting is a strategic investment approach that involves selling underperforming assets to offset capital gains and reduce taxable income. By avoiding short-term capital gains, which are taxed at higher rates, investors can optimize their tax efficiency while maintaining their portfolio’s long-term growth potential. This method helps minimize tax liability while staying invested in the market by reinvesting in similar assets, ensuring continued portfolio diversification and growth.

Common Asset Allocation Mistakes

Performance Chasing

Example: Moving money into tech stocks after big run-ups (2021) only to suffer 2022 declines.

Solution: Stick to your allocation plan regardless of recent performance.

Overconcentration

Risk: Having too much in:

- Employer stock

- A single sector (e.g., tech)

- Home country (lack of international diversification)

Rule of Thumb: No single position should exceed 5-10% of portfolio.

Ignoring Inflation

Problem: Too much in cash/bonds long-term loses purchasing power.

Fix: Maintain adequate equity exposure even in retirement.

Set-and-Forget Mentality

Reality: Allocations need periodic review as:

- Markets move

- Your situation changes

- Economic conditions evolve

Recommendation: Review allocation at least annually.

Implementing Your Asset Allocation

DIY Approach

Steps:

- Determine your target allocation

- Select low-cost funds for each asset class

- Set up automatic investments

- Schedule rebalancing reminders

Recommended Tools:

Robo-Advisors

Best For: Hands-off investors wanting professional allocation at low cost.

Top Options:

- Betterment

- Wealthfront

- Schwab Intelligent Portfolios

Average Fees: 0.25-0.50% AUM

Financial Advisors

When to Consider:

- Complex situations (business owners, estate planning)

- Behavioral coaching needs

- Tax optimization strategies

Fee Structures:

- AUM (assets under management): 0.50-1.50%

- Hourly: $150-400/hour

- Flat fee: 1,000−1,000−5,000/year

The Future of Asset Allocation

Emerging Trends

- Direct Indexing: Customized index exposure with tax benefits

- Alternative Investments: Becoming more accessible to retail investors

- AI-Driven Allocation: Machine learning models optimizing portfolios

- Sustainable Investing: ESG factors influencing allocation decisions

Final Recommendations

- Start Now: Even small amounts benefit from proper allocation

- Keep Costs Low: Expense ratios erode returns over time

- Stay Disciplined: Avoid emotional decisions during market swings

- Review Regularly: Life changes warrant allocation adjustments

Conclusion: Your Asset Allocation Action Plan

Proper asset allocation isn’t about predicting markets – it’s about preparing for various outcomes while staying aligned with your goals. By implementing the strategies covered in this guide, you’ll be positioned to:

- Weather market downturns with less stress

- Participate in market gains

- Achieve your financial objectives efficiently

Your Next Steps:

- Assess your current allocation

- Determine your target mix based on goals and risk tolerance

- Implement using low-cost, diversified investments

- Maintain through periodic rebalancing

In the world of investing, asset allocation is not just a strategy—it’s a cornerstone of financial success. By thoughtfully distributing your investments across various asset classes like stocks, bonds, cash, and alternatives, you create a portfolio that aligns with your goals, risk tolerance, and time horizon. Whether you’re focused on retirement asset allocation , building wealth over decades, or achieving short-term objectives like saving for a home, understanding how to allocate your assets effectively can make all the difference.

Throughout this guide, we’ve explored the nuances of asset allocation by age , emphasizing how younger investors can afford to take on more risk with growth-oriented assets, while older investors prioritize stability and preservation of capital. We’ve also delved into advanced strategies like strategic asset allocation and tactical asset allocation , highlighting their roles in adapting to market conditions and economic cycles. For those seeking simplicity, tools like target-date funds offer a hands-off approach to life stage investing , while DIY investors can leverage rebalancing techniques and tax-efficient strategies to optimize their portfolios.

However, successful asset allocation isn’t just about numbers—it’s about discipline. Sticking to your plan during market volatility, avoiding emotional decision-making, and regularly reviewing your portfolio are essential habits for long-term success. Remember, the goal isn’t to chase short-term gains but to build a resilient portfolio that grows steadily over time.

Ultimately, whether you choose to manage your investments independently or seek professional guidance, mastering asset allocation empowers you to take control of your financial future. By incorporating the principles outlined in this guide—understanding risk tolerance, leveraging diversification, and staying adaptable—you can navigate the complexities of investing with confidence. Start today, and let your well-allocated portfolio pave the way to achieving your dreams.

FAQ’s

1. What is asset allocation, and why is it important for retirement?

Asset allocation refers to dividing your investment portfolio among different asset classes—such as stocks, bonds, and cash—to balance risk and reward. It’s crucial for retirement planning because the right asset allocation strategy helps you grow your wealth while managing risks based on your age, goals, and time horizon.

2. How does asset allocation change as I get closer to retirement?

As you approach retirement, your asset allocation typically shifts from growth-oriented assets like stocks to more stable options like bonds and cash. This transition reduces volatility and protects your savings, ensuring you have enough income during retirement.

3. What is a glide path in asset allocation?

A glide path is a pre-determined strategy that adjusts your asset allocation over time. It gradually reduces exposure to high-risk assets (like stocks) and increases allocations to low-risk assets (like bonds and cash) as you near retirement.

4. How do I determine the right asset allocation for my age?

The right asset allocation by age depends on your financial goals, risk tolerance, and time horizon. For example:

- Younger investors (20s-30s): 80-90% stocks, 10-20% bonds, minimal cash.

- Mid-career (40s-50s): 60-70% stocks, 30-40% bonds, 5-10% cash.

- Near retirement (60+): 40-50% stocks, 40-50% bonds, 5-10% cash.

5. Can target-date funds help with asset allocation?

Yes! Target-date funds are designed to simplify asset allocation by automatically adjusting your portfolio’s mix of stocks, bonds, and cash based on your expected retirement date. They follow a built-in glide path, making them a hands-off option for retirement planning.

6. What happens if I don’t adjust my asset allocation over time?

Failing to adjust your asset allocation as you age can leave your portfolio exposed to unnecessary risks. For example, holding too much in stocks close to retirement could result in significant losses during a market downturn, jeopardizing your financial security.

7. How often should I review my asset allocation?

You should review your asset allocation at least once a year or after major life events (e.g., marriage, job change, or inheritance). Additionally, rebalance your portfolio whenever it deviates significantly from your target allocation (e.g., by 5% or more).

8. What role does cash play in asset allocation for retirement?

Cash and cash equivalents (like savings accounts or Treasury bills) provide liquidity and stability in your asset allocation . They’re especially important for short-term needs, emergencies, or covering living expenses during retirement without selling volatile assets like stocks.

9. How can I implement a strategic asset allocation plan?

To implement a strategic asset allocation plan:

- Start by defining your financial goals and risk tolerance.

- Choose a mix of asset classes that align with your objectives.

- Use tools like target-date funds, robo-advisors, or manual rebalancing to maintain your desired allocation over time.

10. Is asset allocation the same as diversification?

No, but they’re closely related. Asset allocation involves distributing investments across broad categories (e.g., stocks, bonds, cash), while diversification focuses on spreading investments within those categories (e.g., investing in both domestic and international stocks). Together, they help reduce risk and enhance returns.